BlueFocus Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

BlueFocus Bundle

From Overview to Strategy Blueprint

BlueFocus operates in a dynamic market, facing significant pressures from rivals and the constant threat of new entrants. Understanding the subtle interplay of buyer power and supplier leverage is crucial for navigating its competitive landscape.

The complete report reveals the real forces shaping BlueFocus’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

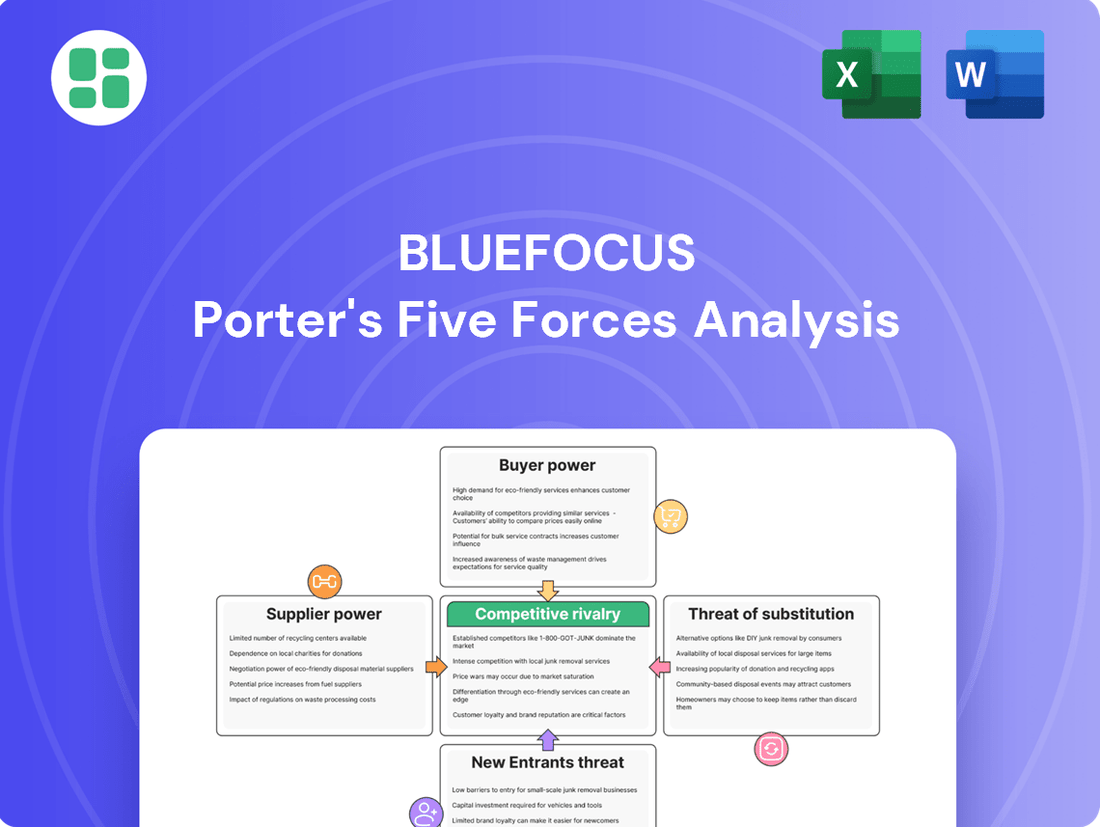

Suppliers Bargaining Power

Specialized Talent

The marketing and communications sector, including firms like BlueFocus, thrives on specialized talent. Think of creative directors, data scientists, and digital strategists. These aren't just any employees; they possess unique skills crucial for campaign success.

The availability of these professionals, particularly in cutting-edge fields like AI in marketing or intricate global brand management, is often limited. This scarcity directly translates to increased bargaining power for these skilled individuals. They can command higher salaries and better benefits, driving up recruitment and retention costs for companies.

For instance, in 2024, the demand for AI and machine learning specialists in marketing roles saw a significant surge, with reported salary increases of up to 20% in some specialized areas. This highlights the leverage these individuals hold, impacting the operational expenses and competitive edge of agencies.

Technology Providers

BlueFocus’s reliance on specialized technology for marketing automation and data analytics means software vendors hold significant sway. If these providers offer unique, hard-to-replicate solutions, they can command higher prices and dictate terms, impacting BlueFocus's operational costs and innovation pipeline.

Media Channels and Publishers

BlueFocus, as a media buying agency, relies heavily on a diverse range of media channels. The bargaining power of suppliers in this sector is significant; for instance, major digital platforms like Google and Meta can dictate advertising rates due to their vast user bases. In 2023, global digital ad spending reached an estimated $603.9 billion, highlighting the dominance of these platforms.

When a few media outlets control a substantial portion of a specific audience or possess unique reach, they gain considerable leverage. This power allows them to set higher advertising rates and more stringent terms, directly affecting BlueFocus's campaign costs and profitability. For example, premium placements on highly sought-after television programs or popular websites can command premium pricing.

Data Providers

Data providers wield considerable influence over BlueFocus, especially as the marketing landscape increasingly relies on detailed consumer insights. Companies that supply unique or hard-to-replicate datasets, such as specialized market research or granular demographic information, can command higher prices or dictate terms. This is particularly relevant in 2024, where the demand for precise audience targeting is at an all-time high.

- High Demand for Data: The global big data and business analytics market was projected to reach $342.13 billion in 2024, highlighting the critical need for data across industries.

- Data Differentiation: Suppliers offering proprietary or exclusive data sources have a stronger bargaining position.

- Switching Costs: The effort and cost involved in finding and integrating alternative data sources can lock BlueFocus into existing supplier relationships.

- Supplier Concentration: If only a few reliable data providers exist, their collective bargaining power increases significantly.

Freelancers and Contractors

The marketing industry heavily utilizes freelancers and contractors, a trend amplified by the growing gig economy. Agencies like BlueFocus often depend on this flexible talent pool for specialized skills in design, content creation, and strategic consulting. This reliance, however, can shift power towards these independent professionals.

Highly skilled and in-demand freelancers, particularly those with niche expertise or a proven track record of successful projects, can significantly influence pricing. Their ability to command premium rates directly impacts the profitability and budget management of agencies that engage their services. For instance, a surge in demand for AI-enhanced content creation specialists in 2024 might see these professionals dictating higher project fees.

- Prevalence of Gig Economy: The marketing sector, including agencies like BlueFocus, increasingly relies on project-based freelance talent.

- Talent Specialization: Niche skills and strong portfolios empower freelancers to negotiate higher rates.

- Impact on Profitability: Premium pricing by sought-after freelancers can squeeze profit margins for agencies.

- Market Dynamics (2024 Example): Increased demand for specialized skills, such as AI content strategists, can further bolster freelancer bargaining power.

Suppliers' leverage reshapes marketing costs and strategies

Suppliers in the marketing sector, particularly those providing essential technology or specialized data, hold significant bargaining power. This is due to the limited availability of unique solutions and the high demand for data-driven insights. For instance, the global big data and business analytics market was projected to reach $342.13 billion in 2024, underscoring the critical need for data providers.

Major media platforms also exert considerable influence, as seen in the $603.9 billion global digital ad spending in 2023. When a few platforms dominate audience reach, they can dictate advertising rates. Similarly, specialized talent, like AI marketing specialists, saw up to a 20% salary increase in certain areas in 2024, reflecting their leverage.

| Supplier Type | Bargaining Power Factors | Impact on BlueFocus | 2024/2023 Data Point |

|---|---|---|---|

| Technology Vendors | Unique/hard-to-replicate solutions | Higher operational costs, potential innovation delays | N/A (specific vendor terms vary) |

| Data Providers | Proprietary/exclusive data, high demand | Increased data acquisition costs, reliance on specific sources | Big data market projected $342.13B in 2024 |

| Media Platforms | Dominant audience reach, limited alternatives | Higher advertising costs, reduced campaign ROI | Global digital ad spending $603.9B in 2023 |

| Specialized Talent (Freelancers) | Niche skills, high demand, gig economy prevalence | Increased project costs, potential talent acquisition challenges | Up to 20% salary increase for AI marketing specialists in 2024 |

What is included in the product

This analysis dissects the competitive forces impacting BlueFocus, examining the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the public relations industry.

Easily identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Client Size and Industry Concentration

BlueFocus serves a global client base, but the bargaining power of its customers can shift based on their size and the industry they operate in. If a single client accounts for a substantial percentage of BlueFocus's total revenue, that client gains considerable leverage to negotiate better pricing and service terms. For instance, if a major automotive manufacturer, a sector known for its large marketing budgets, significantly increases its spend with BlueFocus, its ability to influence contract conditions grows.

Furthermore, industry concentration plays a role. In sectors where there are few alternative marketing and communications service providers capable of meeting the complex needs of large corporations, BlueFocus might find its customers have less bargaining power. Conversely, in highly fragmented industries with many agencies offering similar services, larger clients can more easily switch providers, thereby increasing their negotiating strength.

Switching Costs for Clients

While marketing agencies strive to build loyalty and integrate services, making it harder for clients to leave, the reality is that switching costs in the marketing services industry are generally moderate. For instance, in 2024, many clients can readily compare proposals and transition to a new agency if they are unhappy with results, pricing, or the strategic direction of their current provider.

This ease of switching gives clients significant leverage. They can effectively negotiate for better terms or explore alternative agencies that might offer a more compelling value proposition, directly impacting an agency's pricing power and client retention strategies.

Information Availability and Price Sensitivity

Clients now readily access agency performance data, industry benchmarks, and pricing through online reviews and reports. This heightened transparency, combined with budget pressures, significantly increases price sensitivity. For instance, in 2024, many companies reported scrutinizing agency fees more closely, with some seeking discounts of up to 15% on their marketing retainers.

In-house Marketing Capabilities

Many large corporations are building robust in-house marketing and communication teams. This trend directly impacts the bargaining power of customers, as they gain a viable alternative to external agencies.

When clients can effectively manage certain marketing functions internally, their leverage increases significantly. They can choose to insource services if the costs or perceived value from external agencies fall short of expectations. For instance, by 2024, a notable percentage of Fortune 500 companies reported having expanded their internal digital marketing capabilities.

- Increased Client Leverage: In-house capabilities empower clients to negotiate better terms with external agencies.

- Cost Sensitivity: Clients can opt for internal execution if agency fees become prohibitive.

- Strategic Control: Developing internal teams allows for greater control over brand messaging and strategy.

- Talent Acquisition: A growing number of businesses are investing in in-house talent, with marketing roles seeing significant growth in demand.

Performance-Based Contracts

The increasing prevalence of performance-based contracts significantly bolsters the bargaining power of BlueFocus's customers. As marketing increasingly focuses on measurable return on investment (ROI), clients gain more leverage by tying agency compensation to tangible outcomes.

When contracts are structured around specific key performance indicators (KPIs) or direct sales results, clients can effectively demand accountability from BlueFocus. This arrangement shifts some of the financial risk onto the agency, empowering clients to negotiate more favorable terms and potentially adjust payments based on the achieved performance levels.

- Performance-Based Contracts: Clients can negotiate contracts where BlueFocus's compensation is directly linked to achieving agreed-upon KPIs, such as lead generation volume or conversion rates.

- Measurable ROI: The emphasis on demonstrable ROI in digital marketing allows clients to scrutinize agency performance and use underperformance as a basis for renegotiation.

- Risk Allocation: By linking payment to results, clients transfer a portion of the performance risk to BlueFocus, strengthening their position in price and service discussions.

- Client Leverage: In 2024, many clients in the digital marketing space, especially larger enterprises, have prioritized agencies that can demonstrate clear, quantifiable impact on their bottom line, giving them significant negotiating power.

Client Leverage Reshapes Marketing Agency Landscape

The bargaining power of BlueFocus's customers is substantial, driven by the ease of switching providers and increased price transparency. Clients in 2024 are actively comparing agency fees, with some seeking discounts up to 15%. Furthermore, the growing trend of companies building in-house marketing teams, as evidenced by expanded internal digital capabilities in many Fortune 500 companies by 2024, directly enhances customer leverage.

| Factor Influencing Customer Bargaining Power | Impact on BlueFocus | Supporting Data/Trend (as of 2024) |

|---|---|---|

| Ease of Switching | Increases client leverage, reduces agency pricing power | Moderate switching costs in marketing services industry; clients can readily compare proposals. |

| Price Transparency & Sensitivity | Drives demand for discounts, intensifies price competition | Clients scrutinize fees more closely; some seek up to 15% discounts on retainers. |

| In-house Capabilities | Provides alternative to external agencies, strengthens negotiation position | Notable percentage of Fortune 500 companies expanded internal digital marketing capabilities by 2024. |

| Performance-Based Contracts | Shifts risk to agency, empowers clients to demand accountability | Clients prioritize agencies demonstrating clear, quantifiable impact on bottom line, linking compensation to KPIs. |

Preview Before You Purchase

BlueFocus Porter's Five Forces Analysis

This preview displays the complete BlueFocus Porter's Five Forces Analysis, offering a comprehensive examination of the competitive landscape. The document you see here is precisely what you will receive immediately after purchase, ensuring no discrepancies or missing information. You can trust that this professionally formatted analysis is ready for your immediate use and strategic decision-making.

Rivalry Among Competitors

High Number of Competitors

The marketing services sector is incredibly crowded, with a vast array of agencies, from small, specialized outfits to massive global corporations. This fragmentation means BlueFocus is up against a wide range of competitors, each vying for market share.

BlueFocus contends with both seasoned industry veterans and nimble startups across its entire service spectrum, including public relations, digital marketing, and advertising. This broad competitive landscape intensifies the pressure to innovate and differentiate.

In 2023, the global advertising and marketing services market was valued at approximately $650 billion, underscoring the sheer scale and competitive intensity of the industry BlueFocus operates within. This massive market size attracts numerous players seeking to capture a piece of the pie.

Service Differentiation and Specialization

While BlueFocus provides a broad suite of integrated marketing services, many rivals carve out distinct niches. For instance, some competitors focus intensely on specialized areas like B2B lead generation, healthcare public relations, or performance-driven digital advertising. This means BlueFocus must clearly communicate what makes its integrated approach superior, highlighting its data analytics, technological advancements, and creative prowess to truly differentiate itself in a highly competitive landscape.

Industry Growth and Market Maturity

The marketing services industry, especially digital marketing, is still expanding, but some areas are starting to mature. This maturity often means more intense competition as companies fight harder for their piece of the market. For instance, global digital ad spending was projected to reach over $600 billion in 2024, indicating a large but increasingly contested space.

Constant innovation is key because technology changes so fast and what customers want keeps shifting. Companies that can't keep up risk falling behind. This pressure to innovate means competitors are always trying to be the first to offer the newest, most effective tools and strategies to stay ahead of the curve.

Client Retention and Churn Rates

Client relationships in the marketing industry are indeed dynamic, with agencies frequently facing client churn. This can stem from clients looking for new ideas, more competitive pricing, or specialized skills they believe are lacking. The relative ease of switching providers intensifies competition, compelling BlueFocus to prioritize delivering outstanding performance and cultivating robust, enduring client relationships to keep churn low.

In 2023, the global marketing and advertising industry saw client retention as a critical factor for agency health. While specific churn rates for individual agencies like BlueFocus are often proprietary, industry averages suggest that client switching is a common occurrence. For instance, a significant percentage of businesses re-evaluate their agency partnerships annually, driven by evolving market demands and the constant search for optimal ROI.

- Industry churn is influenced by client perception of value and agency adaptability.

- BlueFocus must proactively demonstrate ROI and foster deep client engagement to combat attrition.

- The competitive landscape pressures agencies to innovate and offer superior service to retain clients.

Global vs. Local Competition

BlueFocus faces a dual competitive landscape, grappling with both global advertising conglomerates and agile local agencies. International rivals such as WPP, Omnicom, and Publicis boast extensive resources and established global networks, presenting a significant challenge for market share.

However, the competition intensifies further due to the presence of strong local players in every market BlueFocus operates in. These local firms often possess a deeper understanding of regional cultural nuances, consumer behaviors, and regulatory environments, allowing them to tailor their services more effectively. For instance, in 2024, the global advertising market saw continued consolidation among the top holding companies, yet the rise of specialized digital agencies and regional powerhouses in Asia and Europe highlighted the persistent strength of local competition.

- Global Giants: BlueFocus competes with multinational advertising groups like WPP, Omnicom, and Publicis, which command substantial global reach and resources.

- Local Market Expertise: The company must also contend with numerous local agencies that have intimate knowledge of specific regional cultures, consumer preferences, and regulatory frameworks.

- Navigational Complexity: Balancing a consistent global brand message with the need to adapt to diverse local market demands creates significant operational complexity and heightens competitive pressure.

Marketing Services: Battling Global Giants and Niche Players

The competitive rivalry within the marketing services sector is fierce, with BlueFocus facing a crowded marketplace populated by both global giants and specialized local agencies. This intense competition is driven by the industry's significant market size, projected to exceed $600 billion globally for digital ad spending in 2024, and the constant need for innovation due to rapid technological advancements and evolving consumer preferences. Agencies must continually demonstrate value and adapt to client demands to mitigate client churn, which remains a significant factor in the industry.

| Competitor Type | Key Characteristics | Impact on BlueFocus |

|---|---|---|

| Global Conglomerates (e.g., WPP, Omnicom) | Extensive resources, established global networks, broad service offerings. | Significant challenge for market share due to scale and brand recognition. |

| Specialized Agencies | Niche expertise (e.g., B2B lead gen, healthcare PR), agile operations. | Pressure to differentiate integrated services and highlight unique value propositions. |

| Local Agencies | Deep understanding of regional nuances, cultural insights, regulatory knowledge. | Require tailored strategies for local markets, increasing operational complexity. |

SSubstitutes Threaten

In-house Marketing Departments

Companies increasingly build their own marketing, PR, and advertising departments. This trend is fueled by technological advancements that simplify many marketing functions, allowing businesses to manage them internally. For instance, the rise of sophisticated marketing automation platforms and content management systems reduces the need for external expertise in many areas.

This shift towards in-house capabilities offers clients greater control over their brand messaging and campaign execution. Furthermore, it can lead to significant cost efficiencies. By eliminating agency markups and overhead, companies can potentially allocate more resources directly to marketing activities. This internal development represents a substantial substitute for the services traditionally offered by external marketing agencies.

Direct-to-Consumer (DTC) Models

The increasing prevalence of Direct-to-Consumer (DTC) models presents a significant threat of substitutes for traditional advertising and media buying services. Brands are increasingly opting to bypass intermediaries, managing their own customer relationships and marketing efforts. This shift means fewer traditional advertising budgets flowing through agencies.

Many DTC brands now handle their social media management, content creation, and targeted digital advertising in-house. For instance, in 2023, the DTC e-commerce sector continued its robust growth, with many brands investing heavily in their own digital platforms and customer engagement strategies, bypassing traditional agency reliance. This self-sufficiency directly substitutes for the core services many agencies offer.

Automated Marketing Platforms & AI Tools

The rise of advanced marketing automation and AI tools presents a significant threat of substitutes for traditional marketing agencies. Platforms like HubSpot and Mailchimp, along with AI-powered content generators and analytics dashboards, allow businesses to manage campaigns, analyze data, and even create marketing materials in-house.

These self-service solutions are increasingly capable of replicating core agency functions, from programmatic advertising to social media management. For instance, the global marketing automation market was valued at approximately $4.4 billion in 2023 and is projected to grow substantially, indicating a clear shift towards businesses adopting these tools directly.

This trend directly impacts agencies by offering a cost-effective alternative for many services. Businesses can leverage these platforms to reduce their reliance on external expertise, especially for routine tasks, thereby lowering operational costs and increasing internal control over marketing efforts.

Consulting Firms and Tech Integrators

Clients increasingly look beyond traditional marketing agencies, considering management consulting firms for high-level brand strategy and technology integrators for implementing complex marketing technology stacks. These entities offer services that can substitute for BlueFocus's integrated solutions, especially in strategic planning and tech deployment.

For instance, major consulting firms like Accenture and Deloitte have expanded their digital marketing and customer experience capabilities, directly competing for strategic brand transformation projects. In 2024, the global management consulting market was valued at approximately $330 billion, with digital transformation services representing a significant portion of that growth.

- Strategic Brand Consulting: Management consulting firms offer overarching brand strategy, potentially replacing the need for specialized marketing agencies for core brand direction.

- Technology Integration: Tech integrators provide end-to-end solutions for marketing technology, substituting for agencies that offer similar, but perhaps less deeply integrated, tech services.

- Market Shift: The demand for integrated digital transformation services is growing, with consulting firms actively acquiring marketing technology expertise.

User-Generated Content and Influencer Marketing Platforms

The increasing prevalence of user-generated content (UGC) and the burgeoning influencer marketing sector present a significant threat of substitutes for traditional advertising and public relations services offered by agencies like BlueFocus. Brands are increasingly leveraging platforms where consumers create and share content, offering a more organic and often cost-effective way to connect with target demographics. For instance, in 2024, global influencer marketing spending was projected to reach $21.1 billion, demonstrating a substantial shift in marketing budgets away from conventional channels.

These alternative avenues allow brands to bypass traditional media gatekeepers and agency intermediaries. By collaborating directly with influencers or fostering UGC campaigns, companies can achieve authentic engagement and reach audiences that might be less responsive to polished, agency-produced advertisements. This direct engagement model can significantly reduce the perceived need for extensive agency services in content creation and media placement.

The threat is amplified by the perceived authenticity and relatability of UGC and influencer-driven campaigns. Consumers often trust recommendations from peers or trusted influencers more than traditional advertising. This shift means that agencies must adapt by offering more integrated strategies that incorporate these new channels, or risk losing clients to platforms and individuals who can deliver similar or better results at a lower price point.

- User-Generated Content (UGC): Brands can encourage customers to create and share content, building authenticity and trust.

- Influencer Marketing Platforms: Direct collaboration with influencers offers targeted reach and often lower costs than traditional campaigns.

- Cost-Effectiveness: UGC and influencer marketing can provide a more budget-friendly alternative for brands seeking audience engagement.

- Authenticity and Trust: Consumer preference for relatable content from peers or influencers challenges the effectiveness of traditional advertising.

Marketing Evolution: In-House, Automation, & Influencers Disrupt Agencies

The rise of in-house marketing departments, direct-to-consumer (DTC) models, and advanced marketing automation tools all serve as significant substitutes for traditional marketing agencies. Businesses are increasingly capable of managing their own campaigns, content creation, and customer engagement, often at a lower cost and with greater control.

Furthermore, management consulting firms and technology integrators are stepping in to offer strategic brand consulting and complex marketing technology implementation, directly competing for high-level projects. The growing prevalence of user-generated content (UGC) and influencer marketing also provides alternative, often more authentic and cost-effective, channels for brands to reach their audiences, bypassing established agency services.

The global marketing automation market was valued at approximately $4.4 billion in 2023, highlighting the adoption of these self-service tools. In 2024, global influencer marketing spending was projected to reach $21.1 billion, demonstrating a substantial shift in marketing budgets.

| Substitute Type | Key Characteristics | Impact on Agencies | Example Data Point |

| In-house Marketing | Greater control, cost efficiency | Reduced demand for core agency services | Simplified marketing functions via tech |

| DTC Models | Direct customer relationships, bypass intermediaries | Fewer traditional advertising budgets flowing through agencies | Continued robust growth in DTC e-commerce (2023) |

| Marketing Automation/AI | Self-service campaign management, data analysis | Cost-effective alternative for routine tasks | Marketing automation market ~$4.4B (2023) |

| Consulting Firms/Tech Integrators | Strategic brand consulting, tech implementation | Competition for high-level projects | Global management consulting market ~$330B (2024) |

| UGC/Influencer Marketing | Authenticity, peer trust, cost-effectiveness | Challenge to traditional advertising effectiveness | Global influencer marketing spend ~$21.1B (2024 proj.) |

Entrants Threaten

Low Capital Requirements for Digital Agencies

The threat of new entrants in the digital marketing space, particularly for agencies, is amplified by remarkably low capital requirements. Unlike their predecessors in traditional advertising, which demanded substantial investments in brick-and-mortar offices and extensive in-house creative departments, digital agencies can launch with minimal upfront costs. This accessibility is a significant factor in the industry's dynamic nature.

The digital landscape itself facilitates this low barrier to entry. Cloud-based software, readily available online marketing tools, and the ability to tap into a global pool of freelance talent drastically reduce the need for physical infrastructure and large, permanent staff. For instance, a startup can operate effectively with just a laptop and internet connection, making it easier for nimble, new competitors to emerge and challenge established players.

Consider the growth of the digital marketing sector. In 2024, the global digital advertising market was projected to reach over $600 billion, indicating a massive and growing opportunity. This expansion attracts new entrants who can leverage affordable digital tools and flexible talent models to offer competitive services without the overhead of older business models.

Specialization and Niche Markets

New entrants are increasingly carving out success by focusing on specialized areas within the marketing landscape. For instance, firms concentrating on niche services like TikTok marketing or B2B SaaS promotion can rapidly build a client base. In 2024, the digital marketing sector saw continued growth in specialized agencies, with some reporting year-over-year revenue increases exceeding 30% by focusing on hyper-targeted services.

Brand Loyalty and Client Relationships

While BlueFocus benefits from established client relationships and a strong brand, the threat of new entrants remains significant. New players can disrupt this by introducing highly innovative marketing technologies, employing aggressive, competitive pricing, or providing a level of personalized service that surpasses current offerings. The marketing landscape, though relationship-centric, sees clients increasingly open to exploring novel partnerships if they promise a distinct competitive edge.

Talent Acquisition and Retention

The marketing industry, particularly areas like digital marketing and creative services, demands highly specialized skills. Attracting and keeping these talented individuals is a significant hurdle for any new company looking to enter the market. Established firms, such as BlueFocus, often possess a stronger brand recognition and greater financial capacity to offer competitive salaries, benefits, and robust training programs, making it harder for newcomers to poach their key personnel.

However, the landscape isn't entirely stacked against startups. A vibrant company culture, the chance to work on innovative or high-profile projects, and offering more agile or flexible work environments can indeed lure top talent away from larger, more established organizations. For instance, in 2024, reports indicated a growing preference among Gen Z professionals for roles that offer purpose and flexibility, factors startups can often highlight more effectively than traditional corporate structures.

- Talent as a Barrier: The need for specialized skills in areas like AI-driven marketing analytics and creative content generation presents a significant barrier to entry.

- Established Player Advantage: Companies like BlueFocus leverage their reputation and resources to attract and retain top marketing professionals, offering competitive compensation and career growth.

- Startup Appeal: Innovative company cultures, unique project opportunities, and flexible work arrangements can attract talent to new entrants, challenging incumbent advantages.

- Market Trends: In 2024, a significant portion of the workforce, particularly younger generations, prioritized workplace culture and flexibility, creating an avenue for startups to compete for talent.

Regulatory and Data Compliance Challenges

The increasing complexity of data privacy regulations, such as GDPR and CCPA, coupled with evolving advertising standards, presents a substantial barrier for new entrants into the digital marketing landscape. Established firms like BlueFocus have developed the necessary infrastructure and in-house expertise to manage these intricate compliance requirements. For instance, in 2024, the global data privacy management software market was valued at approximately $2.1 billion, indicating the significant investment needed to ensure adherence. New companies may find it challenging and costly to implement the robust systems required to navigate these legal frameworks, potentially hindering their market entry and growth.

These compliance challenges can translate into significant operational costs and potential legal risks for newcomers. Navigating the nuances of cross-border data transfer, consent management, and data breach notification protocols demands specialized knowledge and continuous investment in legal and technical resources. In 2023, fines for GDPR violations alone exceeded €2 billion across the EU, underscoring the financial repercussions of non-compliance. This financial and operational burden makes it difficult for smaller, less-resourced entities to compete effectively with established players who have already integrated these compliance measures into their core operations.

- Regulatory Hurdles: New entrants must contend with a growing web of data privacy laws globally.

- Compliance Costs: Significant investment in legal, technical, and operational resources is required.

- Expertise Gap: Established firms possess the experience to manage complex compliance frameworks.

- Risk of Penalties: Non-compliance can lead to substantial fines and reputational damage.

Digital Marketing: New Entrants Face Talent & Regulatory Hurdles

The threat of new entrants in the digital marketing sector is moderate due to low capital requirements, allowing nimble startups to emerge. However, the need for specialized talent and navigating complex data privacy regulations like GDPR and CCPA present significant barriers. Established firms like BlueFocus leverage their brand, resources, and compliance expertise to retain talent and manage regulatory risks, making it challenging for newcomers to compete effectively.

| Factor | Impact on New Entrants | BlueFocus Advantage |

|---|---|---|

| Capital Requirements | Low, facilitating entry. | Established infrastructure and brand recognition. |

| Talent Acquisition | Challenging due to competition for specialized skills. | Stronger financial capacity for competitive compensation and training. |

| Regulatory Compliance | High costs and complexity for new entrants. | Existing infrastructure and in-house expertise for managing data privacy laws. |

| Market Disruption Potential | Can disrupt through innovation and niche specialization. | Focus on retaining clients through superior service and established relationships. |

Porter's Five Forces Analysis Data Sources

Our BlueFocus Porter's Five Forces analysis leverages insights from company annual reports, investor presentations, and industry-specific market research reports to understand competitive dynamics.