Annaly Capital Management Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Annaly Capital Management Bundle

From Overview to Strategy Blueprint

Annaly Capital Management navigates a landscape shaped by intense competition, significant buyer power, and the constant threat of substitutes. Understanding these dynamics is crucial for any investor or strategist looking to grasp their true market position.

The complete report reveals the real forces shaping Annaly Capital Management’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Agency MBS

Annaly Capital Management's primary investment focus is on agency mortgage-backed securities (MBS), which are guaranteed by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. These GSEs are the principal issuers of these securities, wielding considerable influence over their supply and pricing dynamics.

The fundamental structure and guarantees associated with these MBS are absolutely vital to Annaly's entire business model. This reliance inherently grants the GSEs substantial bargaining power as suppliers, shaping the terms and availability of Annaly's core assets.

Cost of Capital and Funding Sources

Annaly Capital Management's ability to secure funding is crucial, and its reliance on repurchase agreements, securitizations, corporate bonds, and equity highlights the significant bargaining power of its suppliers. These suppliers, primarily banks and capital markets, dictate the terms and costs of capital. For instance, in early 2024, Annaly, like many in the mortgage REIT sector, navigated a landscape where short-term borrowing costs remained elevated due to ongoing monetary policy adjustments, directly impacting its net interest margin.

The cost of capital is a direct reflection of supplier power. When interest rates rise, as they did throughout much of 2023 and into 2024, Annaly's borrowing expenses increase, squeezing profitability. The availability of liquidity in the repurchase agreement market, a primary funding tool for Annaly, can also fluctuate, giving providers of these funds leverage. For example, during periods of market stress, the cost of repo funding can spike, making it more expensive for Annaly to finance its asset portfolio.

Regulatory and Policy Changes

Government policies and regulatory bodies, especially those influencing government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, exert significant indirect supplier power. These entities, which are crucial to the agency mortgage-backed securities (MBS) market where Annaly invests heavily, can alter the terms and availability of the assets Annaly trades.

The ongoing discussions about the potential privatization of Fannie Mae and Freddie Mac, or adjustments to their capital requirements and guarantee structures, represent a key area of regulatory influence. For instance, any significant changes to the GSEs' charters or operational frameworks could fundamentally reshape the MBS market, directly impacting Annaly's investment strategies and the overall risk associated with its portfolio. In 2024, the debate around GSE reform remained a prominent feature in financial policy discussions.

Repurchase Agreement Counterparties

Annaly Capital Management, like many mortgage REITs, relies heavily on repurchase agreements to finance its portfolio of agency Mortgage-Backed Securities (MBS) and residential credit investments. These repurchase agreements, often referred to as repos, are essentially short-term borrowing arrangements where Annaly sells securities and agrees to repurchase them later at a slightly higher price. The financial institutions that provide these crucial repo facilities hold significant bargaining power. They dictate the terms of the financing, including the interest rates charged, the haircut applied to the collateral (how much less the repo provider lends than the market value of the security), and the specific collateral requirements.

This power can manifest in several ways. Lenders can adjust rates based on market conditions, Annaly's creditworthiness, and the perceived risk of the underlying collateral. They can also impose stricter collateral requirements or reduce the amount they are willing to lend against certain assets, forcing Annaly to seek alternative, potentially more expensive, funding. For instance, during periods of market stress, repo rates can spike, increasing Annaly's cost of funds and compressing its net interest margin.

- Repo Market Dynamics: Annaly's ability to secure favorable repo financing is directly tied to the health and liquidity of the repurchase agreement market.

- Counterparty Concentration: While Annaly actively works to diversify its repo counterparties to mitigate concentration risk, a highly concentrated market of lenders could increase the bargaining power of individual institutions.

- Collateral Requirements: The terms set by repo counterparties, including haircut percentages on MBS and other assets, directly impact Annaly's leverage and the amount of capital it can deploy.

Mortgage Servicing Rights (MSR) Market

The bargaining power of suppliers in the Mortgage Servicing Rights (MSR) market, a key area for Annaly Capital Management, is moderate. Mortgage originators and servicers are the primary suppliers of MSRs. Factors like fluctuating origination volumes and changing prepayment speeds directly impact the supply and pricing of these rights. For instance, a slowdown in mortgage originations in 2023, driven by higher interest rates, could have tightened the supply of new MSRs available for purchase.

Annaly's strategic growth in its MSR portfolio highlights the importance of managing relationships with these suppliers. The availability and cost of acquiring MSRs are sensitive to market conditions and the operational success of originators and servicers. Annaly's ability to secure desirable MSRs at competitive prices depends on the competitive landscape among buyers and the overall health of the mortgage origination industry.

- Supplier Dependence: Annaly's reliance on mortgage originators and servicers for MSRs creates a degree of supplier influence.

- Market Volatility: Origination volumes and prepayment speeds, key determinants of MSR supply, are subject to economic and interest rate fluctuations.

- Regulatory Impact: Changes in mortgage regulations can affect the profitability and willingness of originators to sell MSRs, thereby influencing supplier power.

- Annaly's Strategy: Annaly's active expansion of its MSR holdings suggests a proactive approach to securing these assets despite potential supplier leverage.

Supplier Leverage: Shaping the Investment Firm's Market and Profitability

Annaly's primary suppliers are government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, which issue the agency mortgage-backed securities (MBS) Annaly invests in. These GSEs hold significant power due to their role in guaranteeing these assets, directly influencing their availability and terms. In 2024, the ongoing discussions surrounding GSE reform continued to highlight their influence over the MBS market, which is Annaly's core business.

Furthermore, Annaly's funding relies heavily on repurchase agreements (repos) from financial institutions. These repo providers dictate borrowing costs and collateral requirements, impacting Annaly's profitability. For instance, elevated short-term borrowing costs in early 2024, driven by monetary policy, directly affected Annaly's net interest margin, demonstrating the suppliers' leverage.

The bargaining power of suppliers in the Mortgage Servicing Rights (MSR) market is moderate. Factors such as mortgage origination volumes and prepayment speeds, which are sensitive to interest rate environments, influence the supply and pricing of MSRs. A slowdown in mortgage originations during 2023, a consequence of higher interest rates, tightened the supply of new MSRs, giving sellers more leverage.

What is included in the product

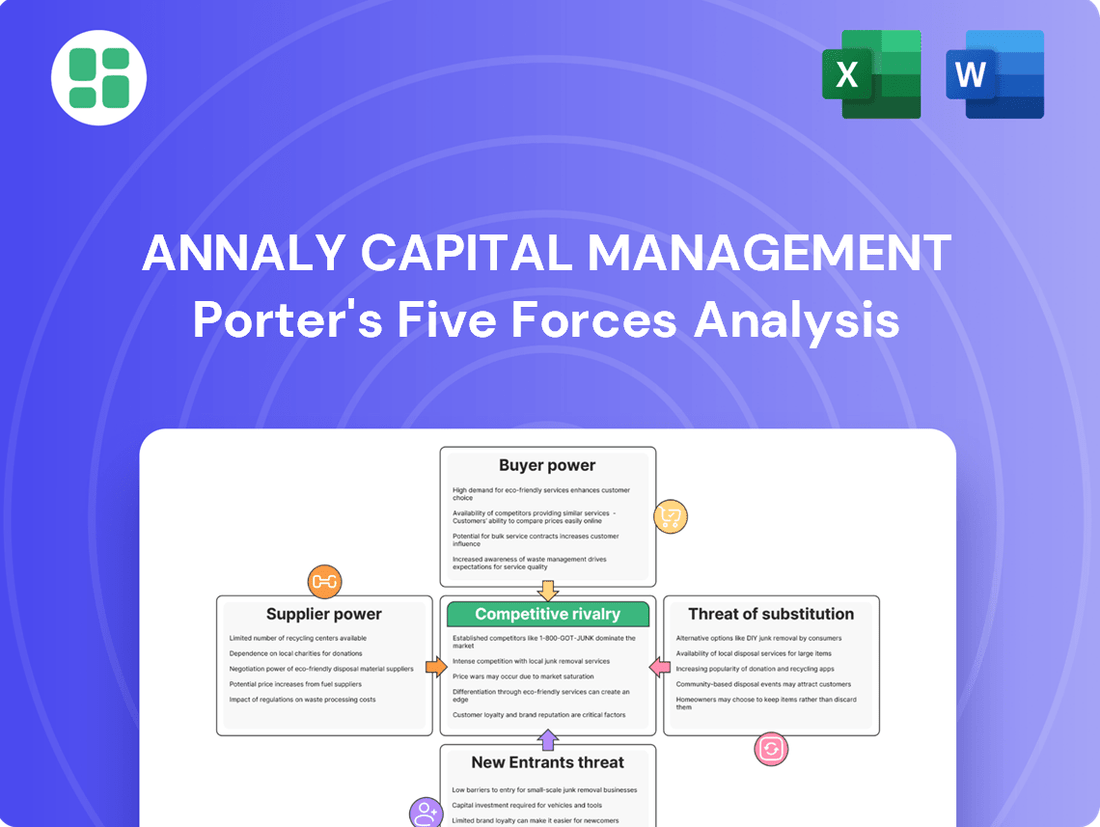

This Porter's Five Forces analysis for Annaly Capital Management dissects the competitive intensity, buyer and supplier power, threat of new entrants, and substitutes within the mortgage REIT industry.

Annaly Capital Management's Porter's Five Forces analysis provides a clear, one-sheet summary of all forces, perfect for quick decision-making and relieving the pain of complex market assessments.

Customers Bargaining Power

Shareholder Demands for Dividends

Annaly Capital Management, as a real estate investment trust (REIT), is fundamentally structured to generate income for its shareholders. This means shareholders are, in essence, the primary customers for the company's financial output, directly influencing its operational focus. Their demand for consistent and attractive dividend payments is a significant factor in Annaly's strategic decisions.

The power of these shareholder-customers is evident in their scrutiny of dividend sustainability. For instance, Annaly's dividend per share has seen fluctuations; a historical dividend cut can significantly impact investor sentiment and, consequently, the company's valuation. In 2023, Annaly reported a core earnings per share of $2.25, which supported its dividend payouts, but the market closely watches how this translates into future distributions.

Investor Sentiment and Capital Flows

Investor sentiment is a significant force affecting Annaly Capital Management. When investors feel optimistic about Annaly's prospects, it can drive up the stock price and make it easier for the company to raise more money through selling shares. Conversely, negative sentiment can hurt the stock and make raising capital more expensive.

Annaly demonstrated this in late 2024, successfully raising over $400 million in new equity. This trend continued into the first half of 2025, with the company bringing in more than $750 million via its at-the-market (ATM) program, highlighting the impact of positive investor sentiment on its capital-raising abilities.

Alternative Investment Options

Annaly's investors have a broad selection of alternative income-generating investments available to them. These include other Real Estate Investment Trusts (REITs), both equity and mortgage-focused, as well as corporate bonds and various dividend-paying stocks. This wide array of substitutes directly empowers customers, giving them significant bargaining power.

Should Annaly's risk-adjusted returns or dividend yield become less appealing compared to these alternatives, investors can readily shift their capital. For instance, in early 2024, the average dividend yield for equity REITs hovered around 3.5%, while mortgage REITs, like Annaly, often offered higher yields, sometimes exceeding 10%, depending on market conditions and specific holdings. This competitive landscape means Annaly must consistently offer attractive terms to retain investor capital.

Demand for Liquidity and Risk Profile

Investors scrutinize Annaly Capital Management, Inc. (NLY) not just on its liquidity but also on its risk-adjusted returns, especially given its operations in a sensitive interest rate climate. For instance, as of the first quarter of 2024, Annaly reported a book value per common share of $21.97, providing a tangible measure for investors assessing its underlying asset value and potential for capital appreciation against its market price.

Annaly's strategic approach involves a diversified portfolio, encompassing Agency mortgage-backed securities (MBS), Residential Credit assets, and Mortgage Servicing Rights (MSRs). This diversification is designed to offer stability and attractive risk-adjusted returns, aligning with investor demand for broad exposure within the housing finance sector.

- Liquidity Assessment: Investors evaluate Annaly's ability to meet short-term obligations and manage cash flows, particularly during periods of market stress.

- Risk-Adjusted Returns: Performance is judged by returns relative to the risk taken, a key metric for mortgage REITs operating in fluctuating interest rate environments.

- Portfolio Diversification: Annaly's holdings in Agency MBS, Residential Credit, and MSRs are intended to mitigate concentration risk and enhance overall portfolio stability.

- Investor Preferences: The company aims to cater to investor appetite for diversified exposure within the complex housing finance market.

Influence on Share Price and Valuation

The bargaining power of Annaly Capital Management's customers, primarily holders of its mortgage-backed securities and other debt instruments, can impact its profitability and, consequently, its share price. When customers have significant leverage, they can demand better terms, potentially reducing Annaly's net interest margin, a key driver of its earnings.

Shareholder activity is a direct reflection of this bargaining power and overall market sentiment towards Annaly. The buying and selling decisions of Annaly's shareholders directly influence its market capitalization and book value per share. For instance, if investors perceive that Annaly's customers are exerting too much pressure, leading to reduced profitability, they may sell their shares, driving down the stock price.

Shareholders' decisions, based on financial performance metrics like earnings available for distribution (EAD) and economic return, dictate the company's valuation in the public markets. In 2023, Annaly reported a distributable earnings per share of $2.26, and its book value per share stood at $20.98 as of December 31, 2023. Changes in these figures, influenced by customer-driven margin pressures, directly affect how the market values the company.

- Customer Leverage: High customer bargaining power can compress Annaly's net interest margin, impacting profitability.

- Shareholder Influence: Shareholder buying and selling directly affects Annaly's market capitalization and book value per share.

- Valuation Drivers: Financial performance, such as distributable earnings and economic return, dictates market valuation.

- 2023 Performance: Annaly's distributable earnings per share was $2.26, with a book value per share of $20.98 at the end of 2023.

Customer Influence on Net Interest Margin

The bargaining power of Annaly Capital Management's customers, primarily those holding its debt instruments or investing in its securities, is a significant factor. When these customers have many alternatives or can easily switch to other investments, they gain leverage. This can force Annaly to offer more attractive terms, potentially squeezing its profit margins.

For instance, the availability of numerous other mortgage REITs and fixed-income investments means Annaly must remain competitive. In the first quarter of 2024, Annaly's net interest margin was a key metric investors watched, and any pressure from customer demands could affect this. By the second quarter of 2024, Annaly reported a net interest margin of 1.77%, illustrating the ongoing need to manage this aspect.

The company's ability to retain capital and attract new investment hinges on its perceived value proposition relative to these alternatives. If Annaly's yield or risk profile becomes less appealing, customers can shift their funds, impacting Annaly's funding costs and overall profitability.

| Metric | Q1 2024 | Q2 2024 |

|---|---|---|

| Net Interest Margin | 1.77% | 1.77% |

Full Version Awaits

Annaly Capital Management Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis of Annaly Capital Management, detailing the competitive landscape and strategic implications for the company. The document you see here is precisely what you will receive immediately after purchase, offering an in-depth examination of industry rivalry, buyer and supplier power, threat of new entrants, and the threat of substitutes. Rest assured, this is the complete, ready-to-use analysis file, professionally formatted and prepared to inform your strategic decisions.

Rivalry Among Competitors

Presence of Numerous Mortgage REITs (mREITs)

The mortgage REIT sector is intensely competitive, featuring many public companies like AGNC Investment, Apollo Commercial Real Estate Finance, and Rithm Capital Corp. These entities frequently vie for the same investment opportunities, particularly in acquiring attractive mortgage-backed securities and other real estate debt. This crowded landscape means Annaly Capital Management faces constant pressure from peers seeking similar assets, driving down potential yields.

Homogeneous Products and Limited Differentiation

Annaly Capital Management, like many mortgage real estate investment trusts (mREITs), primarily operates within the agency mortgage-backed securities (MBS) market. These MBS are largely standardized, meaning there's little inherent difference between the products offered by various mREITs. This homogeneity naturally fuels intense competition, as firms like Annaly must differentiate themselves through superior operational efficiency and strategic acumen rather than unique product offerings.

The lack of product differentiation forces Annaly and its peers to compete fiercely on other fronts. Key areas of rivalry include the ability to secure lower borrowing costs, the sophistication of their portfolio management to optimize yield, and the effectiveness of their hedging strategies to mitigate interest rate risk. Success in generating spread income, the core of an mREIT's business, hinges on excelling in these operational and strategic aspects.

For Annaly, this means a constant focus on optimizing its cost of capital and refining its hedging techniques. In 2024, interest rate volatility continues to be a significant factor, making robust risk management paramount. The firm’s ability to navigate these market dynamics and maintain a competitive edge in spread generation is directly tied to its operational expertise in a market characterized by largely indistinguishable assets.

Sensitivity to Interest Rate Environment

Annaly Capital Management, like other mREITs, faces fierce rivalry directly tied to its sensitivity to interest rate shifts. The mREIT sector thrives on the spread between the interest earned on its mortgage-backed securities and its borrowing costs, making the yield curve a critical battleground. In 2024, the Federal Reserve's monetary policy, including potential rate hikes or cuts, significantly influences these spreads, intensifying the competition for stable, profitable financing and investment opportunities.

This sensitivity necessitates robust interest rate risk management, often through hedging strategies. These hedges, while crucial for stability, can incur costs and impact net interest margins, adding another layer of competitive pressure. Companies that can more effectively manage these risks and adapt to changing rate environments, such as Annaly, often gain an advantage over rivals who are less prepared for market volatility.

Access to Capital and Scale

Annaly Capital Management, like other mortgage real estate investment trusts (mREITs), relies heavily on its scale and efficient access to capital markets. This is crucial because mREITs are highly leveraged entities that fund their portfolios of mortgage-backed securities and other assets through a mix of short-term borrowings, primarily repurchase agreements (repos), and longer-term debt and equity. Having a large operational scale allows Annaly to negotiate more favorable terms on its funding, reducing its cost of capital. For instance, as of the first quarter of 2024, Annaly reported total assets of approximately $78.6 billion, demonstrating a significant scale that facilitates more efficient capital raising compared to smaller, less established players.

The ability to tap into diverse funding sources is a significant competitive advantage. Annaly's established institutional platform and market presence enable it to access a broad range of funding options, including repurchase agreements, securitization, and equity offerings. This diversification helps mitigate risks associated with relying on any single funding source and allows the company to adapt to changing market conditions. In 2023, Annaly successfully issued new equity, raising capital that bolstered its balance sheet and provided flexibility for portfolio management.

- Scale Advantage: Annaly's substantial asset base, exceeding $78 billion in early 2024, allows for economies of scale in funding operations, leading to lower borrowing costs.

- Diverse Funding Access: The company's institutional platform facilitates access to various capital sources, including repurchase agreements and equity markets, enhancing financial flexibility.

- Cost Efficiency: Larger mREITs like Annaly can operate at lower cost levels due to their size, enabling them to be more competitive in acquiring and managing assets.

- Market Access: Annaly's established presence in capital markets, evidenced by successful equity issuances in 2023, underscores its ability to raise capital efficiently.

Portfolio Diversification Strategies

Annaly Capital Management faces intense competition not just in agency mortgage-backed securities (MBS), but also as it diversifies into residential credit and mortgage servicing rights (MSRs). This expansion means Annaly is now competing with a broader range of players for attractive loan assets and MSR portfolios, aiming to boost returns and navigate different market conditions.

The rivalry in these diversified segments is a key factor. Companies are actively seeking to acquire non-agency loans and MSRs, a strategy Annaly itself has pursued to enhance its competitive standing and profitability. For instance, Annaly's strategic focus on growing its presence in these alternative credit areas highlights the dynamic nature of competition within the mortgage REIT sector.

- Diversification into Residential Credit: Annaly and its peers are increasingly active in acquiring non-agency residential loans, moving beyond traditional agency MBS.

- Competition for MSRs: The market for mortgage servicing rights is highly competitive, with companies vying for these revenue streams.

- Annaly's Strategic Growth: Annaly's expansion into these diversified areas demonstrates a proactive approach to managing risk and seeking enhanced returns in a competitive landscape.

- Impact on Returns: Success in these diversified segments can significantly impact a mortgage REIT's overall financial performance and resilience.

Mortgage REIT Competition: Navigating Yields and Rate Shifts

The competitive rivalry within the mortgage REIT sector is substantial, driven by a multitude of publicly traded companies like AGNC Investment and Apollo Commercial Real Estate Finance, all seeking similar investment opportunities. This crowded market means Annaly Capital Management constantly faces pressure from peers competing for the same attractive mortgage-backed securities and other real estate debt, which can compress potential yields.

Annaly's primary focus on agency mortgage-backed securities (MBS) means it operates in a market with largely standardized products, leaving little room for differentiation. Consequently, competition intensifies on operational efficiency and strategic execution, rather than product uniqueness. This necessitates Annaly to excel in securing favorable borrowing costs, sophisticated portfolio management for yield optimization, and effective hedging strategies to manage interest rate risk.

Annaly Capital Management, like its peers, is highly sensitive to interest rate shifts, making the yield curve a critical area of competition. The firm's ability to manage these risks and adapt to changing rate environments is paramount. In 2024, the Federal Reserve's monetary policy decisions directly impact the spreads Annaly relies on, intensifying the competition for stable financing and investment opportunities.

Annaly's scale, with total assets around $78.6 billion in Q1 2024, provides a significant advantage in securing lower borrowing costs through economies of scale. Its diverse access to capital markets, including repurchase agreements and equity, further enhances its financial flexibility and competitive standing, as demonstrated by successful equity issuances in 2023.

| Competitor Example | Asset Focus | Key Competitive Factor |

|---|---|---|

| AGNC Investment | Agency MBS | Scale and funding costs |

| Apollo Commercial Real Estate Finance | Commercial real estate loans and MBS | Diversified asset base and origination capabilities |

| Rithm Capital Corp. | Residential mortgage loans, MSRs, and other financial assets | Diversification and operational integration |

SSubstitutes Threaten

Other Income-Generating Investments

For income-seeking investors, Annaly Capital Management faces significant competition from a variety of substitute investments. Equity REITs, for instance, provide direct ownership in income-producing real estate, offering potentially more stable, albeit often lower, dividend yields than Annaly's mortgage-backed securities. In 2024, the average dividend yield for equity REITs hovered around 3.5%, a figure that can be attractive to investors prioritizing perceived stability over Annaly's higher yield potential.

Direct Real Estate Investment

Investors looking for real estate exposure can bypass Annaly's mortgage-backed securities and REITs by investing directly in physical properties or private syndications. This direct approach offers greater control over assets and can present a different risk-reward dynamic. For instance, in 2024, the U.S. housing market saw continued interest, with median home prices fluctuating but remaining a significant investment avenue for individuals.

Alternative Fixed-Income Securities

Investors have a broad universe of fixed-income alternatives beyond agency mortgage-backed securities. These include corporate bonds, municipal bonds, and U.S. Treasury securities, each offering different risk and return profiles. For instance, as of early 2024, yields on U.S. Treasury notes were competitive, potentially drawing capital away from MBS.

Non-agency mortgage-backed securities also present a substitute, though they carry different credit risk characteristics. The availability and attractiveness of these alternatives, influenced by macroeconomic conditions and market sentiment, directly impact the demand for Annaly's core holdings.

Private Credit and Lending Platforms

Private credit and direct lending platforms present a significant threat of substitutes for traditional mortgage real estate investment trusts (mREITs) like Annaly Capital Management. For large institutional investors, these private avenues allow direct investment in mortgage-related assets or other debt instruments, sidestepping publicly traded mREITs. This bypass can be attractive due to the potential for tailored investment solutions and, at times, enhanced yields, especially when factoring in illiquidity premiums. For instance, the private credit market has seen substantial growth, with global assets under management estimated to reach $2.7 trillion by 2027, indicating a growing appetite for these alternatives.

These platforms can offer investors more control and customized structures compared to the standardized offerings of publicly traded mREITs. This customization, coupled with the potential for higher returns driven by illiquidity and specialized underwriting, draws capital away from the public markets. The increasing sophistication and accessibility of these private debt markets mean that investors seeking exposure to similar asset classes now have viable alternatives that do not involve the liquidity or volatility of public equity markets.

- Growing Private Credit Market: Global private credit assets are projected to reach $2.7 trillion by 2027, highlighting a substantial alternative for investors.

- Investor Preference for Customization: Private lending platforms can provide bespoke investment solutions tailored to specific investor needs, contrasting with the standardized nature of mREITs.

- Yield Enhancement Potential: The illiquidity inherent in some private credit investments can translate into higher potential yields for investors willing to commit capital for longer terms.

- Direct Access to Mortgage Assets: Institutional investors can directly fund or invest in mortgage-related debt through these platforms, bypassing the need to invest in mREITs.

Commodities and Currencies

Commodities and currencies present a broad substitution threat to Annaly Capital Management's business model. In a wider investment portfolio, investors might view these asset classes as alternatives for diversification or as hedges against inflation, particularly during volatile market conditions when traditional income investments may struggle. For example, in early 2024, as inflation concerns persisted, investors looked towards assets like gold, which saw its price climb. This broad accessibility of alternative investments means that capital could be diverted away from mortgage REITs.

The threat is amplified by the accessibility of these alternatives. Investors can gain exposure to commodities through various ETFs and futures contracts, while currency trading is readily available through numerous platforms. This ease of access means that even during periods of economic uncertainty in 2024, where Annaly’s core strategy of investing in mortgage-backed securities might be less appealing, investors have readily available options. For instance, the US Dollar Index (DXY) saw fluctuations in 2024, attracting investor interest as a potential safe haven or trading opportunity.

- Diversification: Investors seek to spread risk across different asset classes, including commodities and currencies, which may perform differently than real estate investments.

- Inflation Hedging: Certain commodities, like precious metals, are traditionally seen as a hedge against rising inflation, a factor that can influence investor decisions in 2024.

- Market Volatility: During periods of high market volatility, investors may shift capital to perceived safer or more liquid assets like certain currencies or stable commodities.

- Accessibility: The increasing availability of exchange-traded funds (ETFs) and online trading platforms makes it easier for investors to access commodities and currencies, broadening the competitive landscape for Annaly.

Alternative Investments Challenge Mortgage-Backed Securities

The threat of substitutes for Annaly Capital Management is substantial, as investors have a wide array of alternative investment vehicles offering similar or even superior risk-adjusted returns. Equity REITs, for example, provided an average dividend yield of around 3.5% in 2024, presenting a more stable, albeit lower, income stream compared to Annaly's mortgage-backed securities. Direct real estate investments and private syndications also offer an alternative, with the U.S. housing market remaining a strong investment avenue throughout 2024.

Fixed-income alternatives, including corporate bonds and U.S. Treasury securities, also compete for investor capital. For instance, early 2024 saw competitive yields on U.S. Treasury notes, drawing attention away from mortgage-backed securities. Furthermore, the burgeoning private credit market, with global assets projected to reach $2.7 trillion by 2027, offers tailored solutions and potential yield enhancements, directly challenging Annaly's market position.

| Substitute Investment | 2024 Yield/Characteristic | Annaly's Potential Drawback |

|---|---|---|

| Equity REITs | Approx. 3.5% average dividend yield | Lower yield potential, but perceived stability |

| U.S. Treasury Notes | Competitive yields in early 2024 | Lower credit risk, potentially less yield |

| Private Credit | Projected $2.7 trillion AUM by 2027; potential for higher yields | Illiquidity, less standardization |

| Direct Real Estate | Fluctuating median home prices in 2024 | Higher capital requirements, illiquidity |

Entrants Threaten

High Capital Requirements

Establishing a mortgage REIT like Annaly Capital Management demands a massive initial investment. Newcomers need billions to acquire a diverse portfolio of mortgage-backed securities and other real estate assets to even compete. Annaly, for example, consistently manages a portfolio valued in the tens of billions of dollars, showcasing the sheer scale of capital required.

Regulatory and Compliance Burdens

New entrants aiming to operate as Real Estate Investment Trusts (REITs) face significant hurdles due to stringent regulatory and compliance requirements. These include mandatory distribution of at least 90% of taxable income to shareholders annually, which can impact capital retention and growth strategies for newcomers.

The broader financial services sector, where Annaly Capital Management operates, imposes its own set of complex regulations. Obtaining necessary licenses, adhering to rigorous financial reporting standards like GAAP, and implementing robust risk management frameworks are essential, adding substantial upfront costs and operational complexity for any potential new competitor.

Expertise in Mortgage Finance and Risk Management

The threat of new entrants into the mortgage Real Estate Investment Trust (mREIT) sector, particularly for a company like Annaly Capital Management, is relatively low due to the specialized knowledge required. Success hinges on deep expertise in mortgage markets, sophisticated interest rate hedging strategies, and robust credit risk management. For instance, Annaly's long history has allowed it to cultivate a team with the analytical prowess to navigate the complexities of managing a substantial, leveraged portfolio, a feat difficult for newcomers to replicate quickly.

Access to Diverse Funding Channels

New entrants to the mortgage REIT sector, like Annaly Capital Management, face a significant hurdle in establishing access to diverse funding channels. Securing repurchase agreements, credit lines, and public market access for debt and equity requires cultivating strong relationships with financial institutions and building a reputation for reliability, a process that is inherently time-consuming and trust-dependent.

For instance, in 2024, the cost of capital for new entrants can be significantly higher compared to established players who benefit from ongoing lender relationships and proven track records. This disparity in funding costs directly impacts profitability and competitive pricing of assets.

- Repurchase Agreements (Repos): Critical for short-term financing of mortgage-backed securities.

- Credit Facilities: Lines of credit from banks provide liquidity and flexibility.

- Public Capital Markets: Issuing debt and equity allows for long-term funding and balance sheet growth.

- Relationship Building: Establishing trust with diverse financial partners is paramount.

Brand Recognition and Investor Confidence

Established players like Annaly Capital Management benefit from decades of operating history, a strong brand, and a proven track record, which significantly bolsters investor confidence. For instance, as of Q1 2024, Annaly managed $98.4 billion in assets, a testament to its long-standing market presence. New entrants face the daunting task of cultivating similar trust and reputation to attract the necessary capital, presenting a substantial barrier in the highly competitive financial services sector.

Annaly's Moat: High Barriers to Entry in Mortgage REITs

The threat of new entrants for Annaly Capital Management is low due to immense capital requirements, exceeding billions for a competitive portfolio. Newcomers also face substantial regulatory hurdles, including strict REIT distribution rules and broader financial service compliance, demanding significant upfront investment and operational complexity.

Furthermore, the specialized knowledge in mortgage markets, interest rate hedging, and credit risk management is a significant barrier. Annaly's established reputation and decades of experience cultivate investor confidence, which new entrants struggle to replicate, impacting their ability to secure vital funding channels and maintain competitive capital costs.

| Factor | Impact on New Entrants | Annaly's Advantage |

|---|---|---|

| Capital Requirements | Extremely High (Billions) | Established Scale ($98.4B Assets Q1 2024) |

| Regulatory Compliance | Complex & Costly | Proven Track Record & Expertise |

| Specialized Knowledge | Steep Learning Curve | Decades of Market Navigation |

| Access to Funding | Difficult & Expensive | Strong Lender Relationships & Reputation |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Annaly Capital Management is built upon a foundation of comprehensive data, including Annaly's SEC filings, investor presentations, and earnings call transcripts. We supplement this with industry-specific reports from financial research firms, macroeconomic data from government agencies, and insights from reputable financial news outlets to capture the full competitive landscape.