Boston Beer Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Boston Beer Bundle

Go Beyond the Preview—Access the Full Strategic Report

Boston Beer faces moderate buyer power as consumers have choices, but brand loyalty can mitigate this. The threat of new entrants is significant due to relatively low barriers to entry in craft brewing, demanding constant innovation. Understanding these forces is crucial for navigating the competitive landscape.

The complete report reveals the real forces shaping Boston Beer’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentrated Raw Material Supply

The Boston Beer Company faces a significant challenge with its concentrated raw material supply, particularly for malt. In 2024, the company relied on just four primary malt suppliers. This limited supplier base grants these key players considerable leverage, allowing them to potentially influence pricing and terms.

This reliance on a small number of suppliers creates vulnerabilities for Boston Beer. Issues like crop quality fluctuations or unexpected supply chain disruptions from even one of these four suppliers could directly impact production schedules and increase operational costs. Managing these relationships and ensuring consistent, high-quality malt is therefore crucial for maintaining profitability and market stability.

Specialized Hop Varieties

Boston Beer Company's reliance on specialized hop varieties, such as those sourced from Europe and other global regions for its Samuel Adams brand, can significantly influence supplier bargaining power. These unique hops, often grown in specific climates and requiring particular cultivation methods, are not easily substituted.

The limited geographic availability and the proprietary nature of certain hop strains mean that suppliers of these key ingredients can command higher prices and dictate terms. For instance, in 2024, the global hop market experienced fluctuations due to weather patterns impacting yields in key growing regions, potentially amplifying the leverage of suppliers with consistent, high-quality harvests of sought-after varieties.

Single-Sourced Flavorings and Fruit Juices

For popular brands like Truly Hard Seltzer and Twisted Tea, the reliance on single-sourced, proprietary flavorings and fruit juices significantly strengthens the bargaining power of those specific suppliers. This dependence means Boston Beer is more susceptible to potential price hikes or disruptions in the supply of these crucial ingredients. In 2023, the beverage industry saw ingredient costs, particularly for specialty fruits and natural flavorings, increase by an average of 5-10% due to various global supply chain pressures.

Reliance on Third-Party Production Contracts

Boston Beer's reliance on third-party production, particularly with City Brewing Company, which handled 26% of its domestic shipments in 2024, highlights supplier leverage. This dependence is further underscored by upfront payments for facility upgrades and potential shortfall fees for unmet volume commitments, demonstrating a tangible impact of these contractual relationships on Boston Beer's operational flexibility and costs.

The company's engagement with contract brewers like Rauch North America Inc. also contributes to the bargaining power of suppliers. These arrangements mean that Boston Beer doesn't own all its production capacity, giving these external partners a degree of control over supply and pricing.

- Third-Party Production Dependence: Boston Beer utilizes external manufacturers for a significant portion of its production.

- Key Supplier: City Brewing Company was responsible for 26% of Boston Beer's domestic shipment volume in 2024.

- Financial Commitments: The company has made advance payments for capital improvements at contract facilities.

- Volume Commitments: Boston Beer faces penalties, such as shortfall fees, if it fails to meet agreed-upon production volumes with its suppliers.

Ongoing Supply Chain Optimization Initiatives

Boston Beer is actively working to lessen the impact of supplier power through ongoing supply chain optimization. This includes a thorough review of existing supplier contracts to build in more flexibility and a sharp focus on achieving cost efficiencies for key inputs like raw materials and packaging.

These strategic initiatives are designed to not only reduce overall procurement expenses but also to bolster the company's resilience against potential supplier leverage. For instance, in 2023, Boston Beer reported cost of goods sold at $1.2 billion, highlighting the importance of managing these supplier relationships effectively.

- Reviewing supplier contracts for enhanced flexibility.

- Focusing on cost efficiencies in raw materials and packaging procurement.

- Aiming to reduce overall procurement expenses.

- Improving resilience against supplier leverage.

Supplier Leverage: Raw Materials and Production Challenges

Boston Beer's bargaining power with suppliers is significantly impacted by its reliance on a few key raw material providers and contract manufacturers. The company's dependence on a limited number of malt suppliers, for example, gives these entities considerable sway over pricing and terms. This situation is further complicated by the need for specialized ingredients like unique hop varieties, which are not easily substituted and are often sourced from specific global regions.

The company's use of third-party production, with City Brewing Company handling 26% of its domestic shipments in 2024, also creates supplier leverage. Boston Beer faces financial commitments, including advance payments for facility upgrades and potential penalties for unmet volume commitments, which directly influence its operational costs and flexibility.

| Supplier Aspect | Impact on Boston Beer | 2024 Data/Context |

|---|---|---|

| Malt Supply Concentration | High supplier bargaining power due to limited options. | Relied on four primary malt suppliers. |

| Specialty Hop Sourcing | Suppliers can command higher prices for unique, non-substitutable varieties. | Global hop market fluctuations due to weather impacted yields. |

| Third-Party Production | Contract manufacturers hold leverage due to production volume. | City Brewing Company handled 26% of domestic shipments. |

| Contractual Financials | Upfront payments and shortfall fees increase costs and reduce flexibility. | Advance payments for facility upgrades were made. |

What is included in the product

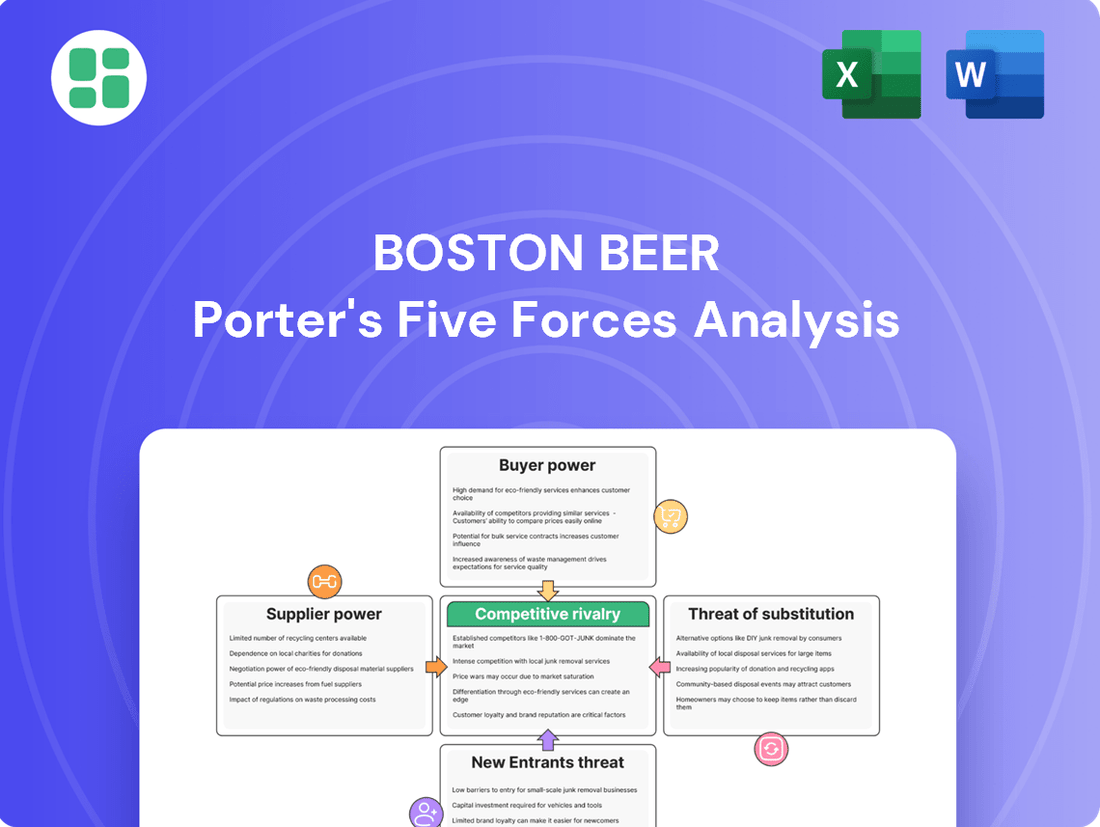

Tailored exclusively for Boston Beer, analyzing its position within its competitive landscape by examining supplier power, buyer bargaining, threat of new entrants, substitutes, and the intensity of rivalry.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces model, allowing for rapid assessment of market dynamics affecting Boston Beer.

Customers Bargaining Power

Three-Tier Distribution System Influence

Boston Beer's reliance on a three-tier distribution system, where independent wholesalers act as intermediaries to retailers, significantly shapes customer bargaining power. These wholesalers and large retail chains, by virtue of the substantial volumes they procure, command considerable influence. This influence directly impacts Boston Beer's pricing strategies, the level of promotional support required, and crucially, the allocation of valuable shelf space in a competitive market.

Shifting Consumer Preferences Towards Moderation

The bargaining power of customers is significantly influenced by shifting consumer preferences towards moderation, especially among younger demographics. Gen Z and Millennials are increasingly embracing 'sober curious' lifestyles and actively seeking out low-calorie, low-sugar, and non-alcoholic beverage choices.

This growing demand for healthier alternatives empowers consumers, giving them greater leverage to pressure companies like Boston Beer to diversify their product offerings. For instance, the non-alcoholic beer market saw substantial growth, with sales increasing by over 20% in 2023 according to some industry reports, demonstrating consumers’ willingness to shift their spending towards these options.

Price Sensitivity and 'Affordable Luxury' Trend

The bargaining power of customers is a significant factor for Boston Beer. While a segment of consumers gravitates towards premiumization, the prevailing economic climate in 2024 has also fueled an 'affordable luxury' trend. This means many customers are looking for high-quality products at more accessible price points, making them more sensitive to pricing strategies, particularly for their widely distributed brands.

This dual consumer behavior forces Boston Beer to carefully calibrate its pricing, ensuring it aligns with the perceived value offered. For instance, while Samuel Adams continues to represent a premium offering, the company must also consider how its broader portfolio, including Truly Hard Seltzer, resonates with value-conscious consumers who might switch to less expensive alternatives if prices rise too sharply. In 2023, the U.S. inflation rate averaged 4.12%, a figure that directly impacts consumer purchasing power and their sensitivity to price changes across all beverage categories.

Availability of Diverse Product Alternatives

The sheer volume of beverage options available significantly amplifies customer bargaining power. Consumers can readily select from a vast spectrum of alcoholic and non-alcoholic drinks, including the rapidly expanding Ready-to-Drink (RTD) category and a growing non-alcoholic segment.

This abundance of substitutes means customers can easily shift their allegiance to different brands or even entirely different beverage types based on factors like taste preference, price point, or the specific occasion. For instance, by the end of 2023, the global RTD market was valued at over $40 billion and is projected to grow substantially, indicating a strong consumer appetite for alternatives that Boston Beer must contend with.

- Broad Beverage Market: Consumers have access to a wide array of alcoholic and non-alcoholic drinks, including spirits, wine, beer, ciders, and a burgeoning RTD market.

- Growth in RTD and Non-Alcoholic Segments: The Ready-to-Drink sector, along with the increasing popularity of non-alcoholic options, presents direct substitutes for traditional beer and hard seltzer products.

- Consumer Choice and Switching: The availability of numerous alternatives empowers consumers to easily switch brands or categories, pressuring producers like Boston Beer on pricing and product innovation.

Strong Sales Force and Brand Building Efforts

Boston Beer Company’s extensive sales force, one of the largest in the U.S. beer industry, is a key asset. This team actively cultivates relationships with distributors and retailers, ensuring prominent placement and support for their brands. By engaging directly with consumers through educational events and promotions, Boston Beer aims to build brand loyalty and influence purchasing decisions, thereby mitigating the bargaining power of customers.

The company's significant investment in brand building, exemplified by its consistent marketing efforts, further solidifies its market position. This focus on brand equity allows Boston Beer to command premium pricing and reduces customer price sensitivity. For instance, in 2023, Boston Beer continued to invest heavily in marketing and advertising to support its diverse portfolio, including Samuel Adams and Truly Hard Seltzer.

- Sales Force Reach: Boston Beer employs a substantial sales team to manage distributor and retailer relationships across the U.S.

- Brand Loyalty Initiatives: Promotional activities and educational programs are designed to foster deep customer connections.

- Market Influence: Direct engagement aims to sway consumer preferences and purchasing habits.

- Competitive Advantage: A strong sales and marketing infrastructure helps counter customer bargaining power.

Consumer Power: Adapting to Evolving Tastes and Economic Pressures

The bargaining power of customers for Boston Beer is substantial due to the wide array of beverage choices available, including the rapidly growing Ready-to-Drink (RTD) and non-alcoholic segments. Consumers can easily switch to alternatives based on price, taste, or occasion, as evidenced by the global RTD market exceeding $40 billion by the end of 2023. This puts pressure on Boston Beer regarding pricing and product innovation.

Furthermore, evolving consumer preferences, particularly among younger demographics, towards moderation and healthier options empower customers. The non-alcoholic beer market alone saw over 20% growth in 2023, signaling a shift in spending habits. In 2024, an 'affordable luxury' trend also makes consumers more price-sensitive, especially for widely distributed brands, as the 2023 inflation rate averaged 4.12%.

Boston Beer's extensive sales force and significant investments in brand building, including substantial marketing efforts in 2023 for brands like Samuel Adams and Truly Hard Seltzer, are key strategies to mitigate this customer power. These efforts aim to foster brand loyalty and influence purchasing decisions, thereby reducing price sensitivity.

| Factor | Impact on Boston Beer | Supporting Data (2023/2024 Trends) |

|---|---|---|

| Availability of Substitutes | High customer bargaining power; easy switching | Global RTD market > $40 billion (end of 2023) |

| Shifting Consumer Preferences | Increased demand for healthier/non-alcoholic options | Non-alcoholic beer market grew > 20% (2023) |

| Economic Climate | Heightened price sensitivity ('affordable luxury') | U.S. inflation averaged 4.12% (2023) |

| Boston Beer's Mitigation Strategies | Building brand loyalty, influencing purchasing | Continued heavy investment in marketing and sales force |

What You See Is What You Get

Boston Beer Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Boston Beer, detailing the competitive landscape, bargaining power of buyers and suppliers, threat of new entrants and substitutes, and the intensity of rivalry within the craft beer industry. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, offering actionable insights for strategic planning.

Rivalry Among Competitors

Mature and Declining Craft Beer Market

The craft beer market, a vital segment for Boston Beer, is showing signs of maturity. In 2024, the number of breweries closing surpassed new openings, indicating a contraction. This trend highlights an intensely competitive landscape where companies fight for market share, often by taking it from competitors.

Intense Competition from Major Beverage Companies

Boston Beer operates in a highly competitive landscape, facing formidable rivals such as Constellation Brands, Molson Coors Beverage, Anheuser-Busch InBev, Diageo, and Heineken. These major beverage companies leverage substantial marketing resources and extensive distribution channels, creating significant pressure on Boston Beer's market share and profitability.

Rapid Growth and Diversification in RTD and Seltzer Segments

The Ready-to-Drink (RTD) and hard seltzer markets are booming, drawing in a crowd of new players and encouraging existing beverage giants to expand their offerings. Boston Beer's Truly and Twisted Tea brands operate in these dynamic spaces, facing intensified competition due to this rapid expansion and product diversification.

Category Blurring and Cross-Market Competition

The beverage industry is experiencing significant category blurring, with traditional beer, wine, and spirits companies increasingly venturing into new, overlapping segments. This expansion includes a notable push into non-alcoholic beverages and spirits-based ready-to-drink (RTD) options, creating a more complex competitive landscape for Boston Beer.

This trend means Boston Beer doesn't just face rivals in its core beer categories; it now contends with a broader spectrum of beverage manufacturers. For instance, in 2024, the RTD segment, which includes spirits-based offerings, continued its rapid growth, with many established liquor brands launching their own canned cocktails, directly challenging Boston Beer's market share in convenient, pre-mixed alcoholic beverages.

- Category Blurring: Traditional beverage players are entering adjacent markets like non-alcoholic drinks and spirits-based RTDs.

- Expanded Competition: Boston Beer now competes against a wider array of beverage companies, not just direct beer rivals.

- RTD Growth: The spirits-based RTD market, a key area of expansion, saw continued strong performance in 2024, intensifying competition.

- Strategic Implications: This cross-market competition requires Boston Beer to adapt its strategies to a more diversified competitive set.

Economic Headwinds and Shifting Consumer Behavior

Economic uncertainty and evolving consumer preferences, particularly a move towards moderation and seeking better value, are impacting overall industry sales volumes. This less robust market landscape heightens competition as businesses vie for a more limited or stagnant customer base.

This intensified rivalry was evident for Boston Beer, which experienced depletion declines in the second quarter of 2025.

- Economic Headwinds: Broader economic challenges are influencing consumer spending habits within the beverage sector.

- Shifting Consumer Behavior: A notable trend is the increased consumer interest in moderation and value-driven purchases.

- Impact on Rivalry: These factors collectively create a more competitive environment, forcing companies to work harder for sales.

- Boston Beer's Experience: Boston Beer's Q2 2025 depletion declines illustrate the pressure from these market dynamics.

Competitive Pressures Mount in Dynamic Beverage Industry

The competitive rivalry for Boston Beer is intense, fueled by a maturing craft beer market and the burgeoning Ready-to-Drink (RTD) segment. Major beverage conglomerates with vast marketing budgets and distribution networks, such as Constellation Brands and Anheuser-Busch InBev, are significant rivals. The industry is also seeing increased category blurring, with traditional alcohol producers entering non-alcoholic and spirits-based RTD markets, directly challenging Boston Beer's product lines like Truly and Twisted Tea. This dynamic environment was underscored by Boston Beer's depletion declines in Q2 2025, reflecting the pressure from these multifaceted competitive forces.

| Competitor | Key Brands | Competitive Actions/Impact |

|---|---|---|

| Constellation Brands | Corona, Modelo, Robert Mondavi | Strong presence in beer and wine; expanding RTD offerings. |

| Molson Coors Beverage | Coors Light, Miller Lite, Blue Moon | Focus on core brands and innovation in seltzer and RTD. |

| Anheuser-Busch InBev | Budweiser, Stella Artois, Michelob Ultra | Dominant market share; aggressive marketing and portfolio expansion. |

| Diageo | Smirnoff, Captain Morgan, Don Julio | Leading spirits producer, actively entering the RTD space with spirit-based canned cocktails. |

| Heineken | Heineken, Tecate, Dos Equis | Global reach; investing in premiumization and diversification. |

SSubstitutes Threaten

Booming Non-Alcoholic Beverage Market

The burgeoning non-alcoholic beverage market poses a considerable threat to traditional alcohol producers like Boston Beer. This segment, encompassing non-alcoholic beers, spirits, and mocktails, is experiencing rapid growth. In 2023, the global non-alcoholic beverage market was valued at over $900 billion, with projections indicating continued expansion, driven by increasing consumer interest in health and wellness, as well as the growing sober curious movement.

Growth of Other Alcoholic Categories

Beyond traditional beer, categories like wine and spirits, especially agave-based spirits such as tequila and mezcal, are experiencing robust growth. For instance, the global tequila market was valued at approximately $13.2 billion in 2023 and is projected to reach over $25 billion by 2030. This expansion signifies a significant shift in consumer preferences.

These diverse alternatives offer distinct taste profiles and consumption experiences, effectively capturing consumer attention and siphoning market share away from beer and hard seltzers. This trend presents a clear threat of substitution for Boston Beer.

Ready-to-Drink (RTD) Cocktails and Flavored Malt Beverages

The threat of substitutes for Boston Beer is significant, particularly from the rapidly growing Ready-to-Drink (RTD) cocktail and flavored malt beverage (FMB) sectors. While Boston Beer has a strong presence with Truly and Twisted Tea, the overall RTD market is diversifying with spirits-based options and a wide array of other FMBs. These alternatives offer consumers similar convenience and flavor profiles, directly competing for market share.

In 2024, the RTD segment continued its upward trajectory, with many analysts projecting double-digit growth. For instance, the spirits-based RTD category alone was expected to see substantial expansion, driven by consumer demand for pre-mixed, high-quality cocktails. This broadens the competitive landscape beyond traditional beer and even Boston Beer's current FMB offerings, presenting a clear substitute threat.

Impact of Health and Wellness Trends

The increasing focus on health and wellness presents a significant threat of substitutes for Boston Beer. As consumers prioritize healthier lifestyles, there's a potential for reduced consumption of traditional alcoholic beverages. This trend is further amplified by the growing popularity of weight-loss drugs, which could lead to a general decrease in overall food and beverage intake, impacting alcohol sales. For instance, by late 2024, the widespread adoption of these medications could reshape consumer spending habits across the entire food and beverage sector.

This macro shift represents a long-term substitution threat as it fundamentally alters consumer preferences and behaviors. Instead of choosing beer, consumers might opt for non-alcoholic alternatives, healthier beverage choices, or simply reduce their overall consumption. This could manifest in several ways:

- Shift to Non-Alcoholic Beverages: Increased demand for sparkling water, kombucha, and low-calorie alternatives.

- Reduced Overall Consumption: Health-conscious individuals may limit intake of all caloric beverages.

- Focus on "Better-for-You" Options: Even within alcoholic beverages, a preference for lower-alcohol or naturally flavored options could emerge.

Emergence of Alternative Recreational Substances

The growing legalization and social acceptance of recreational marijuana across numerous U.S. states present a significant substitute threat to alcoholic beverages. Consumers looking for alternative recreational experiences may choose cannabis products over traditional alcohol, potentially impacting demand within the entire beverage alcohol sector.

This shift is already showing tangible effects. For instance, in states where recreational marijuana is legal, some studies suggest a correlation with a slight dip in beer and spirits sales. In 2023, the U.S. legal cannabis market was estimated to be worth over $30 billion, indicating a substantial consumer spend that could otherwise go towards alcoholic beverages.

- Market Penetration: As more states legalize, the reach of cannabis as a substitute grows.

- Consumer Preference Shift: Younger demographics, in particular, are showing an increasing openness to cannabis as a recreational choice.

- Economic Impact: The diversion of consumer spending from alcohol to cannabis represents a direct revenue threat.

Diverse Substitutes Reshape the Beverage Landscape

The threat of substitutes for Boston Beer is multifaceted, extending beyond traditional alcoholic beverages. Non-alcoholic options, particularly in the burgeoning sober curious movement, are gaining significant traction. The global non-alcoholic beverage market exceeded $900 billion in 2023, showcasing a substantial alternative for consumers seeking healthier choices.

Furthermore, the Ready-to-Drink (RTD) cocktail and flavored malt beverage (FMB) sectors, including spirits-based RTDs, present a direct competitive challenge. The RTD market, projected for double-digit growth in 2024, offers convenience and diverse flavor profiles that appeal to consumers, directly impacting Boston Beer's core offerings like Truly and Twisted Tea.

The increasing focus on health and wellness, potentially amplified by the widespread adoption of weight-loss drugs by late 2024, could lead to reduced overall consumption of caloric beverages, including alcohol. This macro trend encourages a shift towards non-alcoholic alternatives or a general moderation in drinking habits.

The growing acceptance and legalization of recreational marijuana also represent a significant substitute. In 2023, the U.S. legal cannabis market was valued at over $30 billion, indicating a substantial consumer spend that could divert from alcoholic beverage purchases.

Entrants Threaten

High Capital Requirements

The alcoholic beverage industry, especially for craft and specialty beers like those produced by Boston Beer, demands significant upfront capital. Setting up state-of-the-art brewing facilities, acquiring advanced bottling and canning lines, and building a robust distribution network can easily run into tens or even hundreds of millions of dollars. For instance, a new large-scale craft brewery might require $50 million to $100 million in initial investment.

This high capital requirement acts as a formidable barrier to entry. Potential competitors are often dissuaded by the sheer financial commitment needed to even begin operations at a scale that could challenge established players like Boston Beer. Furthermore, substantial marketing budgets are essential to build brand awareness and secure shelf space in a crowded market, adding another layer of financial challenge.

Complex Regulatory Landscape and Licensing

The alcoholic beverage sector is a minefield of regulations, demanding extensive federal, state, and local licenses for every step from brewing to selling. For instance, in 2024, obtaining a federal Alcohol and Tobacco Tax and Trade Bureau (TTB) permit alone can take several months and involve significant paperwork and fees, acting as a substantial hurdle for aspiring brewers.

This complex and costly web of compliance, including varying state-specific franchise laws and direct shipping restrictions, significantly raises the barrier to entry. Newcomers must invest heavily in legal counsel and administrative resources just to get operational, a cost that can easily deter smaller, less capitalized ventures from even attempting to enter the market.

Established Distribution Network Challenges

Boston Beer Company's reliance on a robust, three-tier distribution system presents a significant barrier for new entrants. This established network, deeply entrenched with independent wholesalers and retailers, is not easily replicated or penetrated by emerging craft breweries aiming to gain market access.

Securing shelf space in a crowded market, especially against established brands like Samuel Adams, is a formidable challenge. New players must overcome the inertia of existing relationships and demonstrate substantial value to distributors and retailers, a process that often requires considerable time and capital investment, hindering rapid market entry.

Strong Brand Loyalty and Brand Equity

Boston Beer Company benefits from robust brand loyalty, particularly for its flagship Samuel Adams brand, alongside its popular Truly and Twisted Tea offerings. This strong brand equity, cultivated over years of marketing and product development, presents a significant barrier to entry.

New competitors must invest heavily in marketing and product innovation to even begin to rival Boston Beer's established market presence and consumer trust. For instance, in 2023, Boston Beer's net revenue was approximately $2.04 billion, underscoring the scale of operations and investment required to compete effectively.

- Brand Recognition: Established brands like Samuel Adams have decades of history and widespread consumer awareness.

- Marketing Investment: Boston Beer's significant marketing spend, which contributed to its 2023 net revenue, is a hurdle for new players.

- Consumer Trust: Years of consistent quality and brand messaging build a level of trust that new entrants must earn.

- Market Share Challenge: Capturing even a small percentage of the craft beer and hard seltzer market requires substantial resources and a compelling value proposition.

Industry Maturation and Consolidation

The craft beer industry is exhibiting signs of maturation, with a noticeable slowdown in new brewery launches and a rise in closures during 2024. This shift indicates a less welcoming environment for aspiring entrants.

This trend points towards increased consolidation as existing market pressures, such as intense competition and evolving consumer preferences, make it more challenging for new breweries to establish a foothold. For instance, reports from the Brewers Association in early 2024 highlighted a plateauing growth rate for craft beer production.

- Maturing Market: Craft beer growth rates have moderated, impacting the attractiveness for new entrants.

- Increased Closures: More breweries are ceasing operations in 2024, signaling a tougher competitive landscape.

- Consolidation Expected: The industry is likely to see more mergers and acquisitions rather than significant new player emergence.

- Barriers to Entry: Established brands, distribution networks, and capital requirements pose substantial hurdles for newcomers.

Cracking the Craft Beer Market: A Tough Brew for Newcomers

The threat of new entrants for Boston Beer Company is relatively low, primarily due to the substantial capital required to establish brewing operations and distribution networks. Significant investment in marketing is also crucial to build brand recognition against established players. For instance, Boston Beer's 2023 net revenue of approximately $2.04 billion highlights the scale of resources needed to compete effectively.

Regulatory hurdles, including obtaining federal and state licenses, add another layer of complexity and cost, potentially delaying or deterring new entrants. The established three-tier distribution system also presents a challenge for newcomers seeking market access. Furthermore, the craft beer market, while growing, is maturing, with reports in early 2024 indicating a plateauing growth rate and an increase in brewery closures, making entry less attractive.

| Barrier to Entry | Impact on New Entrants | Example/Data Point |

|---|---|---|

| Capital Requirements | High upfront costs for facilities and distribution | New craft brewery startup costs can range from $50M-$100M |

| Regulatory Compliance | Complex licensing and varying state laws | Federal TTB permit process can take months in 2024 |

| Brand Loyalty & Marketing | Need for significant investment to build awareness | Boston Beer's 2023 net revenue: ~$2.04 billion |

| Distribution Network | Difficulty penetrating established channels | Reliance on existing wholesaler and retailer relationships |

| Market Maturation | Slowing growth and increasing closures | Brewers Association data shows moderated craft beer growth in early 2024 |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Boston Beer leverages data from company annual reports, SEC filings, and industry-specific market research reports to understand competitive dynamics.