Basler Kantonalbank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Basler Kantonalbank Bundle

Go Beyond the Preview—Access the Full Strategic Report

Basler Kantonalbank navigates a competitive landscape shaped by moderate buyer power and the threat of substitutes, particularly from fintech innovations. The bargaining power of suppliers is relatively low, while the threat of new entrants is also somewhat constrained by regulatory hurdles.

The complete report reveals the real forces shaping Basler Kantonalbank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration

Supplier concentration significantly impacts the banking sector's bargaining power. Basler Kantonalbank, like other banks, depends on specialized IT infrastructure, financial data, and payment networks. If these essential services are dominated by a small number of providers, their ability to dictate terms to Basler Kantonalbank grows substantially, as viable alternatives are scarce.

Switching Costs

High switching costs significantly empower suppliers to Basler Kantonalbank (BKB). The bank faces substantial financial investment and operational disruption when considering changes to its core IT systems or key financial service providers. For instance, the average cost for a large financial institution to migrate its core banking system can range from tens of millions to over a hundred million Swiss Francs, with implementation timelines often stretching across several years.

Uniqueness of Services

Suppliers providing highly unique or proprietary technologies, such as specialized fintech solutions or advanced data analytics platforms, wield significant influence. Basler Kantonalbank's dependence on these distinct inputs inherently limits its leverage in negotiating favorable terms and pricing.

Threat of Forward Integration

While traditional banking suppliers like IT infrastructure providers typically lack the inclination for forward integration, the evolving fintech landscape presents a different scenario. Some specialized fintech firms or data analytics companies could potentially leverage their expertise and customer bases to offer direct financial services, thereby becoming competitors to institutions like Basler Kantonalbank.

This threat of forward integration by suppliers, though less prevalent in traditional banking, can indeed amplify their bargaining power. If a supplier can credibly threaten to enter the banking market themselves, they gain leverage in negotiations over pricing, terms, and service level agreements with Basler Kantonalbank. For instance, a data analytics firm that provides crucial customer insights might consider launching its own targeted lending or wealth management products.

- Potential for Fintech Forward Integration: Fintech and data analytics firms are the primary suppliers capable of forward integration into financial services.

- Increased Supplier Leverage: The credible threat of suppliers becoming direct competitors enhances their bargaining power over Basler Kantonalbank.

- Example: Data Analytics Firms: A data analytics provider could potentially leverage its customer insights to offer competing financial products.

Importance of Supplier Input

The criticality of a supplier's services to Basler Kantonalbank's daily operations directly impacts their power. Essential services like secure transaction processing or regulatory compliance software cannot be easily foregone, giving these suppliers significant influence.

For instance, in 2024, the banking sector continued to rely heavily on specialized IT providers for core banking systems and cybersecurity solutions. A disruption from a key supplier in these areas could halt operations, underscoring the suppliers' leverage.

- High Switching Costs: Changing providers for critical banking infrastructure often involves substantial costs and operational risks, strengthening supplier bargaining power.

- Supplier Concentration: A limited number of providers offering specialized financial technology or data services can dictate terms due to lack of alternatives.

- Essential Inputs: Services directly tied to regulatory compliance or secure data management are non-negotiable for Basler Kantonalbank, increasing supplier influence.

Banking's Supplier Grip: Costs & Fintech Risks

Suppliers hold considerable sway over Basler Kantonalbank (BKB) due to the concentration of providers for essential banking services like IT infrastructure and data. High switching costs, often in the tens of millions of Swiss Francs for core system migrations, further solidify supplier leverage. The threat of fintech firms with unique technologies or data analytics capabilities moving into direct financial services also amplifies their power, as seen with data analytics firms potentially offering competing lending products.

| Factor | Impact on BKB | Supporting Data/Example (2024) |

|---|---|---|

| Supplier Concentration | High leverage for few providers | Limited number of core banking software vendors and cybersecurity specialists |

| Switching Costs | Significant barriers to changing suppliers | Core banking system migration costs can exceed CHF 100 million and take years |

| Uniqueness of Offering | Increased dependence on specialized providers | Proprietary fintech solutions for niche markets |

| Threat of Forward Integration | Potential for suppliers to become competitors | Fintech companies leveraging data analytics to offer direct lending or investment services |

What is included in the product

This Porter's Five Forces analysis for Basler Kantonalbank dissects the competitive intensity and profitability potential within the Swiss banking sector, highlighting the influence of rivals, customer power, and regulatory barriers.

Effortlessly identify and address competitive threats with a visual breakdown of Basler Kantonalbank's industry landscape.

Customers Bargaining Power

Customer Concentration

Basler Kantonalbank's customer base is quite diverse, primarily consisting of private individuals, small and medium-sized enterprises (SMEs), and public institutions located within the Basel region. This broad and typically fragmented customer base means that no single customer, or even a small group of customers, holds significant individual leverage over the bank.

This lack of customer concentration is a key factor that diminishes the collective bargaining power of customers against Basler Kantonalbank. For instance, in 2024, the bank reported a substantial number of retail and corporate clients, with the vast majority of these relationships being relatively small in terms of individual value. This wide distribution of customers prevents any one entity from dictating terms or demanding significantly different pricing or service levels.

Switching Costs for Customers

While not exceptionally high, the effort required for customers to switch banks, such as updating direct debits and transferring investments, does present a moderate switching cost for Basler Kantonalbank. This friction can deter customers from immediately moving to a competitor solely based on minor price variations, offering a degree of customer stickiness.

Information Availability

Customers today have unprecedented access to information, readily comparing banking products and services online and through financial advisors. This transparency allows them to easily evaluate offerings from various institutions, including Basler Kantonalbank, and leverage this knowledge to negotiate for more competitive pricing and better terms.

Price Sensitivity

In the Swiss retail banking sector, particularly for common offerings like savings accounts and mortgages, customers often exhibit significant price sensitivity. This means that even small differences in interest rates or fees can influence their choice of bank. For Basler Kantonalbank, this necessitates a careful calibration of its pricing strategies to remain competitive without compromising its financial health.

The bank needs to strike a delicate balance: offering attractive rates to retain existing clients and draw in new ones, while simultaneously ensuring that these prices support sustainable profitability. This is a constant challenge in a mature market where differentiation on price alone can be difficult.

- Price Sensitivity in Swiss Retail Banking: Customers in Switzerland, especially for straightforward products like savings accounts and mortgages, are highly attuned to price.

- Competitive Pricing Imperative: Basler Kantonalbank must offer competitive rates to maintain market share.

- Profitability vs. Acquisition: The bank faces the challenge of balancing attractive pricing for customer acquisition and retention with the need to achieve profitability.

- Market Maturity Impact: In a mature market, price often becomes a key differentiator, intensifying competitive pressures.

Threat of Backward Integration

For significant corporate or institutional clients, the potential to handle their treasury, financing, or investment operations internally, a form of backward integration, diminishes their dependence on conventional banking services. This capability enhances their leverage when negotiating with Basler Kantonalbank.

This threat is particularly relevant as large corporations may possess the scale and expertise to develop in-house financial management capabilities. For instance, a major multinational corporation might establish its own treasury department to manage foreign exchange, cash flow, and debt issuance, thereby reducing the need for external banking partners.

- Reduced Reliance: Clients can bypass traditional banking functions by bringing them in-house.

- Increased Leverage: The option of backward integration strengthens clients' negotiating position.

- Cost Efficiency: Internal management can sometimes offer cost savings for large entities.

Customer Leverage: Key to Banking Market Dynamics

Basler Kantonalbank benefits from a broad, fragmented customer base, limiting individual customer bargaining power. While switching costs exist, readily available market information and price sensitivity, particularly in retail banking, empower customers to seek better terms. For larger clients, the potential for backward integration into financial services also grants them increased leverage.

| Factor | Impact on Basler Kantonalbank | 2024 Data/Observation |

|---|---|---|

| Customer Concentration | Low (fragmented base) | Majority of clients are retail or SMEs with smaller individual transaction values. |

| Switching Costs | Moderate | Customers face some effort in updating direct debits and transferring accounts. |

| Information Availability | High | Online comparison tools and financial advisors allow easy product evaluation. |

| Price Sensitivity | Significant (especially retail) | Customers are responsive to differences in interest rates and fees for common products. |

| Backward Integration Potential | Moderate (for large corporates) | Large firms may develop in-house treasury functions, reducing reliance on banks. |

Preview Before You Purchase

Basler Kantonalbank Porter's Five Forces Analysis

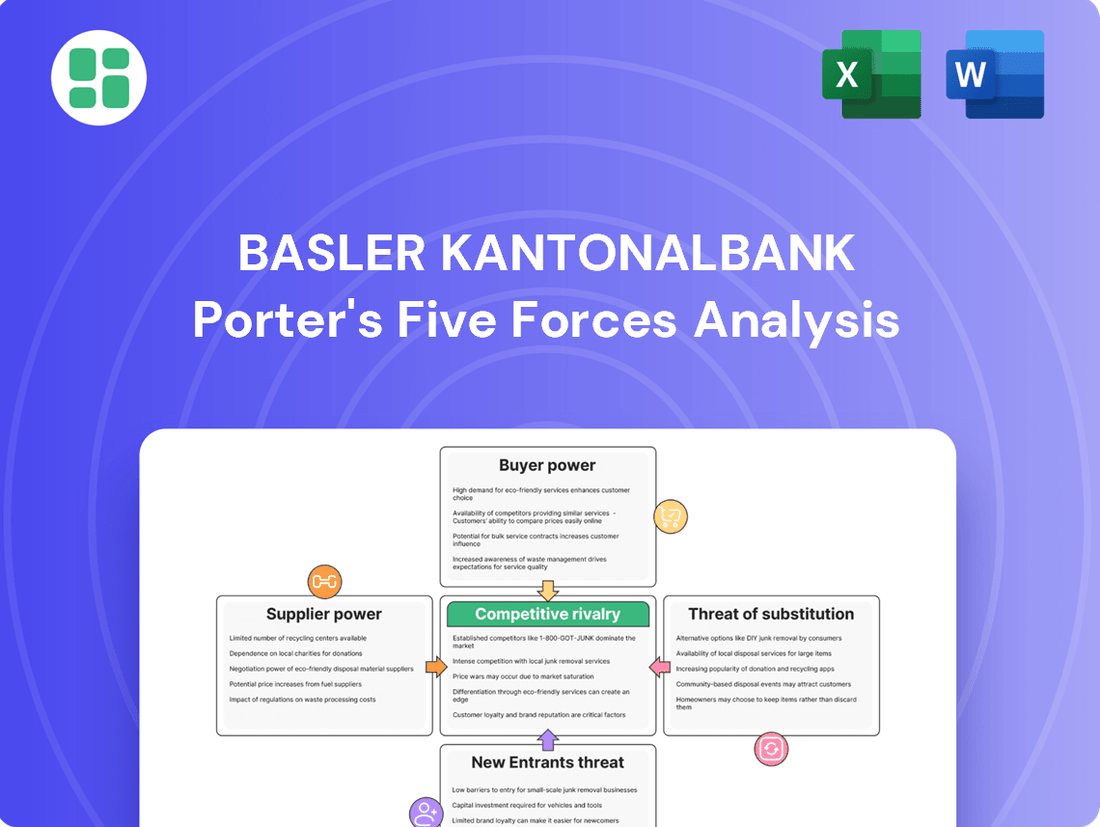

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The comprehensive Porter's Five Forces Analysis for Basler Kantonalbank details the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the Swiss banking sector. Understanding these forces is crucial for strategic decision-making and identifying opportunities for growth and competitive advantage.

Rivalry Among Competitors

Number and Diversity of Competitors

The Swiss banking sector, particularly in the Basel region, is highly competitive. Basler Kantonalbank faces rivals from numerous cantonal banks, specialized private banks, and major universal banks such as UBS. This broad spectrum of competitors, each with unique offerings, creates a dynamic and challenging environment for Basler Kantonalbank.

Industry Growth Rate

The Swiss banking sector, while stable, exhibits moderate growth, especially in areas like interest-bearing business. This maturity intensifies competition as banks like Basler Kantonalbank vie for a larger slice of the existing customer base rather than benefiting from rapid market expansion. For instance, in 2023, Swiss banks reported a combined net profit of CHF 20.1 billion, indicating a healthy but not explosive market.

Product Differentiation

While Basler Kantonalbank highlights its local presence and a broad range of services, many fundamental banking products are becoming increasingly similar across the industry. This commoditization means that basic offerings like savings accounts or mortgages often compete primarily on price.

To effectively counter this, Basler Kantonalbank needs to focus on strong product differentiation or truly unique service features. For instance, in 2023, Swiss banks saw a significant increase in digital banking adoption, with over 80% of customers using online channels for transactions, according to the Swiss Bankers Association. This trend underscores the need for innovative digital solutions or specialized advisory services to capture customer loyalty beyond price alone.

Exit Barriers

High regulatory hurdles in the Swiss banking sector, including stringent capital requirements and compliance mandates, represent a significant barrier for any bank considering exiting the market. These regulations, which were further solidified by Basel III and ongoing refinements, mean that the costs associated with winding down operations or selling off assets are substantial.

Basler Kantonalbank, like other cantonal banks, has invested heavily in specialized infrastructure and IT systems tailored to its specific operational needs and regulatory environment. These are significant sunk costs, making it economically unviable to simply abandon these assets without a substantial loss. For instance, the digital transformation efforts undertaken by Swiss banks in recent years, including significant investments in online banking platforms and cybersecurity, represent millions in unrecoverable expenditure if a bank were to exit.

Furthermore, the unique position of cantonal banks as institutions with a mandate to serve their canton adds a layer of social responsibility. This often translates into a commitment to local employment and community support, making a sudden or disorderly exit socially and politically difficult. This commitment ensures that competitors are unlikely to withdraw easily, thereby sustaining a competitive and often intense rivalry for Basler Kantonalbank within its operational sphere.

- Regulatory Complexity: Swiss financial regulations, such as those from FINMA, impose strict conditions on bank dissolution, increasing exit costs.

- Infrastructure Investment: Significant capital is tied up in physical and digital banking infrastructure, representing unrecoverable sunk costs for potential exiting firms.

- Social Mandate: The cantonal status of banks like Basler Kantonalbank creates an expectation of continued service, discouraging rapid market withdrawal.

- Sustained Rivalry: The combination of these factors locks competitors into the market, intensifying competition for Basler Kantonalbank.

Fixed Costs

The banking sector, including institutions like Basler Kantonalbank, is characterized by substantial fixed costs. These are primarily driven by significant investments in technology infrastructure, ongoing regulatory compliance mandates, and maintaining physical branch networks. For instance, in 2024, banks globally continued to invest heavily in digital transformation initiatives, with IT spending in the financial services sector projected to reach hundreds of billions of dollars.

These high fixed costs necessitate a focus on achieving economies of scale. To cover their operational expenses and achieve profitability, banks often resort to competitive pricing strategies, such as offering lower interest rates on loans or higher rates on deposits, to attract a larger customer base and increase transaction volumes. This drive for volume can intensify the rivalry among existing players.

- High Fixed Costs: Banks face substantial outlays for technology, compliance, and physical infrastructure.

- Economies of Scale: Achieving scale is crucial for profitability due to these high fixed costs.

- Aggressive Pricing: To gain volume, banks may engage in price competition, impacting margins.

- Intensified Rivalry: The pressure to cover fixed costs fuels a more aggressive competitive landscape.

Swiss Banking Sector: Intense Rivalry and Evolving Market Dynamics

Competitive rivalry within the Swiss banking sector, and specifically for Basler Kantonalbank, is intense due to a saturated market with numerous established players. The presence of large universal banks, other cantonal banks, and specialized private banks means that Basler Kantonalbank must constantly innovate and differentiate its offerings to attract and retain customers. For example, in 2024, the Swiss banking industry continued to see consolidation pressures, with smaller institutions merging to achieve greater scale and efficiency, directly impacting the competitive dynamics for mid-sized banks.

The similarity of core banking products, such as mortgages and savings accounts, further fuels price-based competition. Banks are compelled to offer competitive rates to gain market share, which can compress profit margins. This dynamic is evident in the ongoing competition for deposits, where even minor rate differentials can sway customer decisions. In 2023, average interest rates on savings accounts in Switzerland remained relatively low, highlighting the sensitivity of customers to even small yield improvements.

Additionally, high switching costs for customers, often tied to bundled services or established relationships, mean that while rivalry is fierce, customer inertia can play a role. However, digital advancements are lowering these barriers, enabling new entrants and fintech companies to challenge incumbents. The increasing adoption of digital banking platforms, with over 85% of Swiss banking transactions conducted digitally by mid-2024, underscores this shift.

| Competitor Type | Key Characteristics | Impact on Basler Kantonalbank |

| Cantonal Banks | Local focus, strong community ties, broad service range | Direct competition for regional market share, similar customer base |

| Universal Banks (e.g., UBS, Credit Suisse post-merger) | Global reach, extensive product portfolios, significant capital | Price leadership, innovation pressure, potential for cross-selling |

| Private Banks | Wealth management focus, personalized service, niche markets | Competition for high-net-worth individuals, specialized product offerings |

| Fintech/Digital Banks | Agile technology, lower overhead, innovative digital solutions | Disruption of traditional services, pressure on digital offerings and fees |

SSubstitutes Threaten

Fintech Solutions

The proliferation of fintech solutions presents a substantial threat of substitutes for traditional banking services. Companies offering specialized services like peer-to-peer lending, robo-advisory, and digital payments are increasingly attracting customers, particularly younger, tech-savvy demographics.

These fintech alternatives can effectively disintermediate established players like Basler Kantonalbank by providing more streamlined, often lower-cost, and user-friendly options for specific financial needs. For instance, the global fintech market was valued at approximately $2.4 trillion in 2024 and is projected to grow significantly, indicating a strong customer shift towards these innovative platforms.

Non-Bank Financial Institutions

Insurance companies, asset management firms, and other non-bank financial entities present a significant threat of substitutes for Basler Kantonalbank. These institutions increasingly offer investment products, wealth management, and lending services that directly compete with traditional banking offerings.

For instance, the Swiss insurance sector, a key area for substitutes, saw gross premiums written by Swiss insurers reach CHF 103.5 billion in 2023, according to Swiss Insurance Association data. This demonstrates the substantial capital managed by these firms, which can be channeled into investment and lending activities that bypass traditional banks.

Asset managers, particularly those focusing on specialized funds and alternative investments, also siphon away potential banking clients seeking higher yields or diversified portfolios. The Swiss asset management industry managed approximately CHF 1.4 trillion in assets under management as of the end of 2023, highlighting the scale of this competitive force.

Direct Investments and Digital Currencies

Customers increasingly have direct access to financial markets via online brokerage platforms, offering an alternative to traditional banking services. For instance, in 2023, the global online brokerage market was valued at approximately $10.5 billion, with a projected compound annual growth rate of over 10% through 2030, indicating a strong shift towards self-directed investing.

The rise of digital currencies presents another significant substitute, allowing for peer-to-peer transactions and alternative investment vehicles that bypass conventional banking infrastructure. By the end of 2024, the total market capitalization of cryptocurrencies is expected to reach over $2.5 trillion, demonstrating their growing influence as a potential substitute for traditional financial products and services offered by banks like Basler Kantonalbank.

Internal Corporate Finance

Large corporations often possess the financial muscle to bypass traditional banking channels. For instance, in 2024, many large Swiss firms explored alternative financing, including issuing corporate bonds which saw a robust market. This allows them to secure capital for major investments without needing extensive commercial banking relationships.

The availability of direct private equity and venture capital also presents a significant substitute. Companies seeking funding for growth or capital-intensive projects might directly approach private equity firms, thereby reducing their dependence on banks like Basler Kantonalbank for such needs. In 2023, global private equity fundraising reached over $1 trillion, indicating a strong alternative funding landscape.

Self-financing through retained earnings is another potent substitute. Profitable companies can reinvest their profits to fund expansion or new ventures, diminishing the need for external bank loans. This internal capital generation is a consistent and often preferred method for many established businesses.

- Corporate Bond Issuance: Large corporations can raise capital directly from the market, bypassing bank loans.

- Private Equity Investment: Direct investment from private equity firms offers an alternative funding source for growth.

- Self-Financing: Utilizing retained earnings for capital expenditures reduces reliance on external financing.

- Access to Capital Markets: Companies can tap into public markets for funding, offering a substitute for traditional bank lending.

Alternative Payment Systems

The threat of substitutes for traditional banking services, particularly in payment systems, is significant. Beyond standard bank transfers, a growing array of digital payment platforms and mobile wallets, such as Apple Pay and Google Pay, provide consumers with convenient alternatives for everyday transactions.

These alternative payment systems can erode the reliance on traditional bank accounts for daily commerce, potentially impacting Basler Kantonalbank's transaction volumes and fee income. For instance, in 2024, global mobile payment transaction value was projected to exceed $2.5 trillion, highlighting the substantial shift towards these digital alternatives.

- Digital Wallets: Services like PayPal, Revolut, and Wise offer streamlined international and domestic payment solutions, often with lower fees than traditional bank transfers.

- Mobile Payment Adoption: The increasing penetration of smartphones, with over 7 billion users globally by mid-2024, fuels the adoption of mobile payment solutions.

- Peer-to-Peer (P2P) Transfers: Apps facilitating direct P2P payments further bypass traditional banking channels for smaller, person-to-person transactions.

Banking Faces Multifaceted Substitute Threats

The threat of substitutes for Basler Kantonalbank is multifaceted, encompassing fintech innovations, alternative financial institutions, direct market access, digital currencies, and corporate self-sufficiency.

Fintech platforms, robo-advisors, and digital payment solutions are increasingly capturing market share, offering convenience and lower costs. The global fintech market's substantial 2024 valuation underscores this trend.

Moreover, insurance companies and asset managers are expanding their service offerings into areas traditionally dominated by banks, such as wealth management and lending, further diversifying the competitive landscape.

The increasing accessibility of capital markets for corporations, through bond issuance and direct private equity investment, significantly reduces their reliance on traditional bank financing.

| Substitute Category | Examples | Market Size/Growth Indicator (2023-2024 Data) |

|---|---|---|

| Fintech Solutions | Peer-to-peer lending, Robo-advisors, Digital payments | Global Fintech Market valued at ~$2.4 trillion (2024) |

| Alternative Financial Institutions | Insurance companies, Asset managers | Swiss Insurance Gross Premiums: CHF 103.5 billion (2023) Swiss Asset Management: ~CHF 1.4 trillion AUM (end 2023) |

| Direct Market Access | Online brokerage platforms | Global Online Brokerage Market valued at ~$10.5 billion (2023), projected >10% CAGR |

| Digital Currencies | Cryptocurrencies | Total Crypto Market Cap expected >$2.5 trillion (end 2024) |

| Corporate Self-Financing | Corporate bond issuance, Private equity, Retained earnings | Global Private Equity Fundraising: >$1 trillion (2023) |

Entrants Threaten

Capital Requirements

The Swiss banking landscape, known for its stringent regulations and robust capital adequacy requirements, presents a formidable hurdle for any new player. For instance, Swiss banks must adhere to capital ratios that are often higher than international benchmarks, demanding significant upfront investment. This high capital requirement effectively deters many potential entrants, safeguarding established institutions like Basler Kantonalbank.

Regulatory Hurdles

The stringent regulatory landscape in Switzerland, particularly the oversight by the Swiss Financial Market Supervisory Authority (FINMA), acts as a significant barrier. FINMA enforces rigorous licensing procedures, demanding substantial capital reserves and robust compliance frameworks, including strict anti-money laundering (AML) and know-your-customer (KYC) protocols. For instance, in 2023, FINMA continued its focus on operational resilience and cybersecurity, adding layers of complexity for any aspiring entrant.

Economies of Scale and Scope

Established banks like Basler Kantonalbank leverage significant economies of scale in their IT infrastructure and marketing efforts. This allows them to spread fixed costs over a larger customer base, resulting in lower per-unit operating expenses. For instance, in 2023, the average cost-to-income ratio for Swiss banks was around 62%, a figure that benefits from scale efficiencies.

New entrants face a considerable challenge in matching these scale advantages. Building a comparable IT system and launching a broad marketing campaign requires substantial upfront investment, making it difficult to compete on price or offer a full spectrum of services from the outset. This barrier is particularly high in a mature market like Switzerland, where customer expectations for digital services and product variety are already well-established.

Brand Loyalty and Trust

Basler Kantonalbank's deep roots in the Basel region and its long-standing reputation, cultivated over decades, foster significant customer loyalty and trust. This established goodwill acts as a substantial barrier for new entrants aiming to penetrate the Swiss banking market. For instance, in 2023, Basler Kantonalbank reported a customer base of over 400,000 individuals and businesses, underscoring its entrenched market position.

Newcomers must overcome the considerable challenge of building comparable brand recognition and trust, particularly within the conservative and highly regulated Swiss banking sector. This requires substantial investment in marketing and a lengthy period to establish credibility, making it difficult to attract customers away from established, trusted institutions like Basler Kantonalbank.

- Established Brand Reputation: Basler Kantonalbank benefits from a strong, regional brand identity built over many years.

- Customer Loyalty: A significant portion of its customer base demonstrates high loyalty, making acquisition by new entrants difficult.

- Trust Factor: The inherent trust in a cantonal bank, coupled with a long history of reliable service, deters customers from switching to unknown entities.

- Market Inertia: The conservative nature of the Swiss financial market often leads to customer inertia, favoring established players.

Access to Distribution Channels

New banks face substantial hurdles in establishing a widespread distribution network comparable to Basler Kantonalbank's established presence. Replicating its extensive branch network, ATM infrastructure, and sophisticated digital banking platforms demands considerable capital outlay and a significant time commitment. For instance, building out a physical footprint alone can cost tens of millions of Swiss francs, a prohibitive expense for many startups.

Basler Kantonalbank's existing, deeply entrenched physical and digital distribution channels act as a formidable barrier to entry. New entrants must either invest heavily to match this reach or develop truly disruptive innovations in customer access and service delivery to gain traction. In 2024, the average cost to open a new bank branch in Switzerland can range from CHF 1 million to CHF 5 million, depending on size and location, highlighting the capital intensity involved.

- Significant Capital Investment: Establishing a nationwide branch and ATM network requires hundreds of millions of Swiss francs.

- Time to Market: Building brand recognition and customer trust in distribution takes years, not months.

- Digital Platform Development: Creating secure and user-friendly digital banking services is a complex and costly undertaking.

- Competitive Landscape: Existing players like Basler Kantonalbank have already secured prime locations and customer relationships.

High Capital & FINMA Rules Protect Swiss Banks

The threat of new entrants into the Swiss banking sector, and specifically for Basler Kantonalbank, is significantly mitigated by high capital requirements and stringent regulatory oversight from FINMA. These factors demand substantial upfront investment and robust compliance, creating a formidable barrier for aspiring competitors. For instance, in 2024, the average capital required to establish a new bank in Switzerland is estimated to be in the tens of millions of Swiss francs, a figure that deters many potential new players.

Porter's Five Forces Analysis Data Sources

Our Basler Kantonalbank Porter's Five Forces analysis is built upon a foundation of publicly available financial statements, annual reports, and regulatory filings from the bank and its peers. We also incorporate insights from reputable industry publications, market research reports, and economic data from Swiss financial authorities.