American Addiction Centers Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

American Addiction Centers Bundle

From Overview to Strategy Blueprint

American Addiction Centers faces a dynamic landscape shaped by significant buyer bargaining power due to the availability of alternative treatment options. Intense rivalry among existing providers and the looming threat of new entrants also exert considerable pressure, impacting pricing and service innovation.

The complete report reveals the real forces shaping American Addiction Centers’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Medical Professionals

The bargaining power of specialized medical professionals like addiction psychiatrists, therapists, and nurses is a significant factor for American Addiction Centers (AAC). Their unique skills and the intense demand for these roles in addiction treatment give them considerable leverage. AAC depends on these experts for delivering critical services such as evidence-based therapies and medical detoxification. A scarcity of qualified professionals can directly impact operational costs through higher wages or impede the company's ability to grow its service offerings.

Pharmaceutical Companies

Pharmaceutical companies supplying medications for addiction treatment, including detox, craving management, and co-occurring mental health disorders, generally possess moderate bargaining power. While the market for some drugs is competitive with generic alternatives, the availability of proprietary or specialized medications can limit options for treatment centers like American Addiction Centers (AAC), granting these suppliers some pricing leverage.

In 2024, the pharmaceutical sector continues to see price increases on many essential medications. For instance, the average price of brand-name drugs increased by an estimated 5% in the first half of 2024. AAC's ability to negotiate favorable terms is directly tied to its significant purchasing volume and its capacity to identify and utilize therapeutically equivalent, potentially lower-cost, alternatives when available.

Accreditation and Licensing Bodies

Accreditation and licensing bodies, though not direct suppliers, hold considerable sway over American Addiction Centers (AAC). These organizations establish the essential standards AAC must adhere to for legal operation and to retain its reputation. Their mandates can influence everything from staffing requirements to facility upkeep, directly impacting operational costs.

For instance, changes in accreditation standards, such as those from The Joint Commission, could necessitate significant investments in training or infrastructure. In 2023, The Joint Commission reported that over 80% of accredited healthcare organizations met their core performance standards, indicating a general baseline of compliance, but any shift towards higher benchmarks would directly affect AAC's expenditure and operational flexibility.

Failure to meet these rigorous requirements means AAC cannot legally operate or attract patients, making compliance a critical, non-negotiable aspect of its business model. This dependence on external regulatory approval significantly strengthens the bargaining power of these bodies.

Specialized Equipment and Technology Providers

Providers of specialized medical equipment, diagnostic tools, and electronic health record (EHR) systems generally hold a moderate bargaining power over American Addiction Centers (AAC). The significant capital expenditure and ongoing maintenance associated with these critical technologies, coupled with substantial switching costs, contribute to this leverage. For instance, the healthcare IT market, which includes EHR systems, was valued at approximately $35.7 billion in 2023 and is projected to grow, indicating the importance and investment in these areas.

AAC's operational efficiency and ability to deliver personalized treatment plans are heavily dependent on integrated technology, including advanced diagnostic tools and robust EHR systems. This reliance, especially for cutting-edge solutions that enhance patient care and data management, grants these suppliers considerable influence. The complex integration and training required for new systems often make a complete overhaul prohibitively expensive and disruptive, further solidifying supplier power.

- High Integration Costs: Implementing and customizing specialized medical equipment and EHR systems can involve millions of dollars in upfront costs and ongoing integration services, making it difficult for AAC to switch vendors frequently.

- Proprietary Technology: Many advanced diagnostic tools and EHR platforms utilize proprietary software and hardware, limiting interoperability and increasing dependence on the original supplier for upgrades and support.

- Regulatory Compliance: The need to meet stringent healthcare regulations, such as HIPAA, means that EHR systems must be compliant and secure, often tying AAC to suppliers who can guarantee this level of adherence.

- Specialized Expertise: The specialized nature of the technology often requires specific training and support from the vendor, creating a barrier to entry for new suppliers and reinforcing the power of existing ones.

Real Estate and Facility Management Services

The bargaining power of real estate owners and facility management services for American Addiction Centers (AAC) can be substantial, particularly given the specialized needs of addiction treatment facilities. Securing suitable properties, especially for inpatient centers in accessible or desirable locations, presents a significant challenge and can lead to higher costs. For instance, in 2024, the average cost of commercial real estate leases in key metropolitan areas often saw increases, impacting operating expenses for healthcare providers.

Lease agreements and ongoing maintenance contracts represent considerable fixed costs for AAC. Providers who own unique or strategically positioned properties, offering specific amenities or adhering to strict healthcare regulations, can leverage this position to negotiate more favorable terms or command premium rental rates. This is especially true for facilities requiring specialized infrastructure, such as those with specific medical equipment or patient safety features, which are not readily available in standard commercial spaces.

- Specialized Property Needs: Addiction treatment centers often require specific layouts, privacy features, and compliance with healthcare regulations, limiting the pool of suitable and available properties.

- Location Sensitivity: Accessibility for patients and staff, along with proximity to necessary support services, makes location a critical factor, increasing the bargaining power of owners in prime areas.

- High Fixed Costs: Lease payments and facility maintenance represent significant, ongoing operational expenses, making favorable terms crucial for profitability.

- Limited Supply of Qualified Providers: The number of facility management companies experienced with healthcare-specific requirements can be limited, potentially giving them more leverage in contract negotiations.

Supplier Power Dynamics in Treatment Centers

The bargaining power of suppliers for American Addiction Centers (AAC) is influenced by several key groups, including specialized medical professionals, pharmaceutical companies, accreditation bodies, equipment providers, and real estate owners.

Specialized medical professionals, such as addiction psychiatrists and therapists, hold significant leverage due to their unique skills and high demand, directly impacting AAC's operational costs and growth potential.

Pharmaceutical companies possess moderate bargaining power, particularly for proprietary medications, though AAC can mitigate this through volume purchasing and exploring alternative treatments. For example, in the first half of 2024, brand-name drug prices saw an average increase of 5%.

Accreditation and licensing bodies exert considerable influence, as compliance with their standards is essential for AAC's legal operation and reputation, affecting operational costs and flexibility.

Providers of medical equipment and EHR systems also have moderate power due to high integration costs and proprietary technology, with the healthcare IT market valued at approximately $35.7 billion in 2023.

Finally, real estate owners and facility management services can have substantial bargaining power, especially for specialized properties in desirable locations, with commercial lease costs increasing in key metropolitan areas in 2024.

What is included in the product

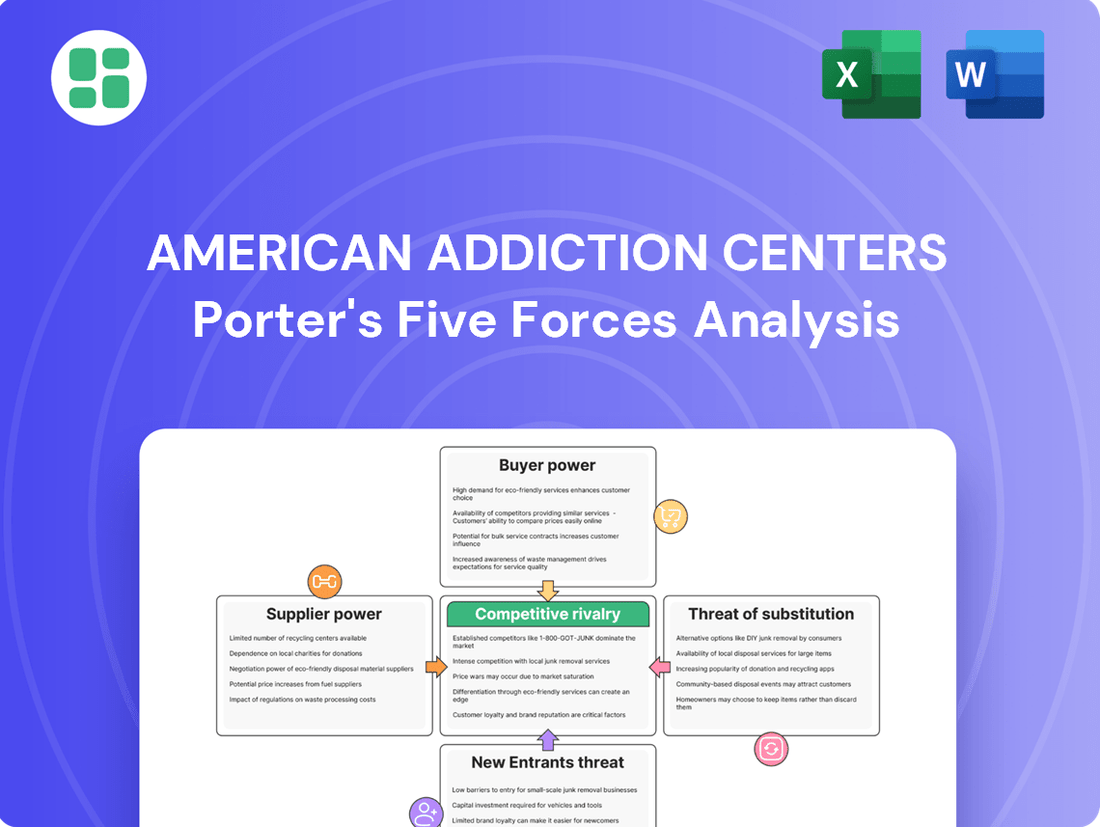

This analysis dissects the competitive forces impacting American Addiction Centers, revealing the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants, and the availability of substitutes within the addiction treatment industry.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces chart, simplifying complex market dynamics for American Addiction Centers.

Customers Bargaining Power

Individual Patients/Clients

Individual patients, despite needing critical addiction treatment, generally possess limited direct bargaining power. Their ability to negotiate is often constrained by the urgent nature of their condition and the specialized services required. For instance, in 2024, the average cost of inpatient addiction treatment in the US can range from $15,000 to $30,000, making price negotiation difficult for many.

The primary leverage for patients lies in their choice of providers, influenced by factors like reputation, treatment methodologies, and observed success rates. However, financial limitations and the significant emotional and psychological distress of addiction can further diminish their capacity to negotiate terms or prices with treatment centers.

Insurance Companies and Managed Care Organizations

Insurance companies and managed care organizations hold substantial sway as primary payers for addiction treatment. These entities actively negotiate reimbursement rates and define the scope of covered services, directly impacting American Addiction Centers' (AAC) revenue streams. Their influence extends to patient referrals, as network agreements often guide patients toward in-network facilities, thus affecting AAC's patient volume.

The bargaining power of these payers is evident in the ongoing pressure on healthcare providers to manage costs. For instance, in 2024, many insurance plans continued to scrutinize out-of-network benefits, pushing providers like AAC to secure more favorable in-network contracts or risk losing patient access.

Referral Sources (e.g., Doctors, Hospitals)

Referral sources, such as doctors, hospitals, and mental health professionals, wield significant indirect bargaining power over American Addiction Centers (AAC). These entities often serve as the initial point of contact for individuals seeking addiction treatment, acting as crucial gatekeepers that influence patient choice. Their recommendations are heavily weighted by patient trust and perceived quality of care.

AAC's ability to secure a consistent flow of patients relies heavily on nurturing these relationships. By demonstrating high standards of care, positive patient outcomes, and reliable service, AAC can incentivize these referral sources to continue sending patients their way. For instance, a primary care physician who trusts AAC's treatment protocols is more likely to refer patients to them than to a less-proven facility.

Employer-Sponsored Programs and EAPs

Employer-sponsored programs and Employee Assistance Programs (EAPs) are becoming more influential customers. These organizations are increasingly focused on value and tangible results for their employees, leading them to negotiate favorable terms and preferred provider arrangements. For American Addiction Centers (AAC), this means demonstrating the effectiveness of their tailored programs is crucial to attracting and retaining these significant clients.

The bargaining power of these employer groups is amplified by their ability to consolidate purchasing power. For instance, in 2024, many large corporations continued to expand their mental health and addiction benefits, seeking providers who can offer comprehensive, outcome-driven solutions. This trend suggests that AAC must be adept at showcasing quantifiable improvements in employee well-being and productivity to secure these contracts.

- Growing Demand: Employer EAP spending is projected to rise, with many companies prioritizing mental health and substance use support in 2024.

- Value-Based Purchasing: Employers are demanding evidence of treatment effectiveness and cost-efficiency, shifting focus from volume to outcomes.

- Negotiating Power: Large employers can leverage their size to negotiate bulk discounts and preferred pricing for addiction treatment services.

- Program Customization: AAC's ability to customize treatment plans to meet specific employer needs and employee demographics enhances its appeal.

Public Perception and Outcomes Data

The bargaining power of customers in the addiction treatment sector is significantly shaped by public perception and the availability of outcomes data. As individuals and their families become more discerning, they actively seek out treatment centers with proven track records, positive patient experiences, and transparent success metrics. American Addiction Centers (AAC) addresses this by emphasizing its commitment to evidence-based therapies and robust aftercare programs, thereby equipping potential patients with the information needed to make data-driven decisions.

This increased transparency empowers consumers, allowing them to compare providers based on tangible results rather than just marketing claims. For instance, a growing number of patients are looking for providers who can demonstrate long-term sobriety rates and successful reintegration into society. AAC's focus on measurable outcomes directly caters to this evolving customer expectation, enhancing its appeal to a more informed clientele.

- Informed Decision-Making: Patients increasingly research treatment efficacy, leading to greater demand for providers with transparent outcomes data.

- Reputation Matters: Positive testimonials and strong public perception directly influence patient choice, increasing the bargaining power of well-regarded facilities.

- Evidence-Based Therapies: A focus on therapies with demonstrated success rates, like those promoted by AAC, strengthens customer confidence and loyalty.

- Aftercare Importance: Comprehensive aftercare planning is becoming a key differentiator, as patients seek long-term support and relapse prevention strategies.

Customer Power Dynamics in Addiction Treatment: Insurers & EAPs

The bargaining power of customers for American Addiction Centers (AAC) is moderate, primarily influenced by insurance providers and employer EAPs. While individual patients have limited direct negotiation power due to the urgent nature of their needs, insurance companies and large employers can exert significant influence through reimbursement rates and preferred provider agreements. For example, in 2024, many insurance plans continued to scrutinize out-of-network benefits, pushing AAC to secure favorable in-network contracts.

Employer-sponsored programs and Employee Assistance Programs (EAPs) are increasingly important customers, demanding value and demonstrable results. These entities leverage their purchasing power to negotiate terms, with many large corporations prioritizing mental health and substance use support in 2024. AAC's ability to offer customized, outcome-driven solutions is crucial for securing these contracts.

| Customer Segment | Bargaining Power Influence | Key Factors for AAC |

|---|---|---|

| Individual Patients | Low | Urgency of need, limited negotiation capacity, emotional distress |

| Insurance Companies & Managed Care | High | Reimbursement rates, network contracts, scope of covered services |

| Referral Sources (Doctors, Hospitals) | Moderate (Indirect) | Trust, perceived quality of care, patient outcomes |

| Employer EAPs & Sponsored Programs | High | Value-based purchasing, program customization, consolidated purchasing power |

Preview Before You Purchase

American Addiction Centers Porter's Five Forces Analysis

This preview displays the complete American Addiction Centers Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape within the addiction treatment industry. The document you see here is precisely what you will receive instantly after purchase, ensuring you get the full, professionally formatted report without any alterations or missing sections. This analysis will equip you with a deep understanding of the industry's dynamics, including supplier power, buyer bargaining power, threat of new entrants, threat of substitutes, and the intensity of rivalry, all presented in the exact format you are currently viewing.

Rivalry Among Competitors

Fragmented Market with Diverse Players

The addiction treatment landscape is highly fragmented, featuring a wide array of providers from large national entities like American Addiction Centers (AAC) to smaller regional clinics, non-profits, and individual therapists. This sheer diversity fuels robust competition for both patient referrals and lucrative insurance agreements.

In 2023, the U.S. addiction treatment market was valued at approximately $53.4 billion, underscoring the significant revenue potential that attracts numerous players. This competitive environment necessitates that AAC clearly articulate its unique value proposition, emphasizing its integrated continuum of care and commitment to scientifically-backed treatment methodologies to stand out.

Competition on Quality and Specialization

Competition within the addiction treatment sector is intensifying, with providers increasingly differentiating themselves on the quality of care and specialized services offered. This includes a growing emphasis on treating co-occurring mental health disorders alongside substance use issues, as well as a focus on demonstrating tangible treatment outcomes. For instance, in 2024, many centers are highlighting their success rates in reducing relapse and improving overall patient well-being.

Providers are actively developing unique programs, incorporating advanced therapeutic modalities, and tailoring treatment plans to individual patient needs to attract a discerning patient base. This specialization allows centers to cater to specific demographics or addiction types, creating a competitive edge. American Addiction Centers' commitment to evidence-based therapies and personalized patient care serves as a significant differentiator in this dynamic market.

Geographic Concentration and Local Competition

While American Addiction Centers (AAC) has a national presence, the reality is that competition in the addiction treatment sector is often intensely localized. This means that while AAC might operate across many states, its facilities are directly competing with other treatment centers in the immediate vicinity for patients. This localized rivalry is a significant factor.

Factors like the physical proximity of treatment centers to patient populations, the local reputation a facility has built within a community, and the effectiveness of its community outreach programs become paramount. These elements can heavily influence patient choice, even when a national brand like AAC is available. For instance, a well-regarded local clinic might draw patients away from a larger, less familiar national provider.

AAC's strategy of establishing a network of facilities across the United States does offer some buffer against the harshest local pressures. By having multiple locations, AAC can spread its resources and brand recognition. However, this national footprint doesn't eliminate the intense regional rivalry; in many key markets, AAC still finds itself in direct competition with numerous other providers, each vying for a share of the local patient base.

Marketing and Brand Reputation

Providers in the addiction treatment sector, including American Addiction Centers (AAC), pour significant resources into marketing and brand building. This is vital for attracting patients and securing referrals in a crowded market. AAC's established national footprint and recognized brand name offer a distinct advantage, but this must be continually reinforced through ongoing marketing investments and a commitment to a positive public image to maintain its competitive edge.

The competitive rivalry in addiction treatment is intensified by the need for extensive marketing. For instance, in 2024, many treatment centers are heavily focused on digital marketing, including search engine optimization (SEO) and pay-per-click (PPC) advertising, to capture individuals actively seeking help. This often translates to substantial marketing budgets to ensure visibility and attract a consistent patient flow.

- Marketing Investment: Companies like AAC dedicate substantial portions of their revenue to marketing and advertising to build brand awareness and patient acquisition.

- Brand Reputation: A strong, positive brand reputation is a key differentiator, influencing patient choice and referral partnerships.

- Online Presence: A robust online presence, including website optimization and social media engagement, is critical for reaching potential patients.

- Referral Networks: Building and maintaining relationships with referring physicians, insurance providers, and other healthcare professionals is essential for patient volume.

Insurance Network Participation

Competition is intense for inclusion in preferred insurance networks, directly influencing patient access and revenue for addiction treatment providers. Companies like American Addiction Centers (AAC) actively vie for favorable contracts with major insurance carriers, understanding that network participation is crucial for business growth.

AAC's established relationships and broad facility network serve as key competitive advantages in securing these vital insurance agreements. However, maintaining these positions requires continuous negotiation and strict adherence to compliance standards, as insurers often adjust their network criteria.

- Network Inclusion is Key: Preferred insurance network participation directly impacts patient volume and revenue streams for addiction treatment providers.

- Provider Competition: Facilities actively compete to secure and maintain favorable contracts with major insurance carriers.

- AAC's Advantage: AAC's extensive facility network and existing insurance relationships are significant competitive assets in this arena.

- Ongoing Effort: Continuous negotiation and compliance are essential to retain and enhance competitive positioning within insurance networks.

Navigating the Competitive Addiction Treatment Market

The addiction treatment market is highly competitive, with numerous providers vying for patients and insurance contracts. This fragmentation means American Addiction Centers (AAC) faces rivalry not only from large national players but also from smaller, localized clinics that often have strong community ties.

Providers are increasingly differentiating themselves through specialized services and demonstrated treatment outcomes, with many centers in 2024 highlighting success rates in reducing relapse. AAC's focus on evidence-based therapies and personalized care is crucial for standing out in this dynamic environment.

Marketing and brand building are essential, as evidenced by the significant investments many centers, including AAC, make in digital marketing strategies like SEO and PPC advertising to attract patients actively seeking help.

Securing favorable contracts with major insurance carriers is another critical competitive battleground, directly impacting patient access and revenue for providers like AAC.

| Competitive Factor | AAC's Position | Market Trend (2024) |

|---|---|---|

| Market Fragmentation | Faces competition from national and local providers | Continued growth of specialized clinics |

| Differentiation | Emphasizes evidence-based, personalized care | Focus on co-occurring disorders and measurable outcomes |

| Marketing & Brand | Leverages national footprint and brand recognition | Increased digital marketing spend for patient acquisition |

| Insurance Networks | Strong existing relationships and broad network | Ongoing negotiation for favorable contract terms |

SSubstitutes Threaten

Self-Help Groups (e.g., AA, NA)

Self-help groups, such as Alcoholics Anonymous (AA) and Narcotics Anonymous (NA), present a considerable threat of substitutes for American Addiction Centers (AAC). These groups offer a free, accessible, peer-driven alternative for individuals seeking recovery. While many find them complementary to professional care, some may opt for these groups as their primary or sole recovery method.

AAC strategically mitigates this threat by often incorporating 12-step principles into its treatment programs and encouraging patients to continue their involvement in self-help groups post-treatment. This integration acknowledges the value of these substitutes and positions AAC as a comprehensive solution. For instance, studies have shown that consistent participation in AA can significantly improve long-term sobriety rates, highlighting the effectiveness of these peer-support networks.

Outpatient Therapy and Counseling

General outpatient therapy and counseling services, not specifically focused on addiction, can pose a threat by serving as substitutes for comprehensive addiction treatment, especially for less severe cases or during early intervention stages. These services are often viewed as more accessible and less stigmatizing than specialized addiction programs.

For instance, in 2024, the broader mental health counseling market experienced significant growth, with many providers offering general talk therapy that could address underlying issues contributing to substance use. This broad availability means individuals might opt for these less specialized services, potentially bypassing intensive, addiction-focused care.

American Addiction Centers (AAC) counters this threat by offering highly specialized, intensive outpatient programs (IOPs) and a full continuum of care specifically designed for addiction. This specialized approach, including evidence-based therapies like Cognitive Behavioral Therapy (CBT) and Dialectical Behavior Therapy (DBT) tailored to addiction, provides a distinct advantage over generalized counseling.

Alternative and Holistic Therapies (non-clinical)

Individuals seeking addiction recovery may turn to alternative and holistic therapies like acupuncture, meditation, or nutritional counseling, often bypassing traditional clinical settings. While these approaches can offer supportive benefits, they generally lack the scientifically validated medical and psychological frameworks essential for comprehensive addiction treatment.

American Addiction Centers (AAC) acknowledges the potential value of integrating certain holistic practices into treatment plans. However, the organization remains firmly committed to a clinically driven methodology that prioritizes evidence-based interventions and professional oversight to ensure patient safety and treatment efficacy.

Unsupervised Detox or Cold Turkey Methods

Individuals attempting unsupervised detox or quitting cold turkey present a significant threat of substitution for professional addiction treatment services. This approach bypasses the structured, medically monitored environment crucial for managing potentially life-threatening withdrawal symptoms. For instance, abrupt cessation of certain substances can lead to severe physical and psychological distress, making professional supervision a vital safeguard.

American Addiction Centers (AAC) emphasizes that unsupervised methods are a dangerous substitute because they lack the necessary medical oversight to ensure safety and effectiveness. This is particularly true for individuals dependent on substances like opioids or benzodiazepines, where withdrawal can be medically complicated and even fatal without expert care. In 2024, reports indicated that a substantial percentage of individuals struggling with substance use disorders attempt to self-manage their withdrawal, highlighting the prevalence of this risky substitute.

- Risk of severe health complications: Unsupervised detox can lead to dangerous physical and psychological reactions, including seizures, cardiac arrest, and severe depression.

- Lower treatment efficacy: Without professional guidance and support, individuals are more likely to relapse due to unmanaged withdrawal symptoms and cravings.

- Increased mortality rates: The lack of medical intervention for severe withdrawal symptoms significantly elevates the risk of death compared to medically supervised detox.

- Limited long-term recovery: Cold turkey methods often fail to address the underlying psychological and behavioral aspects of addiction, hindering sustainable recovery.

Ignoring the Problem or Delayed Treatment

The most prevalent substitute for professional addiction treatment is the decision to ignore the problem or delay seeking help. This often stems from denial, the pervasive stigma surrounding addiction, or concerns about the cost of care. In 2024, the Substance Abuse and Mental Health Services Administration (SAMHSA) reported that millions of Americans with substance use disorders did not receive treatment, highlighting the significant impact of this substitute behavior.

This inaction directly fuels the threat of substitutes by allowing addiction to progress, leading to more severe health consequences and increased societal costs. American Addiction Centers (AAC) actively works to mitigate this threat through extensive public awareness campaigns and by simplifying access to their services. They emphasize the critical advantages of early intervention and the long-term positive outcomes associated with their integrated treatment approaches.

- Ignoring the problem is a major substitute for professional addiction treatment.

- Denial, stigma, and financial worries contribute to delayed treatment.

- Inaction worsens addiction and increases long-term costs.

- AAC addresses this by raising awareness and reducing access barriers.

Beyond Self-Help: The Need for Specialized Addiction Treatment

The threat of substitutes for American Addiction Centers (AAC) is multifaceted, encompassing self-help groups, general counseling, holistic therapies, and even self-managed withdrawal. While these alternatives may offer some level of support, they often lack the comprehensive, evidence-based medical and psychological care that specialized addiction treatment provides. For instance, in 2024, the broader mental health counseling market saw substantial growth, with many providers offering general talk therapy that could address underlying issues contributing to substance use, presenting a more accessible option for some individuals.

| Substitute Type | Description | AAC's Mitigation Strategy | 2024 Relevance/Data Point |

|---|---|---|---|

| Self-Help Groups (e.g., AA, NA) | Free, peer-driven alternatives for recovery. | Integrates 12-step principles into programs; encourages post-treatment involvement. | Studies continue to show improved long-term sobriety rates with consistent AA participation. |

| General Outpatient Therapy | Less specialized counseling addressing underlying issues. | Offers specialized, intensive outpatient programs (IOPs) and a full continuum of care. | The general mental health counseling market grew significantly in 2024. |

| Holistic Therapies (e.g., acupuncture, meditation) | Alternative approaches lacking clinical frameworks. | Acknowledges potential value but prioritizes evidence-based, clinically driven methodology. | These methods are often pursued as complementary, not sole, treatment. |

| Unsupervised Detox/Cold Turkey | Bypasses medically monitored withdrawal. | Emphasizes the dangers and lack of efficacy due to absent medical oversight. | Reports in 2024 indicated a substantial percentage of individuals attempt self-managed withdrawal. |

| Ignoring the Problem/Delaying Help | Avoidance due to denial, stigma, or cost. | Public awareness campaigns; simplifying access to services; emphasizing early intervention. | SAMHSA reported millions of Americans with SUDs did not receive treatment in 2024. |

Entrants Threaten

High Capital Investment for Facilities

The threat of new companies entering the addiction treatment market is significantly reduced by the immense capital needed to set up and run facilities. This includes purchasing property, building structures, acquiring specialized medical equipment, and obtaining necessary licenses and accreditations. For instance, establishing a comprehensive inpatient facility can easily run into millions of dollars, making it a formidable hurdle for aspiring competitors.

Rigorous Licensing and Regulatory Requirements

The addiction treatment sector is a minefield of regulations, demanding extensive state and federal licensing, certifications, and adherence to healthcare laws like HIPAA and 42 CFR Part 2. This intricate web of compliance acts as a formidable barrier for any newcomer, requiring specialized legal knowledge and continuous dedication to rigorous standards. American Addiction Centers (AAC) leverages its existing, robust compliance infrastructure to navigate these complexities effectively.

Building a Reputable Brand and Trust

Building a reputable brand and fostering trust in the addiction treatment sector is a lengthy and resource-intensive endeavor. New entrants must overcome the significant hurdle of establishing credibility, especially in a field where patient well-being and ethical conduct are critical. American Addiction Centers (AAC) benefits from its established national recognition and years of operation, creating a substantial barrier for emerging competitors seeking to gain patient and referral source confidence.

Staffing Challenges and Talent Acquisition

The threat of new entrants in the addiction treatment sector is significantly hampered by staffing challenges. Attracting and retaining a highly qualified and specialized workforce, encompassing medical doctors, psychiatrists, and licensed therapists, presents a substantial barrier for newcomers. This difficulty is exacerbated by a general shortage of addiction specialists, driving up the costs associated with talent acquisition and retention.

American Addiction Centers (AAC), with its established hiring processes and the capacity to offer competitive compensation and benefits packages, is better positioned to secure the essential personnel needed to operate effectively. This existing infrastructure and financial flexibility create an advantage over potential new competitors who would struggle to build a comparable team from scratch in the current tight labor market.

For instance, in 2023, the demand for mental health professionals, including those specializing in addiction, continued to outpace supply. Reports indicated that many facilities faced extended hiring timelines, with some positions remaining unfilled for over six months. This underscores the difficulty new entrants would face in quickly assembling a qualified clinical staff, a critical component for providing quality care and gaining market traction.

- High demand for addiction specialists: A persistent shortage of qualified medical doctors, psychiatrists, and licensed therapists specializing in addiction treatment makes it difficult for new organizations to staff their facilities.

- Cost of talent acquisition: The scarcity of specialized professionals drives up recruitment costs and salary expectations, creating a significant financial hurdle for new entrants.

- AAC's competitive advantage: American Addiction Centers benefits from established hiring infrastructure and the ability to offer competitive compensation and benefits, aiding in securing necessary personnel.

Insurance Network Access and Contracting

New entrants face significant hurdles in gaining access to preferred insurance networks, a crucial element for patient acquisition and revenue generation. Established providers like American Addiction Centers (AAC) often benefit from long-standing relationships and a proven history with major payers, making it difficult for newcomers to secure favorable contracts.

Insurance companies tend to favor established providers with demonstrated quality outcomes and a broad geographic presence. This preference creates a substantial barrier for new addiction treatment centers, potentially limiting their patient base and financial viability. For instance, in 2024, securing in-network status with a top-tier national insurer can take 12-18 months or longer, often requiring extensive credentialing and demonstrated patient volume.

- Network Exclusivity: Many preferred provider organizations (PPOs) and managed care organizations (MCOs) have limited slots in their networks, making it challenging for new entrants to be added.

- Reimbursement Rate Negotiation: New entrants often have less leverage to negotiate competitive reimbursement rates compared to established players like AAC, impacting their profitability.

- Credentialing Delays: The process of getting credentialed with insurance networks can be lengthy and complex, delaying a new facility's ability to bill and receive payments.

- Geographic Concentration: AAC's established network of facilities across multiple states provides broader geographic coverage, which is attractive to insurers seeking to offer members wider access to care.

High Barriers Shield Established Addiction Treatment Providers

The threat of new entrants in the addiction treatment sector is significantly mitigated by the high capital requirements for facility setup and regulatory compliance. Building a reputable brand and securing insurance network access also present substantial barriers, favoring established players like American Addiction Centers (AAC). The competitive landscape is further shaped by the difficulty in acquiring specialized staff, a challenge AAC is better equipped to handle.

| Barrier Type | Description | Impact on New Entrants | AAC's Advantage |

|---|---|---|---|

| Capital Requirements | High costs for facilities, equipment, and licensing. | Formidable financial hurdle. | Established financial resources. |

| Regulatory Compliance | Complex state and federal licensing and accreditation. | Requires specialized legal knowledge and time. | Robust existing compliance infrastructure. |

| Brand Reputation & Trust | Building credibility is lengthy and resource-intensive. | Difficulty gaining patient and referral source confidence. | National recognition and years of operation. |

| Staffing Challenges | Shortage of qualified addiction specialists. | Extended hiring timelines and high recruitment costs. | Established hiring processes and competitive compensation. |

| Insurance Network Access | Securing in-network status with payers is difficult. | Limits patient base and revenue generation. | Long-standing payer relationships and proven outcomes. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for American Addiction Centers is built upon a foundation of comprehensive data, including publicly available financial reports, industry-specific market research from firms like IBISWorld, and regulatory filings from relevant government agencies.

We leverage insights from industry trade publications, competitor investor relations websites, and economic databases to thoroughly assess the competitive landscape, supplier and buyer power, threat of new entrants, and the intensity of substitutes.