Family Room Entertainment Corp. Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Family Room Entertainment Corp. Bundle

A Must-Have Tool for Decision-Makers

Family Room Entertainment Corp. faces moderate rivalry and a significant threat from substitutes, impacting its pricing power. Understanding these forces is crucial for navigating the competitive landscape.

The complete report reveals the real forces shaping Family Room Entertainment Corp.’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Highly Specialized Talent

The media industry, including companies like Family Room Entertainment Corp., is heavily reliant on highly specialized talent. Acclaimed writers, directors, actors, and showrunners are scarce resources, and their unique skills and strong personal brands give them considerable leverage. This often translates into demands for higher compensation and greater creative control over projects.

Talent with a history of producing successful, globally appealing content holds even more sway. For instance, in 2024, top-tier actors and showrunners commanding multi-million dollar deals for single projects became increasingly common, reflecting their indispensable role in driving viewership and revenue for major productions.

Concentration of Key Crews and Technicians

The entertainment industry, while appearing vast, often relies on a concentrated pool of highly specialized talent. For Family Room Entertainment Corp., this means key production crews and technical experts in areas like CGI or virtual production can wield significant influence, particularly in markets with scarce skilled labor. These specialized groups, often organized through unions or by virtue of their unique expertise, can negotiate for higher wages and better working conditions, directly impacting Family Room Entertainment Corp.'s production expenses.

Proprietary Equipment and Software Providers

Suppliers of cutting-edge production equipment and specialized software can wield significant bargaining power. For instance, providers of proprietary 8K cinema cameras or advanced AI-driven editing suites often operate with limited competition, driving up costs for companies like Family Room Entertainment Corp. The high initial investment and the learning curve associated with integrating new technology mean that switching suppliers can be prohibitively expensive, often exceeding 15-20% of the annual operating budget for such specialized equipment.

Intellectual Property Holders and Licensors

Intellectual property holders, such as those with rights to popular book series or comic franchises, are significant suppliers for content creators like Family Room Entertainment Corp. These entities hold exclusive rights, making their source material essential. For instance, in 2024, the licensing fees for major children's book franchises can range from hundreds of thousands to millions of dollars annually, depending on the IP's global appeal and existing brand recognition.

Family Room Entertainment Corp. must negotiate favorable licensing terms with these IP owners. The stronger the brand and the wider its appeal, the greater the bargaining power of the licensor. This leverage allows them to dictate terms, impacting Family Room Entertainment Corp.'s production costs and potential profitability.

- High Demand IP: Properties with established fan bases and proven marketability command higher licensing fees.

- Exclusivity Clauses: Licensors often negotiate exclusive rights, limiting Family Room Entertainment Corp.'s ability to adapt the IP for different media without further negotiation.

- Brand Value Correlation: The market value of the intellectual property directly influences the supplier's ability to set premium licensing rates.

Unionized Labor Force

The bargaining power of suppliers for Family Room Entertainment Corp. is significantly shaped by its unionized labor force. Major unions representing writers, actors, directors, and various crew members hold considerable sway, influencing wage rates, benefits, and working conditions through collective bargaining agreements.

These agreements directly impact Family Room Entertainment Corp.'s operational costs and flexibility. For instance, in 2024, the Screen Actors Guild-American Federation of Television and Radio Artists (SAG-AFTRA) strike highlighted the substantial leverage unions possess, leading to increased labor expenses and production delays for many studios.

- Unionized Workforce: Key creative and technical roles are often unionized, granting collective bargaining power.

- Impact on Costs: Union contracts typically set minimum pay scales and residual payments, increasing production budgets.

- Flexibility Constraints: Agreements can limit a company's ability to adjust staffing or production schedules without incurring additional costs or seeking union approval.

- Industry Standards: Union negotiations often set benchmarks for non-unionized talent and crew, indirectly raising overall labor costs across the industry.

Entertainment Suppliers Hold the Cards: Costs Soar

The bargaining power of suppliers for Family Room Entertainment Corp. is notably high due to the specialized nature of talent and intellectual property. Key creative personnel and owners of popular franchises can command premium rates and dictate terms, directly impacting production budgets. For example, in 2024, the average salary for a top-tier showrunner could exceed $5 million per season, underscoring the significant leverage these individuals possess.

Unionized labor further amplifies supplier power, as collective bargaining agreements set industry standards for wages and working conditions. The 2024 SAG-AFTRA negotiations, which resulted in a new contract, led to an estimated 7% increase in minimum compensation for actors, demonstrating the direct cost implications for studios.

| Supplier Type | Bargaining Power Factor | Impact on Family Room Entertainment Corp. | 2024 Data Point |

| Key Creative Talent | Scarcity and proven track record | Higher compensation, creative control demands | Top showrunner salaries > $5M/season |

| Intellectual Property (IP) Owners | Brand recognition and existing fan base | Increased licensing fees, restrictive terms | Major children's book franchise licensing: $100K-$1M+ annually |

| Unionized Labor (e.g., SAG-AFTRA) | Collective bargaining strength | Increased wage costs, benefit contributions | SAG-AFTRA contract led to ~7% minimum pay increase |

| Specialized Production Equipment Providers | Limited competition, high integration costs | Higher equipment rental/purchase costs | Proprietary 8K camera integration: 15-20% of specialized equipment budget |

What is included in the product

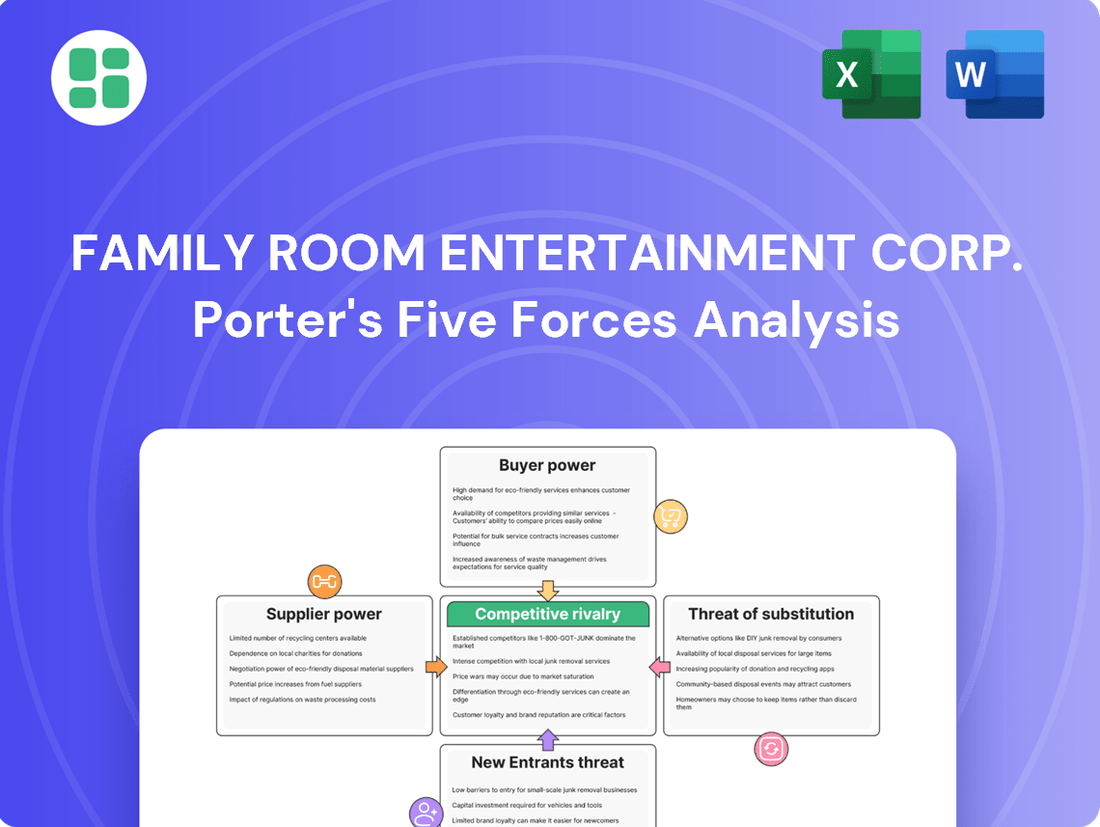

This Porter's Five Forces analysis for Family Room Entertainment Corp. dissects the competitive intensity by examining supplier power, buyer bargaining, threat of new entrants, substitute products, and rivalry among existing firms.

Navigate competitive pressures with a visual breakdown of threats and opportunities, providing actionable insights for Family Room Entertainment Corp.

Customers Bargaining Power

Consolidation of Major Streaming Platforms

The consolidation of major streaming platforms, such as Disney+, Max, and Netflix, significantly amplifies the bargaining power of customers. These giants now represent a substantial portion of the total streaming market, allowing them to exert considerable influence over content creators like Family Room Entertainment Corp. For instance, in 2024, the top three streaming services are projected to capture over 70% of the global paid streaming subscriptions, a clear indicator of their market dominance and, consequently, their enhanced bargaining leverage.

Abundance of Content Producers

The abundance of content producers significantly dilutes the bargaining power of any single entity, including those within Family Room Entertainment Corp. While demand for original content remains high, the sheer volume of independent and studio-backed production companies competing for commissions means platforms aren't reliant on any one provider.

This competitive landscape allows major streaming services and broadcasters to readily pivot between content creators or commission multiple projects concurrently, effectively leveraging the surplus of producers to negotiate more favorable terms. For instance, in 2024, the global content creation market saw a substantial increase in independent studios entering the fray, further intensifying this dynamic.

Backward Integration by Customers

Many major streaming services and broadcast networks are increasingly investing in and expanding their in-house production capabilities. For instance, by 2024, major players like Netflix and Disney+ have significantly scaled their content creation arms, aiming to produce a larger percentage of their library internally. This strategic shift directly reduces their need to license content from external producers.

This move towards backward integration by customers, such as the major streamers, directly weakens the bargaining power of content providers like Family Room Entertainment Corp. When clients can create content themselves, they have less incentive to pay premium licensing fees or negotiate favorable terms with third-party studios, thereby diminishing the producer's leverage.

Data-Driven Content Acquisition

Customers, especially major streaming services, wield significant bargaining power due to their extensive user data. This data informs their content acquisition strategies, making them less responsive to traditional sales tactics. For instance, by analyzing viewing habits, platforms can pinpoint demand for specific genres or talent, influencing Family Room Entertainment Corp.'s production pipeline.

This data-driven approach allows these platforms to dictate terms more effectively. They can demand content tailored to their subscriber base, thereby increasing their leverage in negotiations. In 2024, the streaming market saw continued consolidation and intense competition for subscriber attention, further amplifying the power of these large buyers.

- Data-driven acquisition: Streaming platforms use user data to guide content purchases, reducing reliance on traditional sales pitches.

- Demand for specificity: Platforms can request particular genres, formats, or talent based on viewing analytics.

- Increased buyer control: This data empowers customers, giving them greater influence over Family Room Entertainment Corp.'s content creation.

- Market dynamics in 2024: Intense competition and subscriber focus in the streaming sector amplified buyer leverage.

Global Content Demand and Localized Needs

While the appetite for entertainment content is global, a significant portion of consumers actively seek out programming that resonates with their specific cultural contexts. This preference for localized content empowers customers to diversify their entertainment sources, as numerous international producers can cater to these niche demands. For Family Room Entertainment Corp., this means a constant need to either produce universally appealing content or master the art of hyper-localization. The sheer volume of global content creators, estimated to be in the tens of thousands across various platforms, inherently reduces the bargaining power of any single customer.

The increasing accessibility of diverse international content producers has shifted power towards consumers. For instance, in 2024, the global streaming market saw continued growth, with new players emerging in regions like Southeast Asia and Latin America, offering a broader array of localized content. This fragmentation of supply means that a large customer, like a major streaming platform, can readily switch between providers if Family Room Entertainment Corp. cannot meet their specific content needs or pricing expectations. The ability for customers to access a wide variety of content from different cultural backgrounds means they are less reliant on any single supplier.

- Global Content Consumption: In 2024, global digital media revenues were projected to exceed $2.4 trillion, underscoring the vast market for entertainment content.

- Localized Content Preference: Surveys consistently show that a majority of viewers in key markets prefer content with cultural relevance, impacting viewing habits and platform choices.

- Supplier Diversification: The rise of independent production houses and regional studios worldwide has created a more competitive landscape, offering customers more options.

- Reduced Reliance: Large distributors and platforms can leverage this diverse supply base to negotiate more favorable terms, diminishing the individual bargaining power of content creators like Family Room Entertainment Corp.

Streaming Platforms Dictate Terms to Content Creators

The bargaining power of customers, particularly major streaming platforms, is significantly amplified by their ability to leverage extensive user data. This data allows them to dictate content needs with precision, reducing their reliance on external producers and strengthening their negotiating position. For instance, by 2024, platforms were increasingly demanding content tailored to specific demographic viewing habits, a trend that directly impacts Family Room Entertainment Corp.

The increasing trend of major streaming services and broadcasters investing in their own in-house production capabilities further diminishes the bargaining power of external content creators. By 2024, companies like Netflix and Disney+ had substantially expanded their internal studios, aiming to produce a larger share of their content, thereby reducing their dependence on third-party providers like Family Room Entertainment Corp.

The consolidation of major streaming players, such as Disney+, Max, and Netflix, has concentrated market power, giving these entities substantial leverage over content creators. In 2024, these top platforms were projected to hold over 70% of global paid streaming subscriptions, a clear indicator of their dominance and enhanced bargaining power over companies like Family Room Entertainment Corp.

Preview the Actual Deliverable

Family Room Entertainment Corp. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the competitive landscape for Family Room Entertainment Corp. through Porter's Five Forces, analyzing the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors.

Rivalry Among Competitors

High Number of Competitors

The market for producing both unscripted and scripted entertainment is incredibly crowded. Family Room Entertainment Corp. operates in a landscape populated by thousands of independent production firms, alongside major studios and the internal production divisions of media giants. This sheer volume of players creates a highly competitive environment.

This intense fragmentation means Family Room Entertainment Corp. must constantly vie for essential resources. Securing commissions from networks and streaming platforms, attracting top-tier creative talent, and negotiating favorable distribution agreements are all areas where competition is fierce.

For instance, in 2023, the U.S. Bureau of Labor Statistics reported that over 14,000 establishments were involved in motion picture and sound recording, a figure that captures a broad segment of the content production industry. Many of these are smaller, agile companies capable of rapid adaptation, adding another layer of competitive pressure.

Differentiation Through Intellectual Property and Talent

Family Room Entertainment Corp.'s competitive rivalry hinges on its capacity to secure unique intellectual property and attract elite talent. This differentiation is crucial in a saturated entertainment landscape where distinctive content is the key to audience engagement.

In 2024, the entertainment industry saw significant investment in content creation, with major studios allocating billions to secure compelling narratives and recognizable franchises. Family Room Entertainment Corp. must actively innovate and cultivate a robust portfolio of stories and relationships to carve out its niche and maintain a competitive edge.

Intense Bidding for Projects and Talent

The ongoing 'streaming wars' have intensified competition, leading to aggressive bidding for original content and exclusive talent. This dynamic drives up production costs significantly, making it difficult for mid-sized companies like Family Room Entertainment Corp. to compete purely on price.

In 2024, the global video streaming market was valued at over $100 billion, with major platforms investing heavily in original programming. This fierce bidding environment means Family Room Entertainment Corp. needs to showcase a compelling creative vision and robust financial backing to secure desirable projects and talent.

Low Switching Costs for Buyers

For major platforms and distributors in the entertainment industry, the financial burden of switching content providers is minimal. This low switching cost means they can readily shift their investments and partnerships between different production studios without significant disruption or expense. For instance, a streaming service might easily pivot from commissioning a series from Studio A to Studio B if the latter offers more compelling content or better terms, a flexibility that keeps production companies on their toes.

This ease of substitution directly fuels intense competition among content creators. Production companies must continuously demonstrate their unique value proposition and unwavering reliability to retain and attract business. In 2024, the streaming wars continued to heat up, with platforms like Netflix and Disney+ investing billions in original content, but also showing a willingness to drop underperforming shows or explore new partnerships rapidly. This dynamic forces every studio to innovate and deliver high-quality, cost-effective productions to remain relevant in a buyer’s market.

- Low Switching Costs: Buyers (platforms/distributors) can easily switch between content providers with minimal financial or operational impact.

- Intensified Rivalry: This ease of substitution heightens competition among production companies to prove their worth and secure deals.

- Market Dynamics: In 2024, the streaming sector saw significant content spending, but also a rapid pace of content acquisition and cancellation, underscoring buyer flexibility.

Global Reach and Market Expansion

Family Room Entertainment Corp. faces intense competition as many content creators, including itself, target a worldwide audience. This global ambition means rivals aren't just local; they're international players vying for screen time across different cultures and regulatory landscapes. Understanding varied consumer tastes and navigating diverse legal frameworks becomes crucial for success.

The pursuit of global markets significantly broadens the competitive set. For instance, in 2024, the global media and entertainment market was valued at over $2.5 trillion, indicating a vast but crowded arena. Family Room Entertainment Corp. must contend with established global giants and emerging regional players alike.

- Increased Rivalry: Global expansion introduces a wider array of competitors, from major studios to independent producers in every target region.

- Diverse Market Demands: Success requires adapting content to meet the unique cultural preferences and consumption habits of audiences worldwide.

- Regulatory Hurdles: Operating internationally means complying with varying content regulations, censorship laws, and distribution rights, adding complexity and cost.

- Distribution Challenges: Securing effective distribution channels in new territories can be difficult, often requiring partnerships or significant investment.

Navigating Intense Entertainment Market Competition

Family Room Entertainment Corp. contends with a highly fragmented market, featuring thousands of independent producers alongside major studios. This intense competition means securing commissions, talent, and favorable distribution deals is a constant challenge. The U.S. Bureau of Labor Statistics reported over 14,000 establishments in motion picture and sound recording in 2023, highlighting the sheer volume of players Family Room Entertainment Corp. must navigate.

The ongoing streaming wars, with platforms like Netflix and Disney+ investing billions in original content in 2024, have significantly escalated rivalry. This drives up production costs and necessitates a strong creative vision and financial backing for companies like Family Room Entertainment Corp. to secure projects and talent in a market where buyers have minimal switching costs.

Family Room Entertainment Corp. also faces global competition, as the worldwide media and entertainment market exceeded $2.5 trillion in 2024. This requires adapting content to diverse cultural preferences and navigating varying regulatory landscapes, adding significant complexity and cost to operations.

| Metric | 2023 Data | 2024 Outlook/Trend |

|---|---|---|

| Number of U.S. Motion Picture & Sound Recording Establishments | 14,000+ | Continued high number, with potential for consolidation |

| Global Media & Entertainment Market Value | N/A (Pre-2024 Data) | Over $2.5 trillion |

| Major Streaming Platform Content Investment | Billions | Continued billions in investment, aggressive bidding for IP |

SSubstitutes Threaten

User-Generated Content (UGC) Platforms

User-Generated Content (UGC) platforms like YouTube, TikTok, and Instagram represent a substantial indirect threat to Family Room Entertainment Corp. These platforms allow individuals to create and distribute content at minimal cost, directly competing for audience attention and advertising dollars. In 2024, YouTube alone boasted over 2.7 billion monthly active users, highlighting the sheer scale of this competitive landscape.

This shift towards readily available, often personalized UGC content can significantly alter consumer viewing habits, pulling audiences away from traditional or higher-production value entertainment. For instance, TikTok’s rapid growth, with over 1 billion monthly active users globally by early 2024, demonstrates the powerful draw of short-form, user-driven content that can capture significant engagement.

Interactive Entertainment and Gaming

The threat of substitutes for Family Room Entertainment Corp. within interactive entertainment is significant. Sophisticated video games and immersive virtual reality experiences offer compelling narratives and social engagement, directly competing with traditional passive viewing. This shift means gaming is not just an alternative but a primary entertainment choice for many, vying for leisure time and consumer spending.

In 2024, the global video game market was projected to reach over $200 billion, highlighting the immense scale of this substitute. Furthermore, the rise of cloud gaming services and the increasing accessibility of high-quality gaming on mobile devices broaden the reach of these substitutes, making them readily available to a vast audience that might otherwise engage with Family Room Entertainment Corp.'s offerings.

Live Events and Experiential Entertainment

The threat of substitutes for Family Room Entertainment Corp. is significant, particularly from live events and experiential entertainment. Concerts, sporting events, and theatrical performances offer a unique, in-person social experience that pre-recorded content cannot fully replicate. For instance, the global live music industry was projected to reach over $10 billion in 2024, demonstrating a strong consumer appetite for these out-of-home experiences.

These live activities directly compete for consumers' leisure time and disposable income. As people increasingly seek social engagement and memorable occasions, they may prioritize attending a major sports championship or a popular music festival over staying home. This trend could divert spending and attention away from Family Room Entertainment Corp.'s products, especially if they are perceived as less engaging or unique compared to these tangible, shared experiences.

Podcasts and Audio Content

The burgeoning popularity of podcasts and audiobooks presents a significant threat of substitutes for traditional family room entertainment. Consumers are increasingly turning to audio-first content for narrative and informative experiences, especially during activities like commuting or multitasking. This shift means that time spent listening to podcasts is time not spent watching visual media.

The accessibility and often low cost of this audio content directly compete for consumer attention. For instance, by the end of 2023, it was estimated that over 50% of the US population listened to podcasts, with the average listener consuming roughly seven episodes per week. This widespread adoption highlights a clear alternative to visual entertainment options.

- Podcast Listenership Growth: In 2024, estimates suggest podcast listeners in the US will exceed 160 million people, demonstrating a substantial and growing audience base.

- Audiobook Market Expansion: The audiobook market is also experiencing robust growth, projected to reach over $24 billion globally by 2027, indicating a strong consumer preference for audio content.

- Cost-Effectiveness: Much of this audio content is available for free or through relatively inexpensive subscription models, making it a highly attractive substitute for paid visual entertainment services.

- Engagement During Multitasking: Audio content’s ability to be consumed while performing other tasks provides a unique value proposition that visual media often cannot match, further intensifying its competitive threat.

Emerging Technologies and Metaverse Experiences

The rise of virtual reality (VR), augmented reality (AR), and metaverse platforms presents a significant long-term threat of substitutes for traditional family room entertainment. These immersive technologies offer novel ways for audiences to engage with content, potentially diverting attention from linear media like television or movies. For instance, by 2024, the global VR market was projected to reach over $28 billion, indicating substantial investment and growing consumer interest in these alternative experiences.

These emerging technologies are not just incremental improvements; they represent a paradigm shift in how entertainment can be consumed. Instead of passively watching a show, users can actively participate in virtual worlds or interact with digital elements overlaid on their physical environment. This shift towards interactivity and immersion could make traditional forms of entertainment seem less compelling over time.

The potential impact on Family Room Entertainment Corp. is substantial. Consider these points:

- Growing VR/AR Adoption: Consumer adoption rates for VR and AR devices are steadily increasing, with forecasts suggesting continued growth through 2025.

- Metaverse Investment: Major tech companies are pouring billions into metaverse development, creating robust platforms for future entertainment experiences. In 2024, Meta Platforms alone invested tens of billions into its Reality Labs division, a key indicator of the metaverse's perceived future value.

- Content Innovation: Developers are actively creating unique, interactive content specifically for these platforms, offering experiences that linear media cannot replicate.

- Shifting Consumer Preferences: Younger demographics, in particular, are showing a strong inclination towards digital and interactive forms of entertainment, signaling a potential long-term erosion of traditional viewing habits.

Entertainment Faces Multifaceted Substitute Threats

The threat of substitutes for Family Room Entertainment Corp. is multifaceted, extending beyond direct competitors to alternative leisure activities. User-generated content platforms like YouTube and TikTok, with billions of active users in 2024, capture significant audience attention and advertising revenue. Similarly, the booming video game industry, projected to exceed $200 billion in 2024, offers interactive and social experiences that directly vie for consumers' time and money.

Live events, including concerts and sporting matches, provide unique social engagement, with the live music industry alone expected to reach over $10 billion in 2024. Furthermore, the growing popularity of podcasts and audiobooks, with over 160 million estimated US listeners in 2024, offers a convenient and often low-cost alternative for narrative consumption during multitasking activities.

| Substitute Category | Key Platforms/Examples | 2024 Estimated Market Size/User Base | Key Threat Factor |

| User-Generated Content | YouTube, TikTok, Instagram | YouTube: 2.7 billion+ monthly active users | Captures audience attention and advertising dollars with low-cost, readily available content. |

| Interactive Entertainment | Video Games, VR Experiences | Video Game Market: $200 billion+ | Offers immersive narratives and social engagement, competing for leisure time and spending. |

| Live & Experiential Events | Concerts, Sporting Events, Theatre | Live Music Industry: $10 billion+ | Provides unique, in-person social experiences that divert leisure time and disposable income. |

| Audio Content | Podcasts, Audiobooks | US Podcast Listeners: 160 million+ | Offers convenient, low-cost consumption during multitasking, directly competing for attention. |

Entrants Threaten

High Capital Requirements for Premium Content

Producing premium, unscripted, and scripted entertainment content for a global audience demands significant upfront capital. For instance, major studio productions can easily cost tens to hundreds of millions of dollars for a single series or film. This substantial financial commitment, covering everything from top-tier talent and experienced production crews to cutting-edge equipment and extensive post-production, creates a formidable barrier for new companies lacking deep pockets or established financial relationships.

Difficulty in Securing Distribution Channels

Family Room Entertainment Corp. faces a significant threat from new entrants due to the difficulty in securing essential distribution channels. Established players like Netflix and Disney+ often prioritize content from established studios with proven success, leaving newcomers struggling for visibility. In 2024, the streaming market continued to consolidate, with major platforms investing heavily in original content, further raising the barrier for independent producers to gain access and reach a wide audience.

Need for Established Talent Relationships and IP

Family Room Entertainment Corp.'s success hinges on its deep-seated relationships with seasoned talent and its valuable intellectual property (IP) portfolio. Newcomers struggle to replicate these established networks, which are vital for attracting premier creative projects and securing essential talent.

In 2024, the media and entertainment industry saw continued consolidation, with larger players leveraging their existing IP and talent relationships to dominate. For instance, major studios continued to mine their extensive back catalogs for remakes and sequels, a strategy that requires pre-existing IP and established creative teams, posing a significant barrier for new entrants.

Brand Recognition and Reputation Building

Building a strong brand and a successful content library is a considerable undertaking, requiring substantial time and financial resources. Family Room Entertainment Corp. leverages its established reputation, whereas new competitors face the hurdle of earning trust and credibility with both consumers and creative talent in a crowded marketplace.

New entrants must invest heavily in marketing and content development to even begin to rival the brand recognition Family Room Entertainment Corp. has cultivated over years of operation. For instance, in 2024, the average cost for a major studio to produce and market a tentpole film exceeded $200 million, illustrating the significant capital required to make an impact.

- Significant Capital Investment: New entrants need substantial funding to develop quality content and establish brand awareness, often in the hundreds of millions of dollars.

- Time to Build Reputation: It can take years, even decades, for a new entertainment company to build a reputation comparable to established players like Family Room Entertainment Corp.

- Talent Acquisition Challenges: Attracting top-tier talent is difficult for newcomers, as established companies often offer better deals and a proven track record.

- Consumer Trust Factor: Consumers are more likely to spend money on content from brands they know and trust, creating a barrier for new entrants.

Regulatory and Legal Complexities

The media industry is heavily regulated, and new entrants to family room entertainment face significant hurdles. Navigating complex media regulations, intellectual property rights, international co-production treaties, and labor laws requires substantial investment in legal expertise and compliance. For instance, in 2024, the global media and entertainment market was valued at over $2.5 trillion, with a significant portion subject to diverse national and international legal frameworks.

These regulatory and legal complexities act as a considerable barrier to entry. New companies must dedicate considerable resources to understanding and adhering to these rules to operate effectively on a global scale. This adds a significant operational burden and cost, making it challenging for smaller or newer players to compete with established entities that already have robust legal departments and compliance systems in place.

- Regulatory Hurdles: Family room entertainment companies must comply with broadcasting standards, content rating systems, and data privacy laws, which vary significantly by region.

- Intellectual Property: Protecting copyrights, trademarks, and licensing agreements is paramount, requiring constant vigilance and legal defense against infringement.

- International Treaties: Co-production treaties and distribution agreements across borders necessitate understanding and adhering to a web of international legal obligations.

- Labor Laws: Compliance with diverse labor laws, especially for international productions, adds another layer of complexity and potential cost for new entrants.

Entertainment Industry: Moderate Threat, High Entry Barriers

The threat of new entrants for Family Room Entertainment Corp. is moderate, primarily due to the substantial capital required for content production and distribution. Newcomers face immense challenges in securing the necessary funding, which can run into the hundreds of millions of dollars for a single high-quality production. Furthermore, the established relationships with talent and the existing intellectual property (IP) held by companies like Family Room Entertainment Corp. create significant hurdles for any new player attempting to gain traction in the market.

| Barrier to Entry | Description | 2024 Relevance |

| Capital Requirements | High upfront investment for content creation and marketing. | Major studio productions can exceed $200 million for a single film. |

| Distribution Access | Difficulty securing slots on established streaming platforms. | Consolidation in streaming market favors established content providers. |

| Brand Recognition & Trust | Time and resources needed to build consumer and talent loyalty. | Consumers prefer established, trusted brands for entertainment spending. |

| Talent & IP Advantage | Established relationships with talent and existing IP are hard to replicate. | Studios leverage back catalogs for remakes, requiring pre-existing IP. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Family Room Entertainment Corp. is built upon a foundation of robust data, including industry-specific market research reports, competitor financial filings, and consumer trend surveys. We also incorporate insights from trade association publications and economic indicators relevant to the entertainment sector.