Civista Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Civista Bank Bundle

Don't Miss the Bigger Picture

Civista Bank operates within a landscape shaped by intense competition, the bargaining power of its customers, and the constant threat of new entrants. Understanding these forces is crucial for any stakeholder looking to navigate the banking sector.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Civista Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

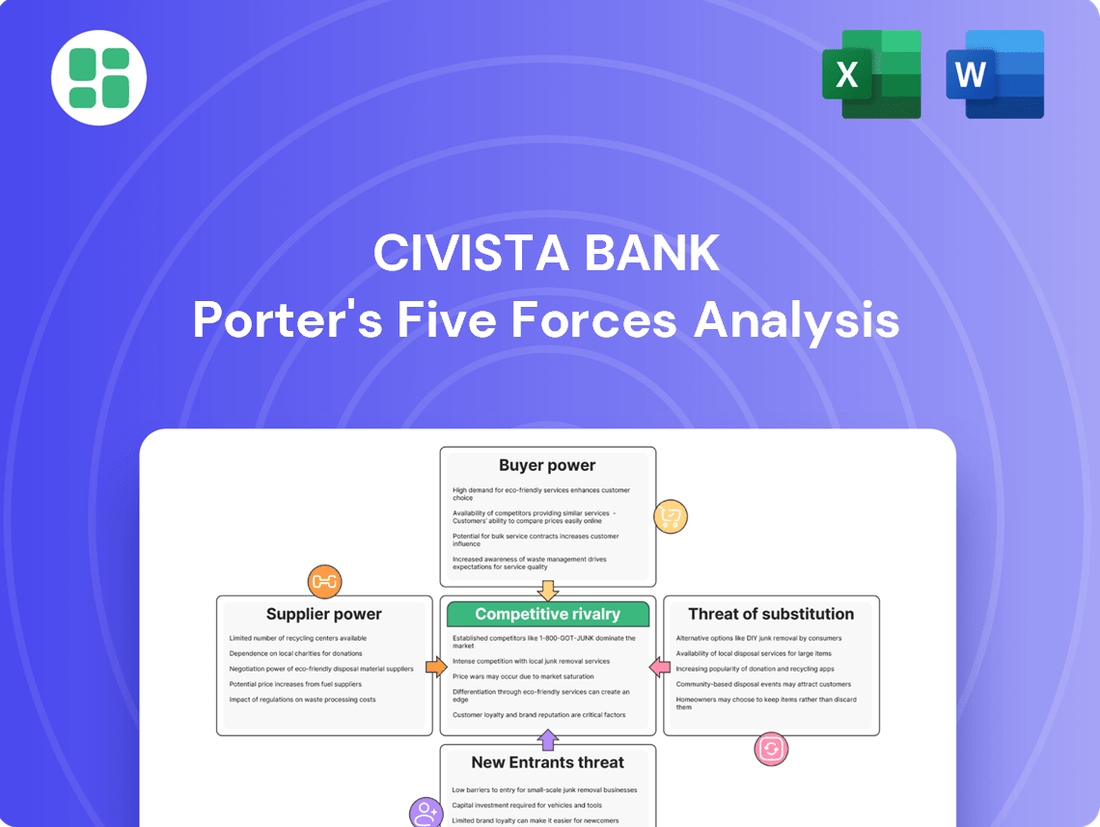

Suppliers Bargaining Power

Access to Capital Markets

Civista Bank's reliance on capital markets for funding means suppliers of capital, like investors and lenders, hold significant bargaining power. The bank's ability to secure funds at favorable rates directly impacts its profitability and expansion plans.

Broader economic factors, interest rate environments, and investor sentiment play a crucial role in determining the cost and accessibility of this capital. For instance, Civista Bank's July 2025 common equity raise of $80.5 million highlights its need to access these markets to fuel growth and potential acquisitions, demonstrating the ongoing negotiation with capital providers.

Depositor Base

Individual and business depositors are essentially the suppliers of funds for Civista Bank, particularly given its focus on core deposit growth as a community bank. While a single depositor might not wield much influence, a collective move towards higher-yield options or alternative investments, spurred by market rates, can significantly amplify their bargaining power. Civista's 2024 financial disclosures highlighted this, showing an increase in their cost of deposits due to heightened competition and a notable migration from non-interest-bearing to interest-bearing accounts, underscoring the impact of depositor preferences.

Technology and Software Providers

Technology and software providers wield considerable influence over banks like Civista Bank. As financial institutions increasingly depend on specialized systems for everything from core operations to digital customer experiences and robust cybersecurity, these vendors become critical partners. The intricate nature of these solutions, often requiring deep customization and carrying substantial switching costs, solidifies their bargaining power.

For Civista Bank, this reliance is amplified by its strategic push into digital banking and its commitment to using technology for profit optimization. This strategic direction inherently increases dependence on these technology vendors, potentially giving them leverage in negotiations. For instance, the global market for banking software and services was projected to reach over $70 billion in 2024, underscoring the significant investment banks make in these areas and the resulting vendor influence.

Human Capital

Skilled employees, especially those with expertise in commercial lending, wealth management, and digital banking, represent a critical supplier of human capital for Civista Bank. The leverage these employees hold is directly tied to prevailing labor market conditions, the demand for their particular skill sets, and Civista's dedication to attracting and retaining top talent. In 2023, the U.S. unemployment rate averaged 3.6%, indicating a relatively tight labor market where skilled workers have more options.

Civista Bank's strategic focus on investing in employee talent and fostering a positive culture underscores its recognition of human capital's significance. This commitment aims to mitigate the bargaining power of suppliers by ensuring a stable and motivated workforce. For instance, banks often invest heavily in training programs; in 2024, the financial services sector is expected to see continued investment in upskilling employees to meet evolving technological demands.

- Talent Specialization: Employees in niche banking areas like specialized lending or advanced financial analytics possess higher bargaining power due to limited supply.

- Market Dynamics: A low unemployment rate, such as the 3.6% recorded in 2023, generally increases the bargaining power of skilled labor across industries, including banking.

- Retention Strategies: Civista's emphasis on talent development and culture directly addresses supplier power by making the bank a more attractive employer, thereby reducing employee turnover.

- Skill Demand: The increasing demand for digital banking expertise and sophisticated wealth management services elevates the bargaining power of employees proficient in these fields.

Regulatory Bodies and Compliance Services

Regulatory bodies act as powerful, albeit non-traditional, suppliers to banks like Civista, essentially granting the license to operate. Their mandates shape everything from capital requirements to consumer protection, directly influencing a bank's cost of doing business and strategic flexibility. For instance, in 2024, the banking sector continued to grapple with evolving cybersecurity mandates, with significant investments required to meet these standards.

The increasing complexity and cost associated with regulatory compliance, particularly in areas like data privacy and anti-money laundering (AML), amplify the bargaining power of these regulatory entities and the specialized service providers that help banks navigate these requirements. This can lead to higher operational expenses for Civista, as adherence to new or updated regulations often necessitates investment in technology and personnel.

Civista Bank's strategic decisions and cost structure are intrinsically linked to compliance. For example, the implementation of new data privacy regulations in 2024, such as those mirroring GDPR principles in various jurisdictions, required substantial upfront investment in systems and ongoing operational adjustments, underscoring the significant influence of regulatory oversight.

- Increased Compliance Costs: Banks face rising expenses for adhering to evolving regulations, impacting profitability.

- Strategic Constraints: Regulatory frameworks can limit a bank's ability to innovate or expand into certain markets.

- Dependence on Compliance Services: Specialized firms offering regulatory solutions gain leverage due to the complexity of compliance.

Civista Bank's Supplier Power Dynamics

Civista Bank's suppliers of capital, including investors and lenders, hold considerable sway over its funding costs and availability. The bank's need for capital, as demonstrated by its July 2025 common equity raise of $80.5 million, directly influences the terms it can negotiate. Broader economic conditions and market sentiment significantly shape this dynamic.

Depositors are a crucial source of funds for Civista, and their collective power can increase if market rates incentivize a shift to higher-yield alternatives. Civista's 2024 financial results showed an increased cost of deposits, reflecting this sensitivity to depositor preferences and competitive pressures.

Technology and software vendors possess significant bargaining power due to banks' increasing reliance on specialized systems for operations and customer experience. High switching costs and the need for customization further solidify this influence, especially as Civista invests in digital banking initiatives, a sector projected to exceed $70 billion globally in 2024.

Skilled employees, particularly those in high-demand areas like digital banking and commercial lending, have growing leverage in a tight labor market. The U.S. unemployment rate averaged 3.6% in 2023, a factor that empowers workers. Civista's investments in talent development aim to mitigate this supplier power by fostering retention.

Regulatory bodies act as powerful suppliers of operational legitimacy, dictating compliance standards that impact costs and strategy. Evolving mandates in 2024, such as those concerning data privacy, necessitate significant investments in technology and personnel, increasing operational expenses for banks like Civista.

| Supplier Type | Key Influence Factor | Impact on Civista Bank | 2023/2024 Data Point |

| Capital Markets | Investor Sentiment, Interest Rates | Cost and availability of funding | July 2025 Equity Raise: $80.5M |

| Depositors | Market Interest Rates, Competition | Cost of deposits, deposit mix | Increased cost of deposits in 2024 |

| Technology Vendors | Specialization, Switching Costs | Operational efficiency, digital capabilities | Global Banking Software Market: >$70B (2024 proj.) |

| Skilled Labor | Labor Market Tightness, Skill Demand | Talent acquisition and retention costs | US Unemployment Rate: 3.6% (2023 avg.) |

| Regulators | Compliance Mandates | Operational costs, strategic flexibility | Increased investment in data privacy compliance (2024) |

What is included in the product

This analysis dissects the competitive forces impacting Civista Bank, revealing the intensity of rivalry, the bargaining power of customers and suppliers, and the threats posed by new entrants and substitutes.

Effortlessly identify and mitigate competitive threats with a visual breakdown of industry power dynamics, allowing Civista Bank to proactively address potential pain points.

Customers Bargaining Power

Deposit Customers

Deposit customers, seeking everything from checking accounts to time deposits, wield significant bargaining power. This power stems from the sheer number of alternative banking options available and the constant competition for better interest rates. Civista Bank, like many others, has seen its deposit costs rise due to this market dynamic, as customers readily move funds for higher yields. For instance, in Q1 2024, the average interest rate on savings accounts across the industry saw an uptick, reflecting this customer leverage.

Loan Customers

The bargaining power of loan customers at Civista Bank is influenced by their creditworthiness, the loan's size, and the overall competitiveness of the lending market. For instance, individuals seeking mortgages or businesses needing commercial loans can leverage strong credit profiles or larger loan amounts to negotiate more favorable terms.

With standardized loan products, customers can readily compare interest rates and conditions offered by various financial institutions, increasing their leverage. Civista Bank's reported loan growth for 2024, alongside initiatives to enhance loan yields, indicates a strategic approach to managing customer demand while prioritizing profitability in this competitive environment.

Wealth Management and Trust Clients

Wealth management and trust clients at institutions like Civista Bank typically possess substantial assets and intricate financial requirements. This financial clout translates directly into significant bargaining power, as they can readily shift their business to competitors offering superior service or returns. For instance, a client managing multi-million dollar portfolios expects highly personalized strategies and consistent performance, making them less sensitive to minor price differences and more focused on value and trust.

The decision-making process for these clients hinges on the quality of bespoke advice, demonstrable investment performance, and the depth of the relationship built with their financial institution. Civista Bank's strategic focus on cultivating robust client relationships and providing customized financial solutions is therefore paramount. This approach is essential not only for retaining these high-value clients but also for attracting new ones who seek a trusted partner for their complex wealth management needs.

Small to Medium-sized Business (SMB) Clients

Small to medium-sized business (SMB) clients often need a comprehensive suite of banking services, including deposits, loans, and sophisticated cash management tools. Civista Bank's focus on relationship banking and providing tailored solutions to these businesses can somewhat mitigate their bargaining power, as these clients value personalized service. However, the growing presence of fintech companies offering specialized services to SMBs is introducing more competition, potentially enhancing the bargaining power of these customers by increasing their available options.

The increasing digital capabilities offered by fintech disruptors are a key factor. For instance, a significant portion of SMBs are actively seeking digital platforms for their financial needs. In 2024, data suggests that over 60% of SMBs are either currently using or exploring fintech solutions for services like payments and lending, which directly impacts their ability to negotiate terms with traditional banks like Civista.

- SMBs demand a mix of deposit, lending, and cash management.

- Civista's relationship banking approach can influence SMB bargaining power.

- Fintech competition is rising, potentially empowering SMB clients.

- Over 60% of SMBs explored fintech in 2024, increasing their options.

Digital-Savvy Customers

Digital-savvy customers wield significant bargaining power due to the proliferation of digital banking and fintech innovations. These consumers expect seamless online experiences, prioritizing convenience and speed, which lowers their switching costs for routine banking services. For instance, in 2024, the global fintech market was valued at over $112 billion, highlighting the competitive landscape and the pressure on traditional banks to offer compelling digital alternatives.

Civista Bank recognizes this trend. Their introduction of Mantle, a new digital deposit account system, is a strategic move to capture online customers beyond their existing physical footprint. This initiative acknowledges that customers can readily shift their funds to institutions providing a superior digital user experience, thereby increasing customer power.

- Digitalization drives customer power: Increased access to fintech solutions empowers customers to seek better digital banking experiences.

- Lower switching costs: For basic banking needs, customers can easily move funds to competitors offering more convenient online platforms.

- Civista's response: The Mantle digital deposit account system aims to attract and retain these digitally inclined customers.

- Market context: The robust growth of the fintech sector in 2024 underscores the competitive pressure on traditional banks to innovate digitally.

Customer Leverage Reshapes Banking Dynamics

Customers' ability to switch providers for better rates or services significantly impacts banks. This is particularly true for deposit customers, where numerous alternatives exist, driving up the cost of funds for institutions like Civista Bank. For instance, in the first quarter of 2024, average savings account interest rates saw an increase across the industry, reflecting this customer leverage.

Loan customers, especially those with strong credit or seeking larger sums, can negotiate favorable terms. The ease with which customers can compare loan products across different banks further amplifies their bargaining power. Civista Bank's 2024 loan growth and yield enhancement strategies highlight their efforts to manage this dynamic.

Wealth management clients, managing substantial assets, hold considerable sway due to their ability to move business to competitors offering superior returns or service. Their expectations for bespoke advice and consistent performance make them powerful negotiators. Civista Bank's focus on relationship banking and tailored solutions is crucial for retaining these high-value clients.

Small to medium-sized businesses (SMBs) often require a broad range of services, and while relationship banking can mitigate their power, the rise of fintech options provides them with more choices. In 2024, over 60% of SMBs were exploring fintech solutions, increasing their leverage in negotiations with traditional banks.

| Customer Segment | Key Bargaining Factors | Civista Bank's Strategic Response | 2024 Market Trend Impact |

|---|---|---|---|

| Deposit Customers | Availability of alternatives, interest rate competition | Focus on digital offerings, competitive rates | Rising savings account rates |

| Loan Customers | Creditworthiness, loan size, market competitiveness | Streamlining loan processes, yield management | Loan growth initiatives |

| Wealth Management Clients | Asset size, complex needs, demand for performance | Personalized advice, relationship building | Focus on client retention and value |

| SMB Clients | Need for diverse services, fintech options | Relationship banking, tailored solutions | Increased fintech adoption by SMBs |

Preview Before You Purchase

Civista Bank Porter's Five Forces Analysis

This preview showcases the comprehensive Civista Bank Porter's Five Forces Analysis, detailing the competitive landscape and strategic positioning of the institution. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, providing actionable insights into industry rivalry, buyer power, supplier power, threat of new entrants, and threat of substitutes. You're looking at the actual document that will equip you with a thorough understanding of Civista Bank's market dynamics.

Rivalry Among Competitors

Local and Regional Banks

Civista Bank faces significant competitive rivalry from local and regional banks within its operating areas of Ohio, Southeastern Indiana, and Northern Kentucky. With 42 locations, it directly contends with numerous community banks and other regional players vying for the same customer base.

This intense competition often centers on factors like personalized customer service, strong community ties, and tailored product offerings. For instance, many community banks in these regions pride themselves on building deep relationships with local businesses and individuals, a key differentiator against larger national institutions.

Large National Banks

While Civista Bank focuses on community banking, it contends with substantial competition from large national banks. These behemoths possess vast financial resources, allowing them to invest heavily in technology and marketing. For instance, in 2023, the top five U.S. banks reported combined net income exceeding $150 billion, demonstrating their immense scale.

These national institutions often offer a wider array of products and services, including sophisticated investment banking and wealth management solutions that may be beyond the scope of a community bank. Their extensive branch networks and advanced digital platforms also provide a significant competitive edge, enabling them to reach a broader customer base and offer greater convenience.

The sheer scale of large national banks allows them to achieve significant economies of scale, which can translate into more competitive pricing for standard banking products like checking accounts and mortgages. This puts pressure on community banks like Civista to differentiate themselves through personalized service and local market expertise, rather than solely competing on price for commoditized offerings.

Credit Unions

Credit unions represent a notable competitive force for Civista Bank, especially in attracting consumer deposits and offering straightforward loan products. Their member-owned structure often allows them to provide more competitive interest rates and lower fees compared to traditional banks. For instance, as of early 2024, the credit union industry in the U.S. held over $2.3 trillion in assets, demonstrating their substantial market presence and ability to compete for customer loyalty.

Fintech Companies and Digital-Only Banks

Fintech companies and digital-only banks are intensifying competitive rivalry for traditional institutions like Civista Bank. These agile players often leverage lower operating costs and superior digital interfaces to attract customers, particularly in high-demand areas such as payments and lending.

For instance, the global fintech market was valued at approximately $2.4 trillion in 2023 and is projected to grow significantly, indicating a strong and expanding competitive threat. Their ability to innovate quickly and offer specialized, often fee-free, services puts pressure on incumbents to adapt their own digital strategies and product offerings.

- Specialized Services: Fintechs excel in specific niches like peer-to-peer payments or buy-now-pay-later, directly challenging traditional banking services.

- Lower Overhead: Digital-only banks operate without the extensive branch networks of traditional banks, allowing for more competitive pricing.

- Enhanced User Experience: Neobanks prioritize seamless, mobile-first customer experiences, which is a key differentiator for digitally savvy consumers.

- Aggressive Market Entry: These new entrants are rapidly gaining market share in areas like consumer lending and digital wallets, forcing established banks to respond.

Interest Rate Environment and Deposit Competition

The current interest rate environment is a major driver of competitive rivalry among banks, forcing them to compete aggressively for deposits by offering more appealing rates. Civista Bank's 2024 annual report and its Q2 2025 earnings both pointed to rising deposit costs, a direct consequence of this intensified competition for customer funds.

This heightened competition for deposits means banks are constantly evaluating and adjusting their offerings to attract and retain customer balances. For Civista Bank, this translates into a direct impact on their net interest margin as they pay more to secure the funding needed for lending activities.

- Increased Deposit Costs: Civista Bank experienced a notable rise in its cost of deposits in 2024, with preliminary Q2 2025 data suggesting this trend continued due to aggressive rate competition.

- Rate Sensitivity: Customers are highly sensitive to interest rate differentials, leading to greater mobility of funds between institutions in pursuit of higher yields.

- Competitive Pressure: The need to offer competitive rates to retain and attract deposits puts pressure on Civista Bank's profitability, especially in a rising rate environment.

Banking Battle: Competition Drives Up Deposit Costs

Civista Bank faces intense competition from local community banks, regional players, and large national institutions, all vying for the same customer base. The rise of credit unions and agile fintech companies further intensifies this rivalry, particularly in attracting deposits and offering digital services.

The need to offer competitive deposit rates, as evidenced by Civista Bank's rising cost of deposits in 2024 and early 2025, directly impacts profitability. This environment forces banks to innovate and differentiate beyond simple pricing to maintain market share and customer loyalty.

| Competitor Type | Key Competitive Factors | Example Data/Impact |

|---|---|---|

| Community Banks | Personalized service, community ties | Strong local relationships |

| National Banks | Scale, technology, broad product offerings | Combined 2023 net income > $150 billion |

| Credit Unions | Competitive rates, lower fees | Over $2.3 trillion in assets (early 2024) |

| Fintech/Digital Banks | Agility, lower costs, digital experience | Global fintech market valued at ~$2.4 trillion (2023) |

SSubstitutes Threaten

Fintech Lending Platforms

Fintech lending platforms present a significant threat of substitutes for Civista Bank. Online lenders and peer-to-peer platforms offer alternative credit sources, often with quicker approvals and more adaptable terms than traditional bank loans. For instance, the online lending market in the US saw substantial growth, with loan volumes projected to reach hundreds of billions of dollars annually by 2024, directly competing with Civista's core lending business.

Digital Payment Systems and Mobile Wallets

Digital payment systems and mobile wallets like PayPal, Venmo, and Apple Pay present a significant threat of substitutes for Civista Bank's core transaction services. These platforms facilitate peer-to-peer payments and online purchases, often bypassing traditional banking channels for everyday spending. By July 2024, the global digital payments market was projected to reach over $10 trillion, highlighting the immense scale of this substitute threat.

Investment Vehicles and Brokerage Firms

Customers seeking savings and wealth management have a vast array of substitutes beyond Civista Bank's traditional deposit accounts. These include mutual funds, individual stocks, bonds, and the direct investment platforms provided by numerous brokerage firms.

These alternatives often present the allure of higher potential returns, particularly during periods when interest rates on conventional savings accounts remain subdued. For instance, as of early 2024, the average savings account yield hovered around 0.45%, while the S&P 500 saw a significant rebound, gaining over 10% in the first quarter of 2024, illustrating the return differential.

The accessibility and user-friendliness of digital brokerage platforms further amplify the threat of substitutes. Many of these platforms offer commission-free trading and sophisticated analytical tools, making it easier for individuals to manage their investments directly, bypassing traditional banking channels for wealth accumulation.

Credit Unions and Non-Bank Financial Institutions

Credit unions represent a significant threat of substitutes for community banks like Civista Bank. These member-owned cooperatives offer a comprehensive suite of banking services, from checking and savings accounts to loans and mortgages, directly competing with Civista's core offerings. In 2023, credit union membership in the U.S. surpassed 136 million, indicating a substantial customer base actively choosing alternatives to traditional banks.

Beyond credit unions, specialized non-bank financial institutions also pose a threat by offering specific services that overlap with Civista's business lines. For instance, companies focusing solely on equipment leasing or business financing can provide a more tailored and potentially aggressive alternative for customers seeking those particular solutions. This fragmentation of services means customers don't always need a full-service bank, increasing the substitutability of Civista's offerings.

- Credit Union Competition: Credit unions offer a full spectrum of banking services, directly challenging community banks.

- Community Focus: Their perceived community orientation can attract customers seeking local, member-focused banking.

- Specialized Non-Banks: Institutions focusing on specific financial products, like equipment leasing, provide targeted alternatives.

- Customer Choice: The availability of specialized providers fragments the market, allowing customers to pick and choose services rather than relying on a single bank.

Alternative Capital Sources for Businesses

Businesses, especially larger corporations, increasingly turn to alternative capital sources, lessening their dependence on traditional bank loans. This is particularly true for substantial growth initiatives or major investment undertakings.

Private equity and venture capital firms, alongside the option to issue corporate bonds, offer viable substitutes for commercial bank financing. For instance, in 2023, global private equity fundraising reached approximately $1.3 trillion, demonstrating the significant capital available outside traditional banking channels.

- Private Equity & Venture Capital: Direct investment from these firms bypasses banks for equity stakes or growth capital.

- Corporate Bonds: Issuing debt directly to investors provides an alternative to bank loans for funding.

- Public Offerings: While more involved, initial public offerings (IPOs) are another way to raise substantial capital without bank intermediation.

- Crowdfunding & Peer-to-Peer Lending: For smaller businesses, these platforms offer accessible, albeit often smaller-scale, alternatives to bank credit.

Digital & Non-Bank Alternatives: A Growing Threat to Traditional Banking

The threat of substitutes for Civista Bank is substantial, encompassing digital alternatives and non-bank financial institutions. Fintech lending platforms, digital payment systems, and a wide array of investment vehicles directly challenge Civista's core services, offering convenience, potentially higher returns, and specialized solutions. Credit unions and non-bank lenders further fragment the market, providing customers with choices that bypass traditional banking relationships.

Businesses also increasingly access capital through alternative channels, reducing reliance on bank loans. Private equity, venture capital, and corporate bonds represent significant substitutes for commercial financing, with substantial capital flowing through these avenues. Even smaller businesses can find alternatives in crowdfunding and peer-to-peer lending platforms.

| Substitute Category | Examples | Impact on Civista Bank | Market Data (2024 Estimates/Trends) |

|---|---|---|---|

| Fintech Lending & P2P | Online lenders, peer-to-peer platforms | Direct competition for loans, potentially faster approvals | US online lending market volume projected in hundreds of billions annually. |

| Digital Payments & Wallets | PayPal, Venmo, Apple Pay | Threat to transaction services, bypassing traditional channels | Global digital payments market projected over $10 trillion. |

| Investment & Savings Alternatives | Mutual funds, stocks, bonds, brokerage platforms | Competition for customer deposits and wealth management | S&P 500 gained >10% in Q1 2024; avg. savings account yield ~0.45%. |

| Credit Unions | Member-owned financial cooperatives | Offer full banking services, community appeal | Over 136 million U.S. credit union members in 2023. |

| Specialized Non-Banks | Equipment leasing, business financing firms | Provide tailored solutions for specific customer needs | Market fragmentation allows customers to pick and choose services. |

| Alternative Business Capital | Private equity, venture capital, corporate bonds | Reduce reliance on bank loans for business funding | Global private equity fundraising ~$1.3 trillion in 2023. |

Entrants Threaten

High Regulatory Barriers

The banking sector is characterized by formidable regulatory barriers that significantly impede new entrants. Obtaining the necessary licenses, adhering to stringent capital adequacy ratios, and navigating continuous federal and state oversight demand substantial upfront investment and ongoing compliance efforts. For instance, in 2024, the Federal Reserve's stress tests continue to enforce rigorous capital requirements, making it difficult for newcomers to meet the necessary financial thresholds.

Significant Capital Requirements

Establishing a new bank, whether traditional or digital, demands substantial initial capital to meet regulatory minimums, build infrastructure, and fund initial operations. For a full-service community bank like Civista, this includes physical branches, technology, and a robust lending capacity, often requiring hundreds of millions of dollars to even begin competing effectively.

Brand Reputation and Trust

In the banking sector, brand reputation is paramount, and Civista Bank, with its origins in 1884, has cultivated deep-seated trust and recognition within its operational areas. This established goodwill represents a significant barrier for new entrants aiming to attract customers and deposits. For instance, in 2024, customer retention rates in the banking industry often exceed 90% for established institutions, highlighting the difficulty new players face in displacing incumbents.

Economies of Scale and Network Effects

Existing banks, like Civista Bank, possess significant advantages due to economies of scale. This allows them to spread the costs of transaction processing, technology, and overhead across a vast customer base, leading to lower per-unit costs. For instance, in 2024, major banks reported substantial operational efficiencies driven by their scale, with some seeing cost-to-asset ratios below 0.5%.

Network effects further bolster incumbent banks. Established branch networks and widespread payment system integration create a powerful moat. New entrants would find it incredibly challenging and expensive to replicate this level of accessibility and trust quickly. In the US, for example, the average large bank operates hundreds of branches, a physical footprint difficult for a startup to match in the short term.

- Economies of Scale: Larger banks can process more transactions at a lower cost per transaction due to their extensive infrastructure and technology investments.

- Network Effects: Established customer bases and integrated payment systems create a self-reinforcing advantage for existing players.

- High Setup Costs: New entrants face substantial capital requirements to build comparable branch networks and technological capabilities.

- Customer Inertia: Consumers often prefer the convenience and familiarity of established banking relationships, making switching difficult for new entrants.

Emergence of Niche Fintech Players

While establishing a full-service bank remains a significant hurdle due to extensive regulations and capital requirements, the threat of new entrants for Civista Bank is more pronounced from specialized fintech companies. These agile players often target specific, profitable banking functions like digital payments, online lending, or automated investment advice. For instance, the global fintech market was valued at approximately $2.4 trillion in 2023 and is projected to grow substantially, indicating a fertile ground for new, focused entrants.

These niche fintechs can erode traditional banks' market share and revenue streams by offering streamlined, often lower-cost alternatives for particular services. They typically operate under less stringent regulatory frameworks compared to chartered banks, allowing for quicker innovation and market penetration. By focusing on a single service, they can achieve operational efficiencies that traditional banks, with their broader mandates, find harder to replicate.

- Niche Fintech Focus: Fintechs concentrate on specific banking services like payments or lending.

- Reduced Regulatory Burden: Niche players face fewer regulations than full-service banks.

- Revenue Stream Erosion: Fintechs can capture market share from traditional banking services.

- Market Growth: The global fintech market's significant growth signals opportunities for new entrants.

Fintechs Redefine Banking Entry: A Shifting Competitive Landscape

The threat of new entrants for Civista Bank is generally low due to high barriers like stringent regulations and substantial capital requirements, making it difficult for traditional banks to emerge. However, the landscape is shifting with the rise of specialized fintech companies that can bypass some of these hurdles by focusing on specific services.

Fintechs often leverage technology to offer streamlined, cost-effective alternatives for payments, lending, or wealth management, directly competing with established banks. For instance, the global fintech market was valued at approximately $2.4 trillion in 2023 and is expected to see continued growth, highlighting the potential for these agile competitors.

These niche players can erode traditional banks' revenue streams by capturing market share in profitable segments, often with a lighter regulatory touch. This focused approach allows them to innovate rapidly and gain customer traction more easily than a full-service startup bank could.

While Civista benefits from economies of scale and established brand loyalty, the agility and targeted offerings of fintechs present a more immediate competitive pressure. This dynamic is particularly relevant in 2024 as digital banking adoption continues to accelerate.

| Factor | Impact on New Entrants | Example/Data (2023-2024) |

| Regulatory Hurdles | High | Federal Reserve stress tests (2024) enforce rigorous capital requirements. |

| Capital Requirements | High | Establishing a full-service bank requires hundreds of millions of dollars. |

| Brand Reputation | High Barrier | Customer retention for established banks often exceeds 90% (2024). |

| Fintech Specialization | Moderate Threat | Global fintech market valued at ~$2.4 trillion (2023), showing growth potential for niche players. |

Porter's Five Forces Analysis Data Sources

Our Civista Bank Porter's Five Forces analysis is built upon a foundation of verified data, including Civista Bank's annual reports and SEC filings, alongside industry-specific research from sources like IBISWorld and S&P Global Market Intelligence.