Central Bank of India Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Central Bank of India Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Central Bank of India faces intense competition from established banks and nimble fintech players, significantly impacting its market position. The bargaining power of customers is considerable, as they have numerous banking options and readily available information. Understanding these pressures is crucial for strategic planning.

The complete report reveals the real forces shaping Central Bank of India’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Depositors (Individuals & Corporates)

Depositors, both individuals and corporations, wield considerable power over the Central Bank of India. In 2023, India's credit growth outpaced deposit growth, forcing banks to compete more aggressively for funds. This competition often translates into higher interest rates offered on term deposits, directly impacting the bank's cost of funds and potentially squeezing net interest margins.

Technology Providers

Technology providers wield considerable bargaining power over Central Bank of India, especially as digital banking becomes paramount. The bank's reliance on IT vendors for core banking, cybersecurity, and AI/ML integration means these specialized services are crucial for its operations. For instance, in 2024, the global IT services market for financial institutions was valued at over $200 billion, highlighting the scale and importance of these suppliers.

Human Capital/Skilled Workforce

The Central Bank of India's reliance on a skilled workforce, especially in digital banking and data analytics, significantly influences its operational efficiency and competitive edge. A scarcity of professionals in these critical domains, as seen in the broader Indian banking sector where demand for tech-savvy talent outstrips supply, can escalate recruitment costs and lengthen hiring timelines.

This heightened demand for specialized skills, particularly in areas like cybersecurity and AI-driven financial services, translates into increased bargaining power for potential employees. For instance, reports from early 2024 indicated a significant premium on salaries for data scientists and cybersecurity experts in the Indian financial services industry, directly impacting labor costs for banks like Central Bank of India.

Ultimately, the bank's capacity to attract and retain top-tier talent in these specialized fields is a crucial determinant of its future performance and its ability to adapt to the evolving financial landscape.

Regulatory Bodies (RBI)

The Reserve Bank of India (RBI) exerts significant bargaining power as a supplier of the operating environment for banks. Its monetary policies, such as the repo rate and cash reserve ratio, directly impact banks' cost of funds and lending capabilities. For instance, the RBI's decision to maintain the repo rate at 6.50% as of early 2024 influences the interest income banks can generate.

The RBI's regulatory framework, including directives on capital adequacy ratios (CAR) and asset quality, dictates how banks must operate and manage risk. For example, the Basel III norms, implemented by the RBI, require banks to maintain higher capital buffers, influencing their strategic decisions and profitability. In 2023, Indian banks generally maintained CAR well above the regulatory minimums, with many exceeding 15%.

Further, the RBI's licensing and supervisory powers grant it considerable influence. Its approval is necessary for new banking licenses and for significant operational changes. Recent actions, like the RBI's focus on strengthening governance and risk management in the digital banking space, set clear operational parameters that banks must adhere to, impacting their technology investments and business models.

- RBI's Repo Rate: Maintained at 6.50% (as of early 2024), influencing banks' borrowing costs.

- Capital Adequacy Ratios (CAR): Indian banks generally exceeded 15% in 2023, demonstrating robust capital buffers above regulatory requirements.

- Regulatory Directives: RBI's ongoing emphasis on digital banking security and governance shapes technological adoption and operational strategies.

Credit Rating Agencies

Credit rating agencies are significant suppliers to the Central Bank of India, providing an essential service that influences its access to capital. By evaluating the bank's financial health, these agencies essentially supply trust and credibility, which directly impacts the bank's ability to tap into capital markets. A positive rating from agencies like CRISIL or ICRA can significantly reduce borrowing costs, while a downgrade can have the opposite effect, potentially increasing funding expenses and deterring investors.

The bargaining power of credit rating agencies stems from their expertise and the market's reliance on their assessments. For Central Bank of India, a favorable rating is not just about cost; it's about maintaining investor confidence and ensuring a steady flow of capital. For instance, in 2023, Indian banks generally saw stable to positive rating outlooks, reflecting the sector's resilience, which indirectly benefits institutions like Central Bank of India by lowering the perceived risk by investors.

- Influence on Borrowing Costs: Favorable ratings from agencies can lower the cost of debt for Central Bank of India.

- Investor Confidence: Ratings directly impact investor perception and willingness to invest in the bank's securities.

- Access to Capital Markets: A good rating is often a prerequisite for accessing international and domestic debt markets efficiently.

- Regulatory Compliance: Certain regulatory requirements may be linked to credit ratings, further emphasizing their importance.

Central Bank of India: Navigating Supplier Power in a Digital Era

The Central Bank of India faces significant bargaining power from its technology providers, especially in the current digital-first banking environment. The bank's reliance on specialized IT vendors for core banking systems, cybersecurity solutions, and advanced analytics means these suppliers hold considerable sway. In 2024, the global market for financial IT services was projected to exceed $200 billion, underscoring the critical and often indispensable nature of these technology partners.

Furthermore, the bank's need for specialized talent, particularly in areas like data science and cybersecurity, amplifies the bargaining power of potential employees and recruitment agencies. As of early 2024, the demand for such skills in India's financial sector significantly outstripped supply, leading to increased salary expectations and longer hiring cycles for institutions like Central Bank of India.

The Reserve Bank of India (RBI) acts as a powerful supplier of the regulatory and monetary framework within which Central Bank of India operates. Its monetary policies, such as the repo rate, directly influence the bank's cost of funds and lending rates. For example, the RBI's decision to maintain the repo rate at 6.50% in early 2024 sets a benchmark for borrowing costs across the banking sector.

Additionally, the RBI's stringent regulatory directives, including capital adequacy requirements and asset quality norms, dictate operational standards and capital management strategies. Compliance with frameworks like Basel III, which requires robust capital buffers, is essential, and in 2023, Indian banks generally maintained capital adequacy ratios well above the minimum regulatory thresholds, often exceeding 15%.

Credit rating agencies also wield considerable bargaining power by supplying essential assessments of Central Bank of India's creditworthiness. Their evaluations directly impact the bank's ability to access capital markets and influence borrowing costs. A favorable rating from agencies like CRISIL or ICRA in 2023, which generally reflected a stable outlook for Indian banks, can significantly reduce funding expenses and enhance investor confidence.

| Supplier Type | Key Influence | Impact on Central Bank of India | 2023-2024 Data Point |

| Technology Providers | Core Banking, Cybersecurity, AI/ML | Increased reliance, potential for higher service costs | Global financial IT services market > $200 billion (2024 projection) |

| Skilled Workforce (Tech) | Digital Banking, Data Analytics Expertise | Higher recruitment costs, longer hiring timelines | Significant salary premiums for data scientists/cybersecurity experts (early 2024) |

| Reserve Bank of India (RBI) | Monetary Policy, Regulatory Framework | Dictates cost of funds, lending rates, operational standards | Repo rate maintained at 6.50% (early 2024); CAR generally > 15% (2023) |

| Credit Rating Agencies | Creditworthiness Assessment | Impacts access to capital, borrowing costs, investor confidence | Stable to positive rating outlooks for Indian banks (2023) |

What is included in the product

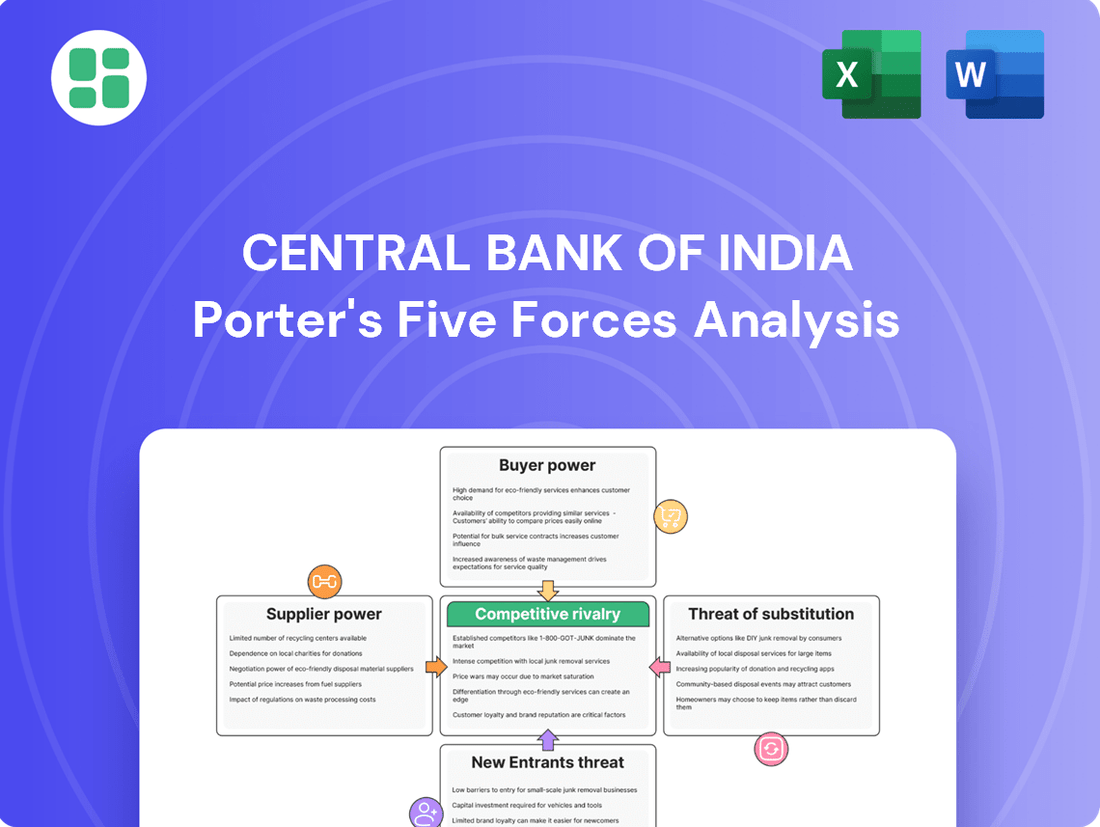

This analysis unpacks the competitive forces impacting the Central Bank of India, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the availability of substitutes within the Indian banking sector.

Gain instant clarity on competitive pressures, enabling proactive strategies to mitigate threats and capitalize on opportunities.

Customers Bargaining Power

Retail Customers (Individuals)

Individual customers, armed with numerous banking choices, wield considerable influence over deposit rates and service standards. The digital revolution, making it simpler than ever to switch providers, amplifies this power, allowing consumers to gravitate towards banks offering superior rates, convenience, or tailored experiences. For instance, in 2024, the average savings account interest rate across Indian banks hovered around 3.5% to 5%, with some digital banks offering slightly higher, giving customers leverage.

Large Corporates and SMEs

Large corporate clients and Small and Medium Enterprises (SMEs) wield considerable bargaining power with the Central Bank of India. This is primarily due to the substantial volume of business they represent and their capacity to negotiate favorable terms for crucial financial services like loans and cash management. Banks, including the Central Bank of India, actively vie for these valuable segments by offering competitive interest rates and tailored solutions.

The Central Bank of India's advances to the corporate and SME sectors demonstrate this dynamic. For instance, as of the fiscal year ending March 2023, total advances by scheduled commercial banks, which includes the Central Bank of India, reached ₹151.4 trillion, with a notable portion directed towards these segments. This indicates the bank's strategic focus on attracting and retaining these clients by offering attractive terms.

Government Entities and Public Sector Undertakings

Government entities and Public Sector Undertakings (PSUs) represent a significant client base for Central Bank of India, and their bargaining power is considerable. As a public sector bank, Central Bank of India often caters to the extensive financial needs of these large organizations, which can translate into substantial transaction volumes. For instance, in 2023, PSUs accounted for a notable portion of the banking sector's credit and deposit base, giving them leverage in negotiating terms for services like large-scale project financing or complex treasury management.

Borrowers (Loan Seekers)

Borrowers, especially those seeking substantial retail or corporate loans, wield significant bargaining power. This power is amplified by the intensely competitive lending landscape where numerous financial institutions actively compete for loan business. For instance, in 2023, the average home loan interest rate in India hovered around 8.5% to 9.5%, creating an environment where borrowers could readily compare and negotiate terms.

The ability for borrowers to easily compare offerings across different banks means they can secure more favorable interest rates, lower processing fees, and more flexible repayment schedules. This is especially true in highly commoditized segments like mortgages, where rates are frequently tied to benchmark indices, making price a primary differentiator.

- Competitive Lending Market: Banks actively compete for loan portfolios, increasing borrower leverage.

- Rate Benchmarking: Key loan products, like home loans, often have benchmarked rates, facilitating easy comparison.

- Negotiable Terms: Borrowers can negotiate interest rates, fees, and repayment structures.

- Increased Borrower Choice: A wider array of lending options empowers borrowers to seek the best financial deals.

Digital-Savvy Customers

The growing digital fluency of customers significantly amplifies their bargaining power against institutions like Central Bank of India. These digitally-savvy individuals increasingly expect intuitive online and mobile banking platforms, pushing the bank to allocate substantial resources towards digital innovation. For instance, a significant portion of banking transactions are now conducted digitally; in 2023, digital channels accounted for over 90% of retail transactions for many major Indian banks.

Customers' demand for seamless user experiences and real-time services directly shapes how Central Bank of India develops its products and delivers its offerings. Failure to keep pace with these evolving digital expectations can lead to customer attrition, as consumers readily switch to fintech companies or competitors offering superior digital engagement. In 2024, fintech adoption rates in India continued to climb, with mobile banking usage showing a steady upward trend, further underscoring this pressure.

- Digital Transaction Growth: In India, digital payments saw a substantial increase, with the volume of UPI transactions alone reaching over 120 billion in the fiscal year 2023-24, indicating a strong customer preference for digital channels.

- Customer Expectations: A recent survey of Indian banking customers revealed that over 70% prioritize ease of use and speed in mobile banking applications when choosing a bank.

- Competitive Landscape: The rise of neobanks and digital-first financial service providers in India offers customers readily available alternatives, intensifying the need for traditional banks to enhance their digital capabilities.

Customer Power Reshapes Banking Dynamics

The bargaining power of customers is a significant force shaping the banking sector, including institutions like the Central Bank of India. This power stems from increased customer choice, digital accessibility, and the commoditization of certain banking services. For instance, in 2024, the competitive landscape for retail deposits meant that banks often had to offer attractive rates to retain customers, with average savings account rates around 3.5% to 5%.

Large corporate clients and SMEs hold substantial sway due to the volume of business they bring. Their ability to negotiate favorable terms on loans and cash management services is a key factor. The Central Bank of India, like its peers, actively seeks to attract and retain these clients by offering competitive interest rates and customized solutions, as evidenced by the ₹151.4 trillion in total advances by scheduled commercial banks in FY23, a significant portion of which served these segments.

| Customer Segment | Basis of Bargaining Power | Impact on Banks |

|---|---|---|

| Individual Retail Customers | High switching costs (low), readily available alternatives, digital convenience | Pressure on deposit rates, demand for better digital services |

| Corporate Clients & SMEs | Large transaction volumes, need for specialized services | Negotiation on loan pricing, fees, and tailored financial products |

| Government Entities & PSUs | Significant deposit and credit base, long-term relationships | Leverage in large-scale financing and treasury management deals |

Preview the Actual Deliverable

Central Bank of India Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of the Central Bank of India you'll receive immediately after purchase, offering a comprehensive understanding of its competitive landscape. You'll gain insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the Indian banking sector. This detailed document is ready for your immediate use, providing a professionally formatted and actionable strategic overview.

Rivalry Among Competitors

Other Public Sector Banks (PSBs)

Central Bank of India navigates a highly competitive landscape with its peers in the public sector banking (PSB) space. Banks like Indian Overseas Bank and IDBI Bank Ltd. present significant rivalry, often mirroring similar product suites and customer bases. This similarity, coupled with a shared objective of financial inclusion, translates into aggressive competition for both customer deposits and loan disbursements nationwide.

Private Sector Banks

Private sector banks, such as HDFC Bank and ICICI Bank, are formidable competitors. Their agility, strong technological investments, and emphasis on customer experience allow them to aggressively capture market share, particularly in the digital and retail banking spaces. This rivalry compels public sector banks to accelerate their own innovation efforts.

Foreign Banks

Foreign banks in India, though fewer in number, significantly intensify competition by targeting high-value corporate clients and affluent retail segments. They introduce global best practices and sophisticated financial products, pushing domestic players like Central Bank of India to enhance their service quality and product offerings. For instance, by mid-2024, foreign banks held approximately 2.5% of India's total banking assets, yet their impact on specialized services and cross-border transactions is disproportionately high.

Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) present a significant competitive rivalry for traditional banks like the Central Bank of India. NBFCs often excel in providing specialized lending and financial services, frequently demonstrating more agility and quicker processing times compared to banks. This allows them to effectively compete for market share in areas such as unsecured retail loans, microfinance, and vehicle financing, particularly by catering to niche segments with tailored offerings.

The competitive landscape is further shaped by regulatory actions. For instance, the Reserve Bank of India (RBI) has implemented increased risk weights on lending to NBFCs, signaling a heightened level of regulatory attention and potentially impacting their funding costs and competitive positioning. This move underscores the dynamic nature of the financial sector and the ongoing interplay between banks, NBFCs, and regulatory bodies.

- NBFCs' Competitive Strengths: Offer specialized services, greater flexibility, and faster turnaround times than traditional banks.

- Key Competitive Segments: Direct competition with banks in unsecured retail loans, microfinance, and vehicle finance.

- Regulatory Impact: RBI's increased risk weights on lending to NBFCs reflect regulatory scrutiny.

- Market Share Capture: NBFCs pose a threat by capturing market share in specific financial niches.

Emergence of Fintech Companies and Payment Banks

The Indian fintech sector is experiencing explosive growth, with payment banks, digital wallets, and P2P lending platforms emerging as significant disruptors. These agile players are leveraging technology to deliver innovative, cost-effective, and user-friendly financial services. For instance, by the end of 2023, India had over 1.5 billion internet subscribers, fueling the digital transformation of financial services.

These fintech companies directly challenge the traditional banking model, particularly in areas like payments, small-ticket lending, and digital transaction processing. For example, Unified Payments Interface (UPI) transactions in India reached an astounding 121 billion in the fiscal year 2023-24, a testament to the shift towards digital payments, often facilitated by fintech platforms.

Central Bank of India is actively responding to this competitive pressure by bolstering its own digital banking capabilities. This includes investing in mobile banking applications, enhancing online account opening processes, and exploring partnerships with fintech firms to integrate new services. The bank aims to retain its customer base and attract new segments by offering competitive digital alternatives.

- Fintech Growth: India's digital payment market is projected to reach $1 trillion by 2026.

- UPI Dominance: UPI transactions processed over ₹182 lakh crore (approximately $2.2 trillion) in FY24.

- Customer Adoption: Over 70% of Indian bank customers now use digital channels for their banking needs.

- Competitive Response: Central Bank of India is focusing on enhancing its mobile banking app and online services to compete with fintech offerings.

India's Banking Sector: Intense Rivalry and Fintech Impact

Competitive rivalry within India's banking sector is intense, impacting Central Bank of India significantly. Public sector banks, private players like HDFC Bank, and foreign institutions all vie for market share, pushing for innovation and better customer service. Fintech firms are also major disruptors, especially in digital payments, with UPI transactions alone reaching 121 billion in FY24, highlighting a rapid shift in customer behavior.

| Competitor Type | Key Characteristics | Impact on Central Bank of India |

|---|---|---|

| Public Sector Banks (PSBs) | Similar product suites, focus on financial inclusion | Direct competition for deposits and loans |

| Private Sector Banks | Agility, technology investment, customer experience focus | Pressure to innovate, potential loss of market share in retail/digital |

| Foreign Banks | Target high-value clients, global best practices | Drives service quality enhancement, competition in specialized segments |

| NBFCs | Agility, specialized lending, faster processing | Competition in retail loans, microfinance, vehicle finance |

| Fintech Companies | Digital innovation, cost-effectiveness, user-friendly services | Disruption in payments, small-ticket lending; necessitates digital investment |

SSubstitutes Threaten

Digital Payment Platforms and Wallets

Digital payment platforms and mobile wallets, such as those built on India's Unified Payments Interface (UPI), present a significant threat of substitution for traditional banking services. These platforms offer unparalleled convenience and speed for everyday transactions, directly competing with bank transfers and card payments.

The widespread adoption of UPI in India is a prime example, with transaction volumes soaring. For instance, UPI transactions crossed the 100 billion mark in 2023, demonstrating a clear shift in consumer behavior away from traditional banking channels for many payment needs.

This substitution erodes the transaction-based revenue streams for banks, as customers increasingly opt for these agile, often fee-free, digital alternatives for their daily financial activities.

Mutual Funds, Equities, and Other Investment Avenues

Mutual funds, direct equity, and insurance products are significant substitutes for traditional bank deposits. These alternatives can attract customer savings if they offer superior returns, potentially reducing the Central Bank of India's deposit base and increasing its funding costs. For instance, in 2023, Indian equity mutual funds saw substantial inflows, demonstrating a clear shift in investor preference towards market-linked instruments over fixed deposits.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-peer (P2P) lending platforms represent a significant threat of substitutes for the Central Bank of India. These platforms directly link borrowers with individual lenders, often for personal loans and small business financing, effectively sidestepping traditional banking channels. This disintermediation offers an alternative for credit seekers and investors alike, directly impacting the bank's core lending operations.

Chit Funds and Unorganized Money Lenders

In certain rural and semi-urban regions of India, informal financial avenues like chit funds and unorganized money lenders persist as viable substitutes for credit, especially for smaller financial needs. These channels, though often lacking regulation and carrying higher risks, provide rapid access to funds, bypassing the extensive documentation typically required by formal institutions. This is particularly relevant for individuals and small businesses underserved by traditional banking services.

The existence of these informal lenders presents a competitive threat to Central Bank of India, as they cater to a segment that may find formal banking processes cumbersome. For instance, Reserve Bank of India data often highlights the continued prevalence of informal credit in rural economies, where accessibility and speed are paramount. In 2023, while formal credit penetration increased, informal channels remained significant for micro-borrowing.

- Informal Credit Prevalence: Chit funds and unorganized lenders offer quick, albeit risky, alternatives for small-scale credit in rural and semi-urban India.

- Accessibility Advantage: These informal channels bypass stringent documentation, appealing to those underserved by formal banking.

- Competitive Threat: Their speed and ease of access can draw customers away from traditional banks like Central Bank of India.

- Regulatory Gap: The lack of regulation in informal sectors creates a riskier but often more convenient environment for borrowers.

Direct Lending by Large Corporates

Large corporations with robust financial health increasingly bypass traditional banking channels by offering direct lending to their business networks, such as suppliers and distributors. For instance, in 2024, several major manufacturing firms announced programs to provide working capital directly to their key suppliers, aiming to secure supply chains and potentially achieve better pricing. This trend allows these corporations to manage their capital more efficiently and reduce their dependence on external financing.

Furthermore, these large entities can tap into capital markets by issuing commercial paper, a short-term debt instrument. In the first half of 2024, corporate bond issuance by non-financial companies saw a notable uptick, reflecting a preference for direct market access over bank loans for immediate funding needs. This capability directly substitutes for the corporate lending services typically provided by banks like the Central Bank of India, thereby impacting the bank's potential for growth in its corporate loan portfolio.

- Direct Lending Programs: Major corporations are establishing internal financing arms or direct lending initiatives for their supply chains.

- Commercial Paper Issuance: Companies are increasingly using the commercial paper market for short-term funding needs.

- Market Access: Strong balance sheets enable large corporates to access capital markets directly, bypassing traditional bank intermediation.

- Impact on Banks: This reduces the demand for corporate loans from financial institutions, potentially limiting loan book expansion.

Multifaceted Substitutes Challenge Traditional Banking Services

The threat of substitutes for Central Bank of India is multifaceted, encompassing digital payment innovations, alternative investment vehicles, and informal financial channels. These substitutes directly compete with traditional banking services by offering greater convenience, higher potential returns, or easier access to credit.

Digital payment platforms like UPI are rapidly capturing transaction market share from banks, as evidenced by UPI's transaction volume exceeding 100 billion in 2023. Similarly, mutual funds saw substantial inflows in 2023, indicating a shift from bank deposits to market-linked investments. Peer-to-peer lending platforms also offer direct competition for credit seekers, bypassing traditional intermediaries.

| Substitute Type | Example | Key Impact | 2023/2024 Data Point |

| Digital Payments | UPI | Erodes transaction revenue | UPI transactions crossed 100 billion in 2023 |

| Alternative Investments | Mutual Funds | Reduces deposit base, increases funding costs | Substantial inflows into Indian equity mutual funds in 2023 |

| Direct Lending | P2P Platforms | Disintermediates core lending operations | Growing P2P lending market in India |

| Informal Finance | Chit Funds, Unorganized Lenders | Captures underserved segments | Continued prevalence of informal credit in rural economies (RBI data) |

| Corporate Finance | Commercial Paper, Direct Lending | Reduces demand for corporate loans | Uptick in corporate bond issuance by non-financial companies in H1 2024 |

Entrants Threaten

New Banking Licenses (Small Finance Banks, Payment Banks)

The Reserve Bank of India's issuance of new licenses for Small Finance Banks and Payment Banks presents a significant threat of new entrants for established players like the Central Bank of India. These new entities, often digitally focused and targeting specific market segments, can rapidly capture market share. For instance, NSDL Payments Bank Limited's recent inclusion in the RBI's Second Schedule highlights the growing presence of these specialized banks.

Fintech Startups and Neo-banks

The Indian fintech landscape is a hotbed of innovation, fueled by substantial investment and robust digital infrastructure like the Unified Payments Interface (UPI). This environment significantly lowers the barrier to entry for new fintech startups and neo-banks. These agile players, often boasting lean operations and a focus on digital-first customer experiences, can quickly challenge established players.

These new entrants are a considerable threat to traditional banks like the Central Bank of India. Their ability to offer specialized, technology-driven services at lower costs, coupled with a seamless digital user journey, can attract a significant customer base. India's fintech adoption rate, which consistently outpaces global averages, underscores the market's receptiveness to these disruptive models.

Large Non-Financial Corporations Entering Financial Services

Large non-financial corporations, particularly those with vast customer networks and advanced digital infrastructure like telecom and e-commerce giants, pose a significant threat by entering the financial services arena. Jio Financial Services exemplifies this trend, launching its comprehensive super app in 2024, which includes digital banking and UPI transaction capabilities.

These entrants leverage substantial financial resources, established customer loyalty, and cutting-edge technology to rapidly gain market share and potentially disrupt traditional banking models. Their ability to integrate financial services into existing ecosystems offers a compelling value proposition to consumers.

Regulatory Changes Promoting New Entry

The Reserve Bank of India's (RBI) evolving regulatory landscape is actively working to boost competition and financial inclusion, which can significantly reduce the hurdles for new businesses entering the financial sector. This proactive approach is designed to make it easier for innovative companies to establish themselves.

Policies such as Open Banking and the establishment of regulatory sandboxes are crucial in this regard. They provide a controlled environment for testing new financial models and services, thereby encouraging innovation and paving the way for a greater number of new entrants across various financial service domains.

A key element of this evolving framework is the proposed Unified Fintech Licensing, a central feature within the Draft Indian Fintech Regulation Bill. This aims to streamline the licensing process for fintech companies.

- RBI's focus on financial inclusion and competition

- Open Banking and regulatory sandboxes fostering innovation

- Unified Fintech Licensing as a key regulatory initiative

Global Players Entering the Indian Market

The Indian financial services sector is increasingly attractive to global players. As India's economy continues its robust growth trajectory, projected to expand by 6.5% in FY2024-25 according to the Reserve Bank of India, international banks and fintech firms are eyeing opportunities. This influx of foreign capital and advanced technological capabilities, especially in areas like blockchain innovation where India is a leader, poses a significant threat of increased competition for established domestic institutions like the Central Bank of India.

Global financial institutions bring substantial capital reserves and proven expertise in digital banking solutions. For instance, foreign direct investment (FDI) in the Indian banking sector has seen consistent inflows, indicating strong international interest. This can lead to intensified competition, particularly in niche segments and digital offerings, where new entrants can leverage their global experience to capture market share.

- Growing Indian Economy: India's GDP growth forecast of 6.5% for FY2024-25 signals a fertile ground for financial services.

- Digital Adoption: Rising smartphone penetration and internet usage create avenues for digital-first global players.

- FDI Inflows: Significant foreign direct investment in the banking sector highlights the attractiveness of the Indian market.

- Technological Advancements: Global firms' expertise in areas like blockchain can disrupt traditional banking models.

New Entrants Intensify Competition in Indian Banking

The threat of new entrants for the Central Bank of India is substantial, driven by regulatory shifts and technological advancements. The Reserve Bank of India's (RBI) push for financial inclusion and competition, exemplified by the issuance of new licenses for Small Finance Banks and Payment Banks, lowers barriers to entry. India's rapidly growing fintech sector, supported by initiatives like UPI, fosters agile startups that challenge traditional players with digital-first offerings and lower costs. Furthermore, large non-financial corporations, such as Jio Financial Services, are entering the market with integrated digital ecosystems, leveraging existing customer bases and significant capital.

| New Entrant Type | Key Characteristics | Impact on Central Bank of India | Example |

|---|---|---|---|

| Small Finance Banks/Payment Banks | Digitally focused, niche targeting | Market share erosion, increased competition in specific segments | NSDL Payments Bank Limited |

| Fintech Startups/Neo-banks | Agile, lean operations, digital-first customer experience | Disruption of traditional services, customer acquisition | Various UPI-enabled payment apps |

| Non-Financial Corporations | Leverage existing customer networks, vast resources, integrated ecosystems | Significant market disruption, cross-selling opportunities | Jio Financial Services (launched comprehensive super app in 2024) |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the Central Bank of India leverages data from the Reserve Bank of India's official publications, annual reports, and economic surveys. We also incorporate insights from reputable financial news outlets and industry analysis reports to provide a comprehensive view of the competitive landscape.