Hammond Power Solutions Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Hammond Power Solutions Bundle

From Overview to Strategy Blueprint

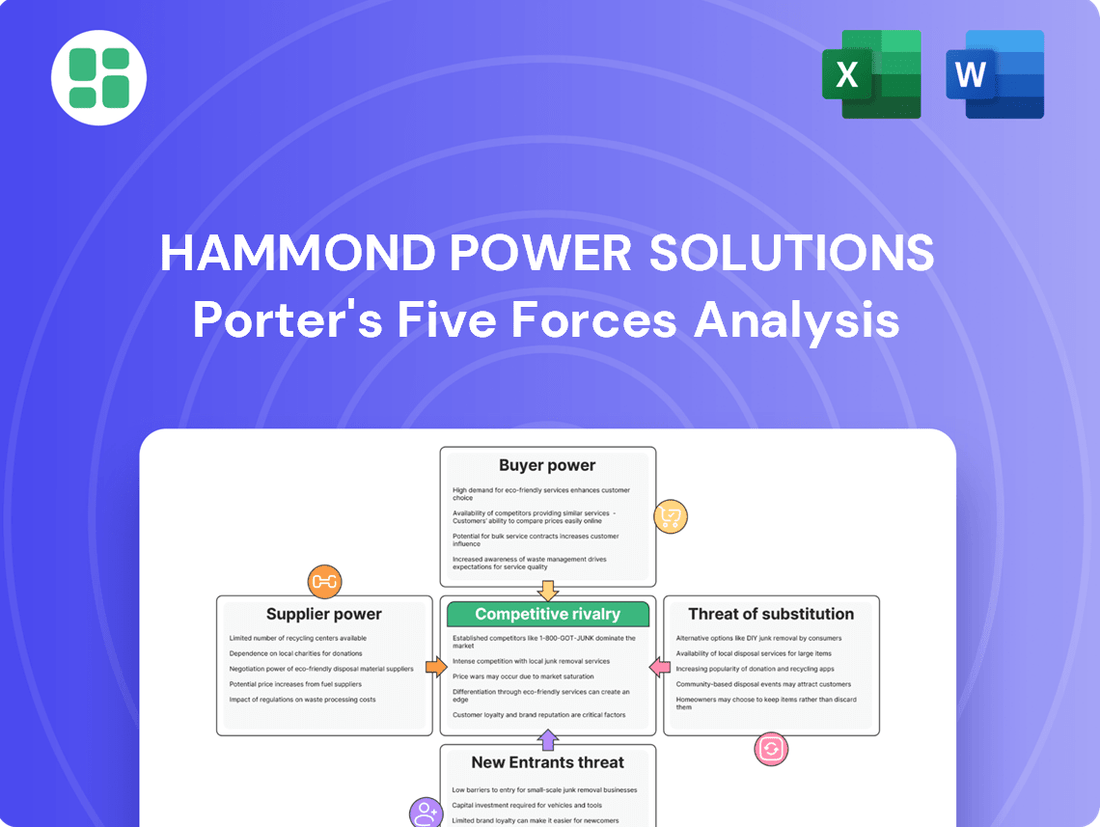

Hammond Power Solutions faces a dynamic competitive landscape, with moderate bargaining power from buyers and suppliers influencing its market position. The threat of new entrants is a key consideration, while the intensity of rivalry among existing players shapes strategic decisions.

The complete report reveals the real forces shaping Hammond Power Solutions’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Limited Supplier Pool for Key Raw Materials

The market for essential transformer components like Grain Oriented Electrical Steel (GOES) and copper is tightly controlled by a small group of suppliers. This scarcity means these suppliers hold considerable sway over pricing and availability.

For instance, the price of GOES has seen a dramatic 100% increase, while copper prices have risen by about 50% since the start of 2020. Such significant price hikes directly impact Hammond Power Solutions' production costs and profitability.

High Switching Costs for Manufacturers

For Hammond Power Solutions, switching suppliers for specialized components like GOES (Grain Oriented Electrical Steel) or core laminations isn't a simple task. It often necessitates substantial re-engineering of their transformer designs and rigorous re-qualification of the new supplier's materials. This complexity translates into high switching costs, effectively strengthening the hand of their current suppliers.

Supply Chain Disruptions and Lead Times

Ongoing global supply chain disruptions and geopolitical tensions, particularly evident in 2023 and continuing into 2024, have significantly extended lead times for critical components like specialized alloys and electrical steel used in transformer manufacturing. This scarcity directly empowers suppliers who can reliably deliver these materials, allowing them to command higher prices and dictate terms, thereby increasing their bargaining power over companies like Hammond Power Solutions.

Specialized Component Requirements

Transformers often demand highly customized components, necessitating specialized manufacturing capabilities. This reliance on niche expertise limits the pool of potential suppliers, thereby increasing their leverage.

The unique specifications required for many transformer parts mean that only a select few manufacturers can meet these demands. This scarcity of specialized providers grants them significant bargaining power, as buyers have fewer alternatives.

- Limited Supplier Base: The need for custom-engineered components restricts the number of viable suppliers for transformer manufacturers.

- High Switching Costs: Developing relationships and qualifying new suppliers for specialized parts can be time-consuming and expensive.

- Proprietary Technology: Some component suppliers may possess proprietary manufacturing processes or materials, further consolidating their market position.

Regulatory and Quality Compliance

Suppliers of materials and components for companies like Hammond Power Solutions face increasing demands for regulatory and quality compliance. This includes adhering to federal, state, and environmental regulations, as well as evolving energy efficiency standards. These requirements can significantly increase a supplier's operational costs and complexity.

Established suppliers who have already invested in meeting these stringent standards are better positioned. Their ability to consistently deliver compliant products gives them leverage. For instance, in 2024, the global transformer market saw a growing emphasis on energy-efficient designs, driven by regulations aimed at reducing electricity consumption and carbon emissions, directly impacting supplier requirements.

- Regulatory Hurdles: Suppliers must navigate a complex web of national and international regulations, impacting production processes and material sourcing.

- Quality Assurance Costs: Meeting rigorous quality standards, including those for energy efficiency, necessitates significant investment in testing and certification.

- Established Supplier Advantage: Suppliers with a proven track record of compliance and quality control are more valuable and can command better terms.

- Market Trends: The push for sustainability and efficiency in 2024 means suppliers who can meet these evolving demands gain a competitive edge.

Supplier Power: Specialized Inputs Drive Cost Increases

The bargaining power of suppliers for Hammond Power Solutions is significant due to the specialized nature of components like Grain Oriented Electrical Steel (GOES) and custom laminations. Limited suppliers for these critical inputs, coupled with high switching costs for Hammond, allow suppliers to exert considerable influence over pricing and terms. For example, the ongoing global emphasis on energy efficiency in 2024 means suppliers capable of meeting these stringent standards, such as those for advanced insulation materials, gain increased leverage. This is further amplified by supply chain vulnerabilities, which have historically led to substantial price increases, with GOES prices doubling and copper prices rising by approximately 50% since early 2020, demonstrating the suppliers' pricing power.

| Factor | Impact on Hammond Power Solutions | Supporting Data/Trend |

|---|---|---|

| Supplier Concentration | High | Limited number of GOES and specialized component manufacturers. |

| Switching Costs | High | Requires re-engineering and re-qualification of new materials. |

| Component Customization | High | Niche expertise needed, limiting supplier pool. |

| Regulatory Compliance | Increasingly Important | Suppliers meeting 2024 energy efficiency standards gain leverage. |

| Material Price Volatility | Significant | GOES prices up 100%, Copper up 50% (since early 2020). |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hammond Power Solutions' transformer manufacturing industry.

Instantly visualize competitive intensity across all five forces, enabling rapid identification of key threats and opportunities for Hammond Power Solutions.

Customers Bargaining Power

Diverse Customer Base Spanning Multiple Sectors

Hammond Power Solutions benefits from a broad customer base, serving original equipment manufacturers (OEMs), distributors, and end-users. This diverse clientele spans critical sectors like industrial, commercial, and renewable energy.

This wide reach across different industries means Hammond Power Solutions isn't overly reliant on any one customer group. For instance, in 2023, the company reported that its largest single customer accounted for only 10% of its total sales, demonstrating a healthy distribution of revenue and limiting the leverage of any individual buyer.

Customized Solutions and High Switching Costs

Hammond Power Solutions (HPS) excels at delivering customized solutions for power quality and energy efficiency, meaning their products are frequently engineered to meet unique client specifications. This high degree of customization inherently raises the barrier for customers to switch to a competitor, as it would necessitate substantial redesign or re-integration efforts, thereby increasing switching costs.

Importance of Product Quality and Reliability

For critical applications in electrical power distribution and control, product quality and reliability are absolutely paramount. Hammond Power Solutions, for instance, operates in sectors where equipment failure can lead to significant downtime and substantial financial losses for their clients.

Customers in industrial and utility sectors are often willing to pay a premium for proven reliability, directly impacting their price sensitivity. This focus on dependable performance means their bargaining power is somewhat reduced when faced with suppliers offering a strong track record and robust warranties.

Growing Demand in Key Market Segments

The transformer market is experiencing robust growth, particularly in sectors like data centers, infrastructure development, and the burgeoning battery storage industry. This surge in demand, fueled by the global transition to electrification and renewable energy sources, creates a favorable environment for suppliers like Hammond Power Solutions. For instance, the global demand for electricity is projected to increase significantly in the coming years, directly impacting the need for transformer capacity.

This heightened demand environment inherently limits the bargaining power of customers. When many buyers are competing for a limited supply of essential products, their ability to dictate terms, including pricing, is diminished. The sheer volume of projects requiring transformers means customers are less likely to find alternative suppliers willing or able to meet their immediate needs at significantly lower costs.

- Growing Demand: Key sectors like data centers and renewable energy infrastructure are driving substantial increases in transformer requirements.

- Electrification Trend: The global shift towards electric vehicles and broader electrification efforts further boosts demand for power distribution and conversion equipment.

- Reduced Customer Leverage: High overall demand weakens customers' ability to negotiate lower prices due to increased competition among buyers.

Customer Segmentation and Volume Impact

Hammond Power Solutions (HPS) serves a mix of large original equipment manufacturers (OEMs) and distributors. While the substantial order volumes from these major clients can grant them a degree of bargaining power, HPS's diversified end-user market offers a counterbalance. This broad customer base means that while large accounts have leverage, numerous smaller, specialized orders typically possess less individual power, diffusing overall customer pressure.

The bargaining power of customers for Hammond Power Solutions is influenced by several factors:

- Customer Concentration: HPS's reliance on a few large OEMs means these key accounts can exert significant influence due to the volume of business they represent.

- Order Volume vs. Diversity: While large orders provide leverage, the presence of many smaller, niche customers dilutes the collective bargaining power of the customer base.

- Switching Costs: The cost and effort for customers to switch to an alternative transformer supplier can impact their willingness to push for lower prices or better terms.

- Product Differentiation: The degree to which HPS's products are unique or specialized can reduce customer bargaining power, as alternatives may not offer the same features or performance.

HPS: Strong Position Against Customer Bargaining Power

Hammond Power Solutions' customer bargaining power is moderate, influenced by its diverse clientele and customized product offerings. While large OEMs can exert pressure due to order volume, the company's broad market reach and high switching costs for specialized solutions limit individual customer leverage.

The increasing demand for transformers, driven by electrification and infrastructure projects, further reduces customer bargaining power. For instance, the global electrical transformer market was valued at approximately $60 billion in 2023 and is projected to grow significantly, meaning customers have fewer alternatives when seeking essential components.

Hammond Power Solutions' ability to provide highly engineered, customized transformers means customers face substantial costs and integration challenges if they switch suppliers. This differentiation, coupled with the critical nature of their products where reliability is paramount, gives HPS a stronger position against price-sensitive buyers.

| Factor | Impact on Customer Bargaining Power | Hammond Power Solutions Context |

|---|---|---|

| Customer Concentration | High concentration increases power | Largest customer was 10% of sales in 2023, indicating moderate concentration. |

| Switching Costs | High costs decrease power | Customized solutions create high switching costs for clients. |

| Product Differentiation | High differentiation decreases power | Specialized engineering for power quality and efficiency. |

| Demand Environment | High demand decreases power | Robust growth in data centers, renewables, and electrification. |

Full Version Awaits

Hammond Power Solutions Porter's Five Forces Analysis

This preview showcases the complete Hammond Power Solutions Porter's Five Forces Analysis, detailing the competitive landscape and strategic implications for the transformer industry. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, providing actionable insights without any placeholders or alterations.

Rivalry Among Competitors

Fragmented Global Market with Numerous Players

The global transformer market is indeed a crowded space, with a vast number of companies vying for market share. This fragmentation means that while large, established players like Schneider Electric and Siemens are significant, there are also many smaller, regional manufacturers specializing in particular types of transformers. This diverse landscape fuels a highly competitive environment.

In 2023, the global transformer market was valued at approximately $55 billion, and it’s projected to grow, but this growth is spread across many participants. This fragmentation means that companies like Hammond Power Solutions often face intense price pressure and must constantly innovate to differentiate themselves. The sheer number of competitors, from global giants to niche producers, makes it challenging to gain a dominant position.

Presence of Large Global Competitors

Hammond Power Solutions faces intense competition from global giants such as Siemens AG, Schneider Electric SE, Hitachi Energy Ltd., and GE Vernova. These competitors boast considerable financial resources, expansive product offerings, and established worldwide distribution networks, allowing them to apply significant pressure on market share and pricing.

Product Differentiation and Customization

Hammond Power Solutions (HPS) actively differentiates its dry-type transformers and magnetic products by focusing on specialized applications and customized solutions. This strategy directly addresses specific power quality and energy efficiency requirements for clients.

This emphasis on tailored offerings allows HPS to maintain a strong competitive edge against manufacturers with more standardized product lines. For instance, in 2023, HPS reported revenue of $442.4 million, demonstrating market penetration achieved through its specialized approach.

Market Growth Driven by Electrification and Renewables

The dry-type transformer market is seeing substantial growth, fueled by increased industrial activity, expanding cities, and major spending on renewable energy sources and updating power grids. This growth allows more companies to enter and operate, which can temper the intensity of competition among existing players.

For instance, the global dry-type transformer market was valued at approximately USD 10.5 billion in 2023 and is projected to reach USD 16.2 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.4%. This expansion offers room for new entrants and existing manufacturers to gain market share without necessarily engaging in aggressive price wars.

- Market Expansion: The significant growth in demand for dry-type transformers, driven by electrification trends and renewable energy projects, creates opportunities for multiple competitors.

- Capacity Absorption: The expanding market size can absorb the production capacities of numerous players, potentially reducing the pressure for intense competitive rivalry.

- Investment Focus: Increased investments in grid modernization and renewable energy infrastructure globally, such as the Biden administration's Infrastructure Investment and Jobs Act in the US, which allocates billions to grid upgrades, directly benefit the dry-type transformer sector and support a more diverse competitive landscape.

Capacity Expansion and Strategic Acquisitions

Hammond Power Solutions, like many in the electrical equipment sector, faces intense competition driven by capacity expansion and strategic acquisitions. Companies are investing heavily to boost production and gain market share, signaling a dynamic and aggressive marketplace. For instance, in 2024, many competitors announced significant capital expenditures aimed at increasing manufacturing output for transformers and related components, responding to rising demand from infrastructure projects and renewable energy initiatives.

This trend is evident in the broader industry's M&A activity. Companies are actively seeking to acquire smaller players or complementary businesses to expand their product portfolios, geographical reach, and technological capabilities. This consolidation aims to achieve economies of scale and enhance competitive positioning. The pursuit of market dominance through these strategies intensifies the rivalry, forcing companies like Hammond Power Solutions to continually innovate and optimize their operations to remain competitive.

- Capacity Expansion: Competitors are increasing production volumes to meet surging demand, particularly in areas like grid modernization and electric vehicle charging infrastructure, with significant investments reported throughout 2024.

- Strategic Acquisitions: The industry saw a notable uptick in M&A activity in 2024 as companies sought to consolidate, acquire new technologies, and expand their market footprint.

- Market Share Focus: These actions underscore a strong emphasis on capturing greater market share, leading to heightened price competition and a drive for operational efficiency among all players.

Custom Solutions: Thriving in a Competitive Transformer Market

Hammond Power Solutions operates in a highly competitive landscape, facing pressure from global powerhouses like Siemens and Schneider Electric, who leverage vast resources and established networks. The market is fragmented, with numerous smaller, specialized manufacturers also vying for attention, leading to intense price competition and a constant need for innovation.

Despite this, the growing demand for dry-type transformers, projected to reach $16.2 billion by 2030 with a 6.4% CAGR, offers opportunities for market expansion. Hammond Power Solutions differentiates itself through customized solutions for specific power quality needs, a strategy that allowed it to achieve $442.4 million in revenue in 2023.

The industry is also characterized by significant capacity expansions and strategic acquisitions throughout 2024, as companies aim to increase production and consolidate market share. This aggressive pursuit of dominance intensifies rivalry, compelling players like Hammond to focus on operational efficiency and unique value propositions.

| Competitor | 2023 Revenue (Approx.) | Key Differentiator |

| Siemens AG | $72.0 billion (Energy Sector) | Global reach, broad product portfolio |

| Schneider Electric SE | $35.7 billion | Energy management, automation solutions |

| Hitachi Energy Ltd. | $10.0 billion (Est.) | Grid modernization, renewable integration |

| GE Vernova | $33.0 billion (Est.) | Energy transition technologies |

| Hammond Power Solutions | $442.4 million | Specialized dry-type transformers, customization |

SSubstitutes Threaten

Limited Direct Substitutes for Core Functionality

Dry-type transformers are critical for power distribution, and there are very few direct substitutes that can perform their core function across all applications. This makes them indispensable in many electrical infrastructure settings. For instance, in 2024, the global market for transformers was valued at approximately $50 billion, with dry-type transformers holding a significant and stable share due to this lack of direct alternatives.

Emergence of Solid-State Transformers (SSTs)

Solid-State Transformers (SSTs) are an emerging technological threat to traditional transformers. These advanced units boast higher efficiency, a smaller footprint, and superior control compared to conventional designs.

While current adoption is limited by cost, SSTs are poised to challenge the market, especially in areas like smart grids and electric vehicle charging infrastructure. For instance, by 2024, the global market for power electronics, which underpins SSTs, was projected to reach hundreds of billions of dollars, indicating significant investment and development in this area.

Technological Advancements in Magnetic Materials

Technological advancements, particularly in magnetic materials, present a significant threat of substitutes for traditional transformer manufacturers like Hammond Power Solutions. Innovations such as amorphous steel cores and nanocrystalline alloys are enhancing the efficiency and performance of existing transformer technologies. For instance, amorphous steel cores can reduce core losses by up to 70% compared to conventional silicon steel, making transformers more energy-efficient and cost-effective over their lifespan. This increased competitiveness of traditional transformers can slow the adoption of entirely new, potentially disruptive, substitute technologies.

Cost and Infrastructure Barriers for New Technologies

New technologies, such as solid-state transformers (SSTs), face substantial hurdles to broad acceptance, primarily due to their significant upfront costs and the extensive infrastructure modifications required for integration. For instance, the initial investment for SST technology can be considerably higher than for traditional transformers, potentially deterring widespread adoption by utilities and grid operators. This cost factor, coupled with the need for grid modernization to support these advanced systems, limits the immediate threat of substitution for established technologies.

These high barriers mean that while SSTs offer future potential, their current impact on the market remains limited. Companies like Hammond Power Solutions, which specialize in transformer manufacturing, benefit from this situation as the capital expenditure and technological retraining necessary for competitors to fully transition to new paradigms are substantial. The development and deployment of new grid infrastructure, including the necessary charging stations and communication networks for technologies like electric vehicles that might utilize advanced transformers, are ongoing processes that take considerable time and investment.

- High Initial Capital Expenditure: The cost of advanced transformers like SSTs can be significantly higher per unit compared to conventional transformers, impacting the economic viability for immediate large-scale replacement.

- Infrastructure Modernization Needs: Integrating new technologies often requires upgrades to existing electrical grids, including substations and distribution networks, which represent substantial additional investment and planning.

- Limited Scalability of New Technologies: While promising, the production and deployment of novel transformer technologies are not yet at a scale that can readily substitute the vast installed base of existing transformers.

- Technological Maturity and Reliability Concerns: Newer technologies may still be undergoing rigorous testing and validation to ensure long-term reliability and performance in diverse operational environments, which can slow adoption.

Dependence on Specific Applications and Regulations

The viability of substitute products for Hammond Power Solutions' transformers is significantly shaped by the specific needs of an application and the dynamic landscape of regulations. For example, in environments where fire safety is paramount, such as hospitals or densely populated urban areas, dry-type transformers are often the preferred choice over oil-filled units due to their inherent fire-resistant properties and reduced environmental impact. This preference limits the substitutability of oil-filled transformers in these critical sectors.

Regulatory shifts can further influence the attractiveness of substitutes. As environmental standards tighten, transformers that offer lower emissions or utilize more sustainable materials may gain an advantage. For instance, advancements in solid-insulation technologies for transformers could present a growing substitute threat if they meet performance requirements and comply with increasingly stringent environmental mandates. Hammond Power Solutions, like others in the industry, must monitor these evolving standards closely to understand how they might impact the demand for their existing product lines versus potential alternatives.

- Dry-type transformers offer superior fire safety and environmental benefits, making them a preferred substitute in sensitive applications.

- Evolving regulatory standards, particularly those concerning environmental impact and safety, can alter the competitive landscape for transformer types.

- The suitability of substitutes is directly tied to specific application demands, such as power density, operating environment, and maintenance requirements.

Transformer Substitutes: A Moderate but Growing Threat

The threat of substitutes for traditional transformers, like those produced by Hammond Power Solutions, is currently moderate but growing. While direct replacements offering equivalent performance across all applications are scarce, emerging technologies such as Solid-State Transformers (SSTs) present a future challenge. The global transformer market's substantial size, estimated at around $50 billion in 2024, indicates the entrenched nature of existing technologies, but the rapid growth in power electronics development, a key enabler for SSTs, signals potential disruption.

| Substitute Technology | Key Advantages | Current Market Penetration | Projected Impact |

|---|---|---|---|

| Solid-State Transformers (SSTs) | Higher efficiency, smaller footprint, superior control | Limited (due to high cost and infrastructure needs) | Growing threat, particularly in smart grids and EV charging |

| Advanced Magnetic Materials (e.g., amorphous steel) | Reduced core losses (up to 70% vs. silicon steel) | Increasing adoption in high-efficiency transformers | Enhances competitiveness of existing technologies, potentially slowing adoption of entirely new substitutes |

Entrants Threaten

High Capital Investment Requirements

Entering the transformer manufacturing sector, particularly for specialized equipment like those produced by Hammond Power Solutions, demands significant upfront capital. Newcomers face the hurdle of investing millions in state-of-the-art manufacturing plants, precision machinery for winding coils and assembling core components, and sophisticated testing apparatus to ensure product reliability and safety.

For instance, establishing a facility capable of producing high-voltage transformers, a core area for companies like Hammond Power Solutions, can easily run into tens of millions of dollars. This extensive capital outlay for infrastructure, technology, and skilled labor creates a formidable barrier, deterring many potential new competitors from entering the market.

Need for Highly Skilled and Technical Workforce

New entrants to Hammond Power Solutions' market face a significant hurdle in acquiring a highly skilled and technical workforce. This necessity stems from the advanced machinery and stringent product specifications inherent in transformer manufacturing. For instance, in 2024, the demand for specialized electrical engineers and technicians continued to outpace supply, driving up recruitment costs and lead times for new market participants.

The specialized nature of the transformer industry means that simply hiring general labor is insufficient. New companies must invest heavily in recruiting, hiring, and then training individuals who can operate complex equipment and adhere to precise quality standards. This labor access challenge, particularly for those with expertise in areas like electromagnetic design or advanced welding techniques, acts as a considerable barrier to entry.

Established Global Supply Chains

Established global supply chains represent a significant barrier to entry for new competitors in the power transformer market. Companies like Hammond Power Solutions have spent years building robust relationships with key suppliers for essential materials such as copper and electrical steel. For instance, in 2024, the price of copper, a primary component in transformer windings, remained volatile, influenced by global demand and geopolitical factors, underscoring the importance of secure and cost-effective sourcing agreements.

New entrants would struggle to replicate these established networks, facing higher procurement costs and potential supply disruptions. Building trust and securing favorable terms with these specialized material providers requires time and proven reliability, which newcomers lack. This advantage allows incumbents to maintain more stable production costs and delivery schedules, further deterring potential market entrants.

Brand Reputation and Customer Relationships

Established players like Hammond Power Solutions benefit from deeply ingrained brand reputations built over decades, fostering strong customer loyalty. For instance, their long-standing relationships with original equipment manufacturers (OEMs), distributors, and major utility companies are a significant barrier to entry. These relationships are not easily replicated by new entrants, as trust and proven performance are paramount in the power solutions sector.

The extensive history of reliable service and product quality cultivated by incumbent firms creates a formidable challenge for newcomers. Building comparable brand equity and securing the same level of trust from key industry stakeholders requires substantial investment and a proven track record, which takes considerable time to develop.

In 2024, the power transformer market, where Hammond operates, continues to emphasize reliability and long-term partnerships. New entrants face the uphill battle of not only matching product specifications but also demonstrating the same level of commitment and service that established players have consistently provided. This often translates into a longer sales cycle and higher initial marketing costs for new companies attempting to gain market share.

- Established Brand Loyalty: Hammond Power Solutions leverages its long-standing reputation for quality and reliability, making it difficult for new entrants to win over customers accustomed to their proven performance.

- OEM and Utility Relationships: Decades of collaboration with key industry players like OEMs and utilities create strong switching costs and preferred supplier arrangements that new competitors struggle to penetrate.

- Time and Investment Hurdle: Building the necessary trust, service infrastructure, and market presence to compete effectively requires significant time and capital investment, acting as a deterrent for potential new entrants.

Complex Regulatory Environment and Standards

The transformer industry faces a significant threat from new entrants due to the complex and evolving regulatory environment. Companies looking to enter must contend with a web of federal, state, and environmental regulations, including stringent energy efficiency standards. For example, in 2024, ongoing updates to DOE (Department of Energy) efficiency standards for distribution transformers continue to shape market entry requirements.

Navigating these intricate compliance and testing procedures represents a substantial barrier. New entrants must invest heavily in ensuring their products meet these rigorous specifications, which can be costly and time-consuming. This regulatory hurdle significantly deters potential competitors who may lack the expertise or capital to manage such complexities effectively.

- Evolving Federal and State Regulations: Continuous updates to energy efficiency standards and environmental compliance requirements.

- Stringent Testing Procedures: New entrants must pass rigorous testing to prove product compliance.

- High Capital Investment: Significant upfront costs are required to meet regulatory demands and establish compliant manufacturing processes.

Why New Entrants Struggle in the Specialized Transformer Sector

The threat of new entrants for Hammond Power Solutions is moderate, primarily due to high capital requirements and established supplier relationships. However, the specialized nature of transformer manufacturing and the need for deep industry expertise also serve as significant deterrents.

In 2024, the demand for advanced manufacturing capabilities and a skilled workforce continues to be a critical factor. Newcomers must overcome substantial hurdles in acquiring both the necessary technology and the specialized talent to compete effectively in this niche market.

The established trust and long-term partnerships Hammond enjoys with major clients like utilities and OEMs create a substantial barrier. Replicating these relationships, which are built on a history of proven reliability and service, requires considerable time and investment for any new player.

Porter's Five Forces Analysis Data Sources

Our Hammond Power Solutions Porter's Five Forces analysis is built upon a robust foundation of data, incorporating information from company annual reports, investor presentations, and industry-specific trade publications. This blend of primary and secondary sources allows for a comprehensive understanding of competitive dynamics.