Banco Bradesco Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Banco Bradesco Bundle

Don't Miss the Bigger Picture

Banco Bradesco navigates a dynamic financial landscape shaped by intense rivalry among established players and the looming threat of agile fintech disruptors. Understanding the bargaining power of its diverse customer base and the influence of regulatory bodies is crucial for its strategic positioning.

The complete report reveals the real forces shaping Banco Bradesco’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

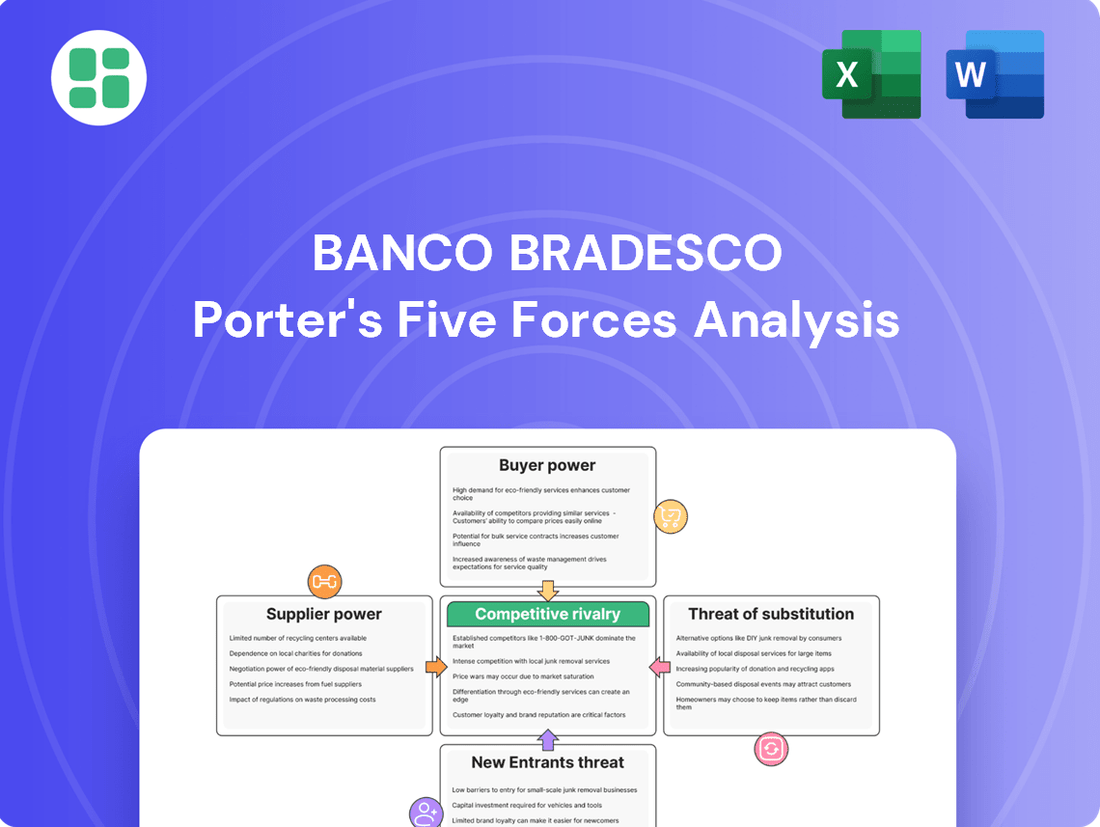

Suppliers Bargaining Power

Technology and Infrastructure Providers

The bargaining power of technology and infrastructure providers for Banco Bradesco is generally considered moderate to high. Bradesco, as a major financial player, depends on specialized IT systems, robust cybersecurity, and reliable network infrastructure to manage its vast operations, including its digital banking platforms and ATM network.

The highly specialized nature of these technology services, coupled with the substantial costs and complexities involved in switching core banking systems, grants these suppliers considerable leverage. For instance, the global market for core banking software is dominated by a few key players, limiting Bradesco's immediate alternatives.

However, Bradesco's sheer size and financial strength do provide it with significant negotiation power. The bank can leverage its scale to secure better pricing and terms, and it has the capacity to explore in-house development for certain critical technologies or diversify its vendor relationships to mitigate supplier dependency.

Human Capital (Skilled Labor)

The bargaining power of skilled labor for Banco Bradesco, especially in IT, data analytics, and financial innovation, is currently moderate to high. The Brazilian banking sector is actively pursuing digital transformation, which naturally drives up demand for these specialized professionals.

In 2024, the demand for IT professionals in Brazil saw significant growth, with some reports indicating a shortage of qualified candidates in areas like cybersecurity and cloud computing. This scarcity allows skilled workers to negotiate for better compensation and benefits, directly impacting Bradesco's labor costs and talent acquisition strategies.

Depositors and Capital Providers

Depositors, as a primary source of funding for Banco Bradesco, wield considerable collective bargaining power. While an individual depositor's influence is minimal, the aggregated decisions of millions of customers seeking favorable interest rates and superior services can shape Bradesco's deposit-gathering strategies. In 2024, Brazil's central bank interest rate, the Selic, remained a key benchmark influencing deposit rates offered by banks like Bradesco.

Institutional investors and capital markets are also crucial funding sources for Bradesco, providing capital through bonds and other financial instruments. These sophisticated providers of capital possess significant leverage, as their investment choices are heavily influenced by prevailing interest rates, overall economic stability in Brazil, and Bradesco's reported financial performance and credit ratings.

Interbank Market and Central Bank

The Central Bank of Brazil, through its monetary policy and the benchmark Selic rate, exerts significant influence over Banco Bradesco's cost of funds and lending activities. For instance, the Selic rate, a key indicator, saw adjustments throughout 2024, directly impacting the profitability and pricing strategies of major banks like Bradesco.

The interbank market, where banks lend to each other, represents another critical supplier relationship. Bradesco, despite its size, relies on this market for short-term liquidity. Fluctuations in interbank lending rates and the availability of funds can therefore affect Bradesco's operational efficiency and its ability to meet immediate financial obligations.

- Central Bank's Monetary Policy: The Central Bank of Brazil's decisions on the Selic rate directly influence Bradesco's cost of capital.

- Interbank Market Dynamics: Bradesco's dependence on the interbank market for liquidity means its operational flexibility can be swayed by market conditions.

- Regulatory Framework: The Central Bank also supplies the essential regulatory environment within which Bradesco operates, shaping its business practices and risk management.

Data and Information Providers

Data and information providers, such as those supplying financial data, market intelligence, and credit assessment tools, exert moderate bargaining power over institutions like Banco Bradesco. Bradesco's operational efficiency and strategic decision-making are heavily dependent on the accuracy and timeliness of the data it receives for crucial functions like risk management and regulatory compliance.

The specialized nature and often proprietary technology behind certain data services allow these suppliers to maintain pricing leverage. However, this power is somewhat tempered by the growing accessibility of alternative data streams and the increasing capacity for banks to generate and analyze their own internal data. For instance, in 2024, the global financial data market was valued at over $30 billion, indicating significant investment and reliance on these providers.

- Moderate Supplier Power: Data and information providers hold sway due to the critical nature of their offerings for banks.

- Reliance on Accuracy: Bradesco, like other financial institutions, needs precise and current data for risk, investment, and compliance.

- Specialization and Proprietary Data: Unique data sets and technologies enable suppliers to influence pricing.

- Counterbalancing Factors: The rise of alternative data sources and internal data capabilities can reduce supplier dominance.

Supplier Influence: A Critical Force in Banking Operations

The bargaining power of suppliers for Banco Bradesco is multifaceted, encompassing technology providers, skilled labor, capital sources, and data providers. While Bradesco's scale offers some negotiation strength, the specialized nature of many inputs, particularly in technology and skilled labor, grants suppliers considerable leverage. The cost and complexity of switching core systems or acquiring niche talent in a competitive market can significantly impact Bradesco's operational costs and strategic agility.

In 2024, the demand for IT professionals in Brazil, especially in cybersecurity and cloud computing, remained high, leading to increased salary expectations. Similarly, the cost of capital, influenced by the Central Bank of Brazil's Selic rate and interbank market conditions, directly affects Bradesco's funding expenses. The reliance on specialized data providers also means that the quality and cost of information can influence strategic decisions.

| Supplier Category | Bargaining Power Level | Key Factors Influencing Power |

|---|---|---|

| Technology & Infrastructure Providers | Moderate to High | Specialization of services, high switching costs, dominance of key software players. |

| Skilled Labor (IT, Data Analytics) | Moderate to High | High demand due to digital transformation, shortage of qualified professionals in Brazil in 2024. |

| Depositors (Retail & Institutional) | Moderate (Collective) | Individual power is low, but aggregated decisions on interest rates and services are influential; influenced by Selic rate. |

| Capital Markets & Investors | High | Sophisticated investors, influence of interest rates, economic stability, and credit ratings. |

| Central Bank of Brazil | Very High | Sets benchmark interest rates (Selic), dictates regulatory environment, influences cost of funds. |

| Interbank Market | Moderate to High | Crucial for short-term liquidity, influenced by market conditions and lending rates. |

| Data & Information Providers | Moderate | Specialized and proprietary data, reliance on accuracy for risk management and compliance; counterbalanced by alternative data sources. |

What is included in the product

This analysis of Banco Bradesco's competitive landscape reveals the intensity of rivalry, the bargaining power of customers and suppliers, and the threats posed by new entrants and substitutes, offering insights into its strategic positioning.

Effortlessly identify and mitigate competitive threats with a dynamic, interactive Porter's Five Forces model for Banco Bradesco.

Customers Bargaining Power

Individual Retail Customers

The bargaining power of individual retail customers is on the rise for Banco Bradesco, largely fueled by the expansion of digital banking and open finance. In 2023, Brazil saw significant growth in digital account openings, with neobanks capturing a substantial share, putting pressure on traditional institutions to innovate.

Customers now have unprecedented ease in comparing services and switching providers, thanks to user-friendly apps and competitive interest rates offered by a growing number of fintechs. This increased mobility means customers are more sensitive to pricing and expect highly personalized, seamless digital experiences from their banks.

Bradesco must therefore continue to invest heavily in its digital platforms and customer service to retain and attract these increasingly empowered individuals. The bank's focus on digital transformation in 2024 aims to address these evolving customer expectations directly.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) hold a moderate level of bargaining power with institutions like Banco Bradesco, primarily due to their demand for accessible credit and specialized financial services. While Bradesco offers a wide array of solutions, the growing presence of fintech companies providing niche lending and payment services gives SMEs alternative avenues, thus slightly increasing their leverage.

Bradesco's strategic emphasis on growing its SME client base, as evidenced by its continued investment in digital platforms and tailored product offerings, underscores the significance of this segment. This focus suggests Bradesco is actively working to provide competitive terms and customized solutions to retain and attract these businesses, mitigating their bargaining power by meeting their specific needs.

Large Corporate and Institutional Clients

Large corporate and institutional clients wield significant bargaining power, primarily due to the sheer volume of their transactions and their extensive network of financial service providers. These clients can easily switch between banks or tap into international capital markets, giving them leverage to negotiate more favorable terms on loans and other financial products. For instance, in 2024, major corporations often secured prime lending rates by comparing offers from numerous domestic and global institutions.

This ability to shop around means banks like Bradesco must compete aggressively on pricing and service quality to attract and retain these high-value customers. Institutions can demand lower fees for asset management or better rates on complex financial instruments, directly impacting a bank's profitability. Bradesco's strategy to counter this involves offering a broad spectrum of integrated services, from traditional banking to sophisticated investment banking and asset management solutions, thereby increasing client stickiness.

Increased Digital Adoption and Financial Literacy

The surge in digital adoption, particularly with Brazil's Pix instant payment system and the ongoing Open Finance initiatives, has dramatically amplified customer bargaining power. By mid-2024, Pix transactions were consistently exceeding 100 million daily, demonstrating a profound shift in consumer behavior towards digital channels.

As Brazilians become more adept with digital tools and gain greater financial literacy, their expectations for banking services have escalated. They now demand personalized experiences, seamless convenience, and absolute transparency in all transactions. This evolving landscape compels Bradesco to invest heavily in its digital infrastructure and incorporate advanced technologies, such as artificial intelligence, to retain its customer base.

- Pix adoption: Over 100 million daily transactions by mid-2024.

- Open Finance impact: Increased customer ability to compare and switch providers.

- Customer expectations: Demand for personalization, convenience, and transparency.

- Bradesco's response: Focus on digital innovation and AI integration to prevent churn.

Switching Costs and Loyalty Programs

While traditional banks once held significant sway due to high switching costs, the landscape has shifted. The emergence of digital-first competitors has considerably lowered these barriers, making it easier for customers to move their business. For instance, in 2024, the Brazilian fintech sector continued its rapid expansion, with new digital banks attracting millions of customers with streamlined onboarding processes.

Banco Bradesco is actively working to counteract this by cultivating customer loyalty. This involves offering a broad spectrum of services, developing integrated digital platforms, and exploring the potential of loyalty programs to retain its customer base. The bank recognizes that customer retention is increasingly dependent on delivering superior service and digital experiences, rather than relying solely on the inconvenience of switching.

- Digital Onboarding: In 2024, many new digital banks in Brazil reported onboarding times measured in minutes, a stark contrast to traditional banking processes.

- Customer Retention Strategies: Bradesco's focus on integrated digital platforms and comprehensive service offerings aims to increase stickiness, moving beyond inertia-based loyalty.

- Evolving Customer Expectations: The demand for seamless digital experiences means that customer loyalty is now a function of value and convenience, not just the difficulty of switching.

Digital Shift Empowers Customers, Reshaping Banking Loyalty

The bargaining power of customers for Banco Bradesco is significantly elevated due to the pervasive influence of digital channels and open finance initiatives in Brazil. By mid-2024, the daily volume of Pix transactions surpassed 100 million, underscoring a dramatic shift towards digital engagement and providing customers with greater transactional control and visibility.

This heightened digital fluency empowers customers to readily compare offerings across numerous providers, from traditional banks to agile fintechs, seeking competitive rates and personalized digital experiences. Consequently, customer loyalty is increasingly tied to the quality of digital service and value proposition rather than the friction of switching.

Banco Bradesco's strategy to mitigate this involves substantial investments in its digital transformation, aiming to enhance customer retention through integrated platforms and superior user experiences, thereby directly addressing the evolving demands of an empowered customer base.

| Factor | Impact on Bradesco | 2024 Data/Trend |

| Digital Channel Adoption | Increased customer ability to compare and switch | Over 100 million daily Pix transactions by mid-2024 |

| Open Finance | Lowered switching costs, greater transparency | Facilitated easier access to competitor services |

| Customer Expectations | Demand for personalization, convenience, and competitive pricing | Growing preference for seamless digital onboarding and service |

| Fintech Competition | Provided alternative banking solutions | Continued rapid expansion of digital banks in Brazil |

Preview Before You Purchase

Banco Bradesco Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Banco Bradesco, detailing the competitive landscape and strategic implications within the Brazilian banking sector. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, offering insights into buyer power, supplier power, threat of new entrants, threat of substitutes, and industry rivalry as they pertain to Bradesco's operations.

Rivalry Among Competitors

Dominance of Large Incumbents

The Brazilian banking landscape is heavily concentrated, with a few major players like Bradesco, Itaú Unibanco, Banco do Brasil, and Santander Brasil controlling a substantial portion of the market. This oligopolistic structure means these large incumbents are in constant, fierce competition with each other for customers and market share.

These 'mega-banks' collectively hold a dominant market share, making it challenging for smaller institutions to gain traction. They actively compete on pricing for loans and deposits, as well as on the innovation of financial services to attract and retain clients.

For instance, as of the first quarter of 2024, Bradesco reported total assets of R$1.9 trillion, while Itaú Unibanco reached R$2.8 trillion, highlighting their immense scale and the competitive pressure they exert on each other.

Rise of Digital Banks and Fintechs

The competitive rivalry for Banco Bradesco is intensifying due to the swift expansion of digital banks and fintech companies. Neo-banks such as Nubank, Banco Inter, and C6 Bank, alongside a vibrant fintech sector, are reshaping the financial landscape. These agile, digital-native competitors provide attractive features like reduced fees and superior user experiences, drawing in customers, especially younger segments and those previously underserved by traditional banking. For instance, by the end of 2023, Nubank reported over 99 million customers, highlighting the significant market share these new entrants are capturing.

Product and Service Diversification

Banco Bradesco faces intense rivalry as banks increasingly diversify beyond core lending. Bradesco's significant footprint in insurance and asset management allows for cross-selling opportunities, enhancing customer retention. This diversification strategy is mirrored by competitors, intensifying competition across a broader spectrum of financial services and necessitating ongoing innovation to secure market share.

Regulatory Environment Promoting Competition

The Central Bank of Brazil's proactive regulatory approach, exemplified by initiatives like Pix and Open Finance, is a significant driver of increased competition within the banking sector. These programs are specifically designed to foster financial inclusion and reduce traditional barriers to entry.

By facilitating data sharing and enabling instant payments, Pix and Open Finance empower smaller financial institutions and burgeoning fintech companies to challenge established players like Banco Bradesco more effectively. This regulatory shift compels traditional banks to continuously innovate and adapt to a more dynamic and competitive landscape.

- Pix adoption: By the end of 2023, Pix had over 150 million users in Brazil, processing an average of 30 million transactions daily, demonstrating its widespread impact on payment competition.

- Open Finance growth: As of early 2024, over 13 million Brazilians had authorized data sharing through Open Finance, creating new opportunities for competitive product offerings.

- Fintech market share: Fintechs in Brazil captured approximately 20% of the digital banking market by 2023, highlighting the success of regulatory changes in leveling the playing field.

Strategic Investments and Restructuring

Banco Bradesco, like other major financial institutions, is actively engaged in strategic investments and restructuring to sharpen its competitive edge. A significant portion of these efforts is directed towards technological advancements, including substantial outlays in artificial intelligence and cloud infrastructure. For instance, in 2024, Bradesco continued its digital transformation journey, aiming to streamline operations and elevate customer experiences.

These internal strategic shifts are a direct countermeasure to the intensifying rivalry within the financial sector. The bank faces pressure not only from established banking giants but also from nimble fintech companies that are rapidly innovating. By investing in technology and optimizing its organizational structure, Bradesco seeks to boost its profitability and solidify its market standing.

- Technology Investment: Bradesco's commitment to digital transformation involves substantial investments in AI and cloud migration, crucial for enhancing operational efficiency and customer engagement in 2024.

- Organizational Overhaul: The bank is undertaking internal restructuring to improve service delivery and cost management, a direct response to competitive pressures.

- Competitive Response: These strategic moves are designed to counter the growing threat from both traditional rivals and agile fintechs, aiming to maintain and grow market share.

- Profitability and Market Presence: The ultimate goal of these investments and restructurings is to enhance profitability and strengthen Bradesco's overall market presence in a dynamic financial landscape.

Brazil's Banking Battle: Traditional vs. Digital

Banco Bradesco operates in a highly competitive Brazilian banking sector, facing robust rivalry from both established financial institutions and agile digital players. The presence of large incumbents like Itaú Unibanco and Santander Brasil, alongside rapidly growing fintechs such as Nubank, intensifies pressure on pricing, service innovation, and customer acquisition. Regulatory initiatives like Pix and Open Finance further democratize the market, empowering new entrants and forcing traditional banks to adapt swiftly.

| Competitor | Total Assets (Q1 2024, R$ trillions) | Customer Base (End 2023, millions) | Digital Focus |

|---|---|---|---|

| Banco Bradesco | 1.9 | ~70 | High |

| Itaú Unibanco | 2.8 | ~90 | High |

| Nubank | N/A (Fintech) | 99+ | Very High |

| Banco do Brasil | 1.7 | ~75 | High |

| Santander Brasil | 1.0 | ~50 | High |

SSubstitutes Threaten

Digital Wallets and Instant Payment Systems (e.g., Pix)

The proliferation of digital wallets and Brazil's instant payment system, Pix, poses a substantial threat of substitution for traditional banking services offered by Banco Bradesco. Pix, introduced by the Central Bank of Brazil, facilitates immediate payments and transfers, thereby diminishing the necessity for conventional bank accounts, cards, and ATM usage. This shift diverts a significant portion of daily transaction volume from established banking channels, impacting fee-based revenue streams and the traditional role of physical bank branches.

Fintech Lending Platforms

Fintech lending platforms, such as peer-to-peer (P2P) lenders and online credit specialists, present a significant threat of substitution for traditional banks like Banco Bradesco. These digital alternatives often boast faster loan origination processes and can offer more competitive pricing, especially for borrowers who may not fit the traditional credit profiles. For instance, by mid-2024, reports indicated that fintech lenders were capturing an increasing share of the small business loan market in Brazil, offering a viable alternative for entrepreneurs seeking quick capital.

These platforms can siphon off profitable customer segments from Bradesco, particularly in areas like unsecured personal loans and small business financing. As of early 2024, the Brazilian fintech sector continued its robust growth, with several digital lenders reporting substantial increases in loan volumes, directly challenging incumbent banks. This trend suggests that Bradesco must continually innovate its lending products and customer experience to retain its market share against these agile competitors.

Non-Bank Investment Platforms

The proliferation of independent investment platforms and digital brokerages presents a significant threat of substitutes for traditional bank-offered investment and asset management services. These platforms frequently offer a broader selection of investment products, competitive fee structures, and advanced analytical tools, appealing to investors who prioritize greater portfolio control and potentially higher returns. For instance, in 2024, the Brazilian fintech sector continued its rapid expansion, with digital investment platforms capturing an increasing share of assets under management, directly challenging incumbent financial institutions like Banco Bradesco.

Insurance Alternatives and Direct Providers

The rise of direct insurance providers and specialized insurtechs poses a significant threat of substitution for Banco Bradesco's insurance products. These agile competitors often leverage digital platforms to offer more personalized policies, streamlined customer experiences, and potentially lower costs, directly challenging Bradesco's traditional bundled offerings.

For instance, in 2024, the Brazilian insurtech market continued its rapid expansion, with several startups gaining traction by focusing on niche segments or innovative distribution models. This trend means customers have more choices beyond traditional banking insurance packages, potentially eroding market share for established players like Bradesco Seguros.

- Increased Competition: Direct-to-consumer insurance platforms and insurtechs are simplifying the purchase process and offering specialized coverage, diverting customers from traditional bank-affiliated insurance.

- Customer Preference Shift: Younger demographics, in particular, are showing a preference for digital-first interactions and customizable insurance solutions, which many new entrants are better positioned to provide.

- Pricing Pressures: The operational efficiencies of some digital insurers can translate into more competitive pricing, forcing incumbents like Bradesco to re-evaluate their cost structures and product offerings.

Cryptocurrencies and Blockchain-based Solutions

The burgeoning world of cryptocurrencies and blockchain technology presents a potential, though currently limited, threat of substitution for traditional banking services. While not yet widely adopted for daily transactions, these innovations offer alternative avenues for value exchange, borrowing, and investment, potentially disintermediating established financial institutions. For instance, by mid-2024, the global cryptocurrency market capitalization hovered around $2.5 trillion, indicating a significant, albeit volatile, alternative financial ecosystem.

Brazilian financial institutions, including Banco Bradesco, are actively investigating and integrating digital assets and blockchain applications to navigate this evolving landscape. This proactive approach aims to leverage the efficiencies and new possibilities these technologies offer, ensuring continued relevance in a digitally transforming financial sector. Bradesco, for example, has been involved in pilot programs for tokenized assets, signaling a strategic move towards embracing these disruptive forces.

The threat is primarily long-term, as widespread consumer adoption for core banking functions remains a hurdle. However, as regulatory frameworks mature and user-friendliness improves, cryptocurrencies and decentralized finance (DeFi) could offer compelling alternatives for specific services like cross-border payments or yield generation, impacting traditional revenue streams. The potential for peer-to-peer lending platforms, for example, could reduce reliance on bank credit facilities.

Digital Innovation: Reshaping Banking Through Substitution

The rise of digital payment solutions, particularly Pix, directly substitutes many transactional services traditionally offered by Banco Bradesco. Pix's real-time, low-cost transfers diminish the need for traditional bank accounts for everyday payments, impacting fee income. By early 2024, Pix transactions in Brazil had already surpassed traditional bank transfers in volume, highlighting this substitution effect.

Fintech lenders and specialized credit platforms offer faster, often more accessible loan alternatives, particularly for small businesses and individuals. These platforms are increasingly capturing market share, as evidenced by reports in mid-2024 showing significant growth in fintech lending volumes, directly challenging Bradesco's traditional credit products.

Digital investment platforms provide a competitive alternative to Bradesco's asset management services, offering wider product choices and potentially lower fees. As of early 2024, digital brokerages in Brazil reported substantial increases in assets under management, indicating a growing preference for these substitute investment channels.

Insurtechs and direct insurance providers are simplifying policy acquisition and offering tailored products, substituting traditional bank-linked insurance offerings. The Brazilian insurtech market's rapid expansion in 2024, with startups focusing on niche areas, presents a clear threat to Bradesco's insurance segment.

Entrants Threaten

Regulatory Environment and Capital Requirements

The Brazilian banking sector presents a significant threat of new entrants due to its inherently high regulatory hurdles and substantial capital demands. The Central Bank of Brazil mandates complex licensing, rigorous prudential regulations, and stringent compliance standards, creating a formidable barrier for aspiring financial institutions.

However, recent policy shifts, such as the implementation of Open Banking and the Pix instant payment system, are designed to stimulate competition. These initiatives, while not eliminating all entry barriers, do offer a pathway for fintech companies to enter the market by reducing certain non-capital related obstacles.

Digital Disruption and Fintech Innovation

The threat of new entrants in banking, particularly for institutions like Banco Bradesco, is significantly amplified by nimble fintech startups and digital-only banks. These disruptors are adept at utilizing cutting-edge technology to deliver financial services that are not only innovative but also more affordable and user-friendly. They often sidestep the substantial overhead associated with traditional banks, such as extensive branch networks and legacy IT systems.

These agile competitors can rapidly onboard new customers, especially appealing to younger, digitally-savvy demographics. For instance, in Brazil, digital banks like Nubank have seen explosive growth, reaching over 90 million customers by early 2024, demonstrating the significant market share erosion traditional banks face. This rapid customer acquisition directly challenges the established positions of incumbent players.

Brand Loyalty and Trust

Established financial institutions like Banco Bradesco leverage decades of customer trust and robust brand recognition, creating a formidable barrier for new entrants. This deep-seated loyalty, often built over generations, translates into a significant competitive advantage that newcomers struggle to replicate. For instance, Bradesco's extensive branch network and long-standing reputation for security and reliability are not easily matched by emerging digital-only platforms.

Economies of Scale and Network Effects

Banco Bradesco's immense operational scale, built over decades, provides substantial economies of scale. This means they can spread their fixed costs, like technology infrastructure and marketing, across a much larger customer base than any new entrant could initially match. For instance, in 2023, Bradesco reported over R$2 trillion in assets, a figure that highlights the sheer magnitude of their operations and the cost advantages that come with it.

The network effect is also a significant barrier. Bradesco's extensive network of branches and ATMs, coupled with a large and loyal customer base, makes their services more valuable to existing users and more attractive to new ones. This established ecosystem is difficult and costly for newcomers to replicate. In 2023, Bradesco operated over 4,000 branches and service points across Brazil, a physical presence that digital-only competitors cannot easily overcome.

While traditional barriers are high, digital disruptors like Nubank have shown that a different approach can bypass some of these. Nubank, for example, achieved rapid scale and network effects through a purely digital model, leveraging viral marketing and significantly lower operational costs. By early 2024, Nubank had surpassed 100 million customers, demonstrating that a strong digital-native strategy can indeed challenge established players by creating its own form of network effect and achieving scale efficiently.

- Economies of Scale: Bradesco's R$2 trillion in assets (2023) allows for cost efficiencies in operations, technology, and marketing unmatched by startups.

- Network Effects: Over 4,000 branches and service points (2023) create a physical advantage, while a vast customer base enhances service value.

- Digital Disruption: Nubank's growth to over 100 million customers (early 2024) illustrates how digital-first strategies can build scale and network effects rapidly, bypassing traditional barriers.

Access to Funding and Talent

New entrants, especially smaller fintechs, often struggle to secure the substantial funding needed to compete with established players like Banco Bradesco. While venture capital investment in Brazil's fintech sector has seen growth, the capital demands for comprehensive financial service offerings remain a significant hurdle. For instance, in 2023, fintech funding in Latin America reached billions, but scaling to match incumbent infrastructure requires more than just initial capital.

Attracting and retaining top talent is another challenge for new entrants. Experienced professionals with deep knowledge of banking regulations and customer relations are often drawn to the stability and resources offered by larger, well-capitalized institutions. This talent gap can hinder a new entrant's ability to innovate and execute effectively in the competitive financial landscape.

- Funding Gap: Fintechs need significant capital to match the scale of operations of incumbents like Bradesco.

- Talent Acquisition: Established banks often have an advantage in attracting experienced financial professionals.

- Operational Scale: Building a robust infrastructure comparable to a large bank requires immense investment, deterring many new entrants.

Brazil's Banking: Fintechs Drive Digital Shift

Despite regulatory hurdles, the Brazilian banking sector is experiencing increased competition from agile fintechs. Initiatives like Open Banking and Pix are lowering some entry barriers, allowing digital disruptors to gain traction. However, established players like Banco Bradesco benefit from significant economies of scale and strong brand loyalty, making direct competition challenging for newcomers.

| Factor | Banco Bradesco Advantage | New Entrant Challenge |

|---|---|---|

| Capital Requirements | R$2 trillion in assets (2023) provides significant financial muscle. | Securing substantial funding to match incumbent scale is difficult. |

| Network & Trust | Over 4,000 branches (2023) and decades of customer trust. | Building a comparable physical presence and brand recognition takes time and resources. |

| Digital Disruption | Adapting to digital trends while maintaining legacy systems. | Rapidly scaling digitally, as seen with Nubank's 100+ million customers (early 2024), can bypass traditional barriers. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Banco Bradesco is built upon a foundation of comprehensive data, including the bank's annual reports, investor presentations, and regulatory filings with the Central Bank of Brazil. We also incorporate insights from reputable financial news outlets, industry research reports from firms like Fitch Ratings and Moody's, and macroeconomic data from sources such as the Central Bank of Brazil and IBGE.