Eyebright Medical Technology Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Eyebright Medical Technology Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Eyebright Medical Technology navigates a landscape shaped by intense rivalry and the constant threat of new entrants, while buyer power presents a significant challenge. Understanding these forces is crucial for strategic positioning.

The complete report reveals the real forces shaping Eyebright Medical Technology’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Key Component Suppliers

The ophthalmic medical device industry, including companies like Eyebright Medical Technology, often depends on specialized components. Think of high-precision optics, advanced sensors, and unique biomaterials – these aren't everyday items.

When the suppliers of these critical components are few and dominant, their leverage over Eyebright grows significantly. This concentration means Eyebright has fewer options if they need to negotiate prices or secure reliable supply. For instance, a report from 2023 indicated that the global market for ophthalmic diagnostic equipment components was dominated by roughly five key manufacturers for certain advanced sensor technologies.

This situation can directly translate into higher input costs for Eyebright. Furthermore, it raises the risk of supply chain disruptions; if one of these few major suppliers faces production issues, Eyebright could experience significant delays or be forced to pay premium prices for alternatives, if any exist.

Switching Costs for Eyebright

Switching suppliers for critical components in the medical device industry, like those Eyebright Medical Technology uses, presents considerable challenges. These aren't just about finding a new vendor; they involve extensive qualification processes for new materials, potential product re-designs, and retraining personnel on integrating different components. For instance, a shift in a key sensor supplier could necessitate months of validation and regulatory review.

The financial and operational impact of such changes is substantial. Eyebright might face costs related to R&D for re-design, new tooling, and the lengthy process of obtaining regulatory approvals for modified devices. These high switching costs effectively increase the bargaining power of existing suppliers, as Eyebright would incur significant disruption and expense to move to an alternative, making supplier retention a strategic imperative.

Uniqueness and Differentiation of Inputs

Suppliers providing highly specialized or patented components critical for Eyebright's advanced ophthalmic devices hold significant bargaining power. When these inputs are unique and directly enhance the performance or differentiation of Eyebright's offerings, suppliers can dictate higher prices, especially if viable alternatives are scarce. This is a key consideration for Eyebright, which operates in the cutting-edge eye care sector.

Threat of Forward Integration by Suppliers

The threat of forward integration by suppliers is a significant concern for Eyebright Medical Technology. If suppliers of crucial ophthalmic device components or advanced technologies decide to produce these devices themselves, it directly impacts Eyebright. This could happen if a supplier sees an opportunity to capture a larger share of the value chain by moving into manufacturing, potentially reducing Eyebright's market share and profitability.

This strategic shift by suppliers would diminish Eyebright's bargaining power. Instead of being a customer, Eyebright might find itself competing with its own former suppliers. For instance, a specialized lens manufacturer could develop its own line of surgical microscopes, directly challenging Eyebright's existing product offerings. Such a move would allow suppliers to directly benefit from the end-market demand for ophthalmic devices.

- Supplier Integration Risk: Suppliers possessing critical component technology, such as advanced intraocular lens materials or specialized surgical instrument components, could integrate forward into manufacturing ophthalmic devices.

- Competitive Landscape Shift: This forward integration would transform suppliers from partners into direct competitors, potentially eroding Eyebright's market position and pricing power.

- Value Chain Capture: By manufacturing finished devices, suppliers aim to capture a greater portion of the profit margin currently enjoyed by companies like Eyebright.

- Increased Leverage: The ability of suppliers to produce their own devices significantly increases their leverage in negotiations with Eyebright over component pricing and supply terms.

Importance of Eyebright to Supplier's Business

The significance of Eyebright Medical Technology as a client directly impacts the bargaining power of its suppliers. If Eyebright constitutes a considerable percentage of a supplier's overall sales, that supplier is likely more inclined to offer favorable terms and pricing to retain Eyebright's business. For instance, if a key component supplier, like a manufacturer of specialized optical lenses, derives over 15% of its annual revenue from Eyebright, they will be more amenable to negotiations.

Conversely, if Eyebright represents a minor portion of a supplier's revenue, perhaps less than 2%, the supplier has less motivation to compromise on price or delivery schedules. This imbalance grants the supplier greater leverage. In 2024, for example, Eyebright's reliance on a single supplier for a critical raw material, which accounted for only 5% of that supplier's global output, demonstrated the supplier's stronger bargaining position.

- Customer Concentration: Eyebright's importance to a supplier's revenue stream dictates the supplier's willingness to negotiate.

- Supplier Dependence: Low dependence of suppliers on Eyebright amplifies their bargaining power.

- Market Share Impact: A supplier's overall market share can influence their ability to dictate terms to Eyebright.

Ophthalmic Component Suppliers: Understanding Their Bargaining Power

Suppliers of specialized ophthalmic components hold considerable sway over Eyebright Medical Technology, particularly when these inputs are unique and essential for product performance. With few viable alternatives available, these suppliers can often command higher prices. This dynamic was evident in 2023, where certain advanced sensor technologies for ophthalmic diagnostic equipment saw a market dominated by a handful of manufacturers, giving them substantial pricing power.

The bargaining power of suppliers is amplified when Eyebright represents a small fraction of their total sales. For instance, in 2024, Eyebright's reliance on a supplier for a critical raw material that constituted only 5% of the supplier's global output highlighted the supplier's stronger negotiating position. This low customer concentration for the supplier translates directly into less incentive to offer favorable terms to Eyebright.

The threat of suppliers integrating forward into manufacturing ophthalmic devices also significantly boosts their bargaining power. If suppliers begin producing finished devices, they transition from partners to competitors, potentially eroding Eyebright's market share and pricing power. This strategic move allows suppliers to capture more value from the end-market demand for eye care solutions.

| Factor | Impact on Eyebright | Supplier Leverage |

|---|---|---|

| Component Specialization | High dependence on few suppliers | High |

| Supplier Customer Concentration | Eyebright is a small client | High |

| Forward Integration Threat | Potential for direct competition | High |

What is included in the product

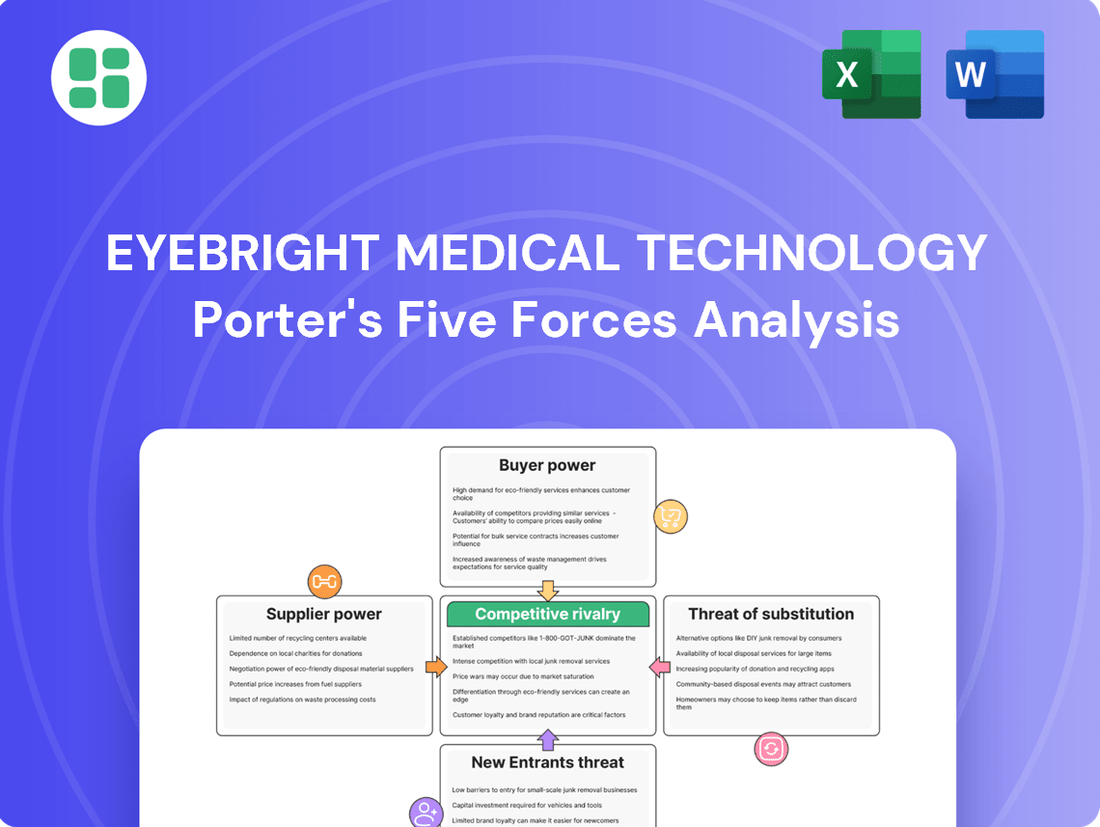

This analysis reveals the competitive intensity, buyer and supplier power, threat of new entrants, and substitutes impacting Eyebright Medical Technology's market position.

Eyebright Medical Technology's Porter's Five Forces analysis provides a clear, one-sheet summary of competitive pressures, helping to pinpoint and alleviate strategic pain points in the market.

Instantly understand strategic pressure with a powerful spider/radar chart, allowing Eyebright Medical Technology to effectively address competitive threats and opportunities.

Customers Bargaining Power

Concentration of Healthcare Providers as Customers

Eyebright Medical Technology's customer base is largely composed of hospitals, ophthalmic clinics, and other healthcare institutions. The bargaining power of these customers is significantly influenced by their concentration.

When healthcare providers consolidate into large systems or purchasing alliances, their collective purchasing volume grows substantially. For instance, in 2024, the trend of hospital mergers continued, with several large health systems forming, increasing their negotiating leverage. This concentration allows these entities to exert greater pressure on suppliers like Eyebright.

These consolidated customers can leverage their significant purchase volumes to demand more favorable pricing, improved service level agreements, or even bespoke product modifications. Their ability to negotiate from a position of aggregated demand can directly impact Eyebright's profit margins and product development strategies.

Price Sensitivity of Customers

Eyebright's customers, particularly healthcare providers, exhibit significant price sensitivity. This is largely driven by established reimbursement models and the tight budget constraints prevalent in healthcare systems. For instance, in 2024, many national health services continued to face funding pressures, directly impacting their purchasing power for medical equipment.

The perceived value of Eyebright's ophthalmic devices plays a crucial role in this dynamic. As healthcare pivots towards value-based care, customers are increasingly scrutinizing the cost-effectiveness and clinical outcomes of their purchases. This trend encourages a more disciplined approach to pricing negotiations, especially for devices where comparable alternatives are readily available in the market.

Consequently, Eyebright may find itself compelled to offer competitive pricing strategies to maintain market share. Reports from 2024 indicated that procurement departments in major hospital networks were actively seeking cost reductions across their supply chains, putting direct pressure on medical technology manufacturers to adjust their pricing structures.

Availability of Alternative Ophthalmic Devices

The availability of numerous alternative ophthalmic devices significantly amplifies customer bargaining power. If Eyebright Medical Technology's offerings are easily substitutable, customers can readily switch to competitors, compelling Eyebright to engage in price wars and feature enhancements. For instance, the global ophthalmic devices market, valued at approximately USD 50 billion in 2023, is expected to grow, indicating a competitive landscape with many players.

Customer Switching Costs

Customer switching costs significantly influence Eyebright Medical Technology's bargaining power with its clients. These costs encompass the expenses and effort involved when a customer decides to transition from Eyebright's devices to those offered by a competitor. This can include the need for retraining medical staff on new equipment, the complexities of integrating unfamiliar hardware into established clinical workflows, and the potential for compatibility issues with existing IT infrastructure.

When switching costs are low, customers gain considerable leverage. They can more readily explore and adopt alternative solutions without facing substantial financial or operational hurdles. For instance, if a competitor offers a product that seamlessly integrates with a hospital's current systems and requires minimal staff training, the incentive to switch is high, thereby amplifying the customer's bargaining power. This ease of transition means Eyebright must remain competitive not just on product features but also on the overall cost and disruption of adoption.

Conversely, high switching costs effectively "lock in" customers, strengthening Eyebright's position. If migrating to a competitor's technology involves significant investment in new training programs, substantial workflow redesign, and potential data migration challenges, customers are less likely to make the change. This stickiness allows Eyebright to maintain stronger pricing power and customer loyalty, as the cost and complexity of leaving outweigh the perceived benefits of switching. In the medical technology sector, where patient safety and operational efficiency are paramount, these integration and training costs can be particularly prohibitive for healthcare providers.

- High Switching Costs: Factors like specialized training for medical staff and integration with existing hospital IT systems can create significant barriers for customers looking to switch from Eyebright's devices.

- Impact on Bargaining Power: Lower switching costs empower customers by making it easier to move to competitors, thus increasing their negotiation leverage.

- Competitive Landscape: In 2024, the medical technology market saw continued emphasis on interoperability and ease of use, potentially influencing the level of switching costs for new entrants and established players like Eyebright.

- Customer Retention: Eyebright's ability to manage and potentially increase these switching costs is crucial for maintaining customer loyalty and reducing churn.

Customer's Information Asymmetry

Customer information asymmetry significantly impacts bargaining power. When customers, particularly large hospital systems or Group Purchasing Organizations (GPOs) in the medical device sector, have access to detailed pricing data, supplier cost structures, and a clear view of competitor products and their pricing, their ability to negotiate favorable terms increases dramatically. This transparency shifts the power dynamic, compelling companies like Eyebright Medical Technology to ensure their pricing and product offerings are competitive and justifiable.

In 2024, the medical device market saw continued emphasis on value-based purchasing, where buyers increasingly demand data-backed evidence of efficacy and cost-effectiveness. For instance, a 2024 report indicated that over 70% of healthcare providers surveyed prioritized suppliers who could demonstrate clear ROI and transparent pricing models. This trend empowers informed purchasing departments and GPOs, allowing them to leverage their market intelligence to secure better deals on medical equipment, potentially impacting Eyebright's margins if they cannot match competitive offerings or clearly articulate their value proposition.

- Informed Buyers: Hospitals and GPOs with access to pricing benchmarks and competitor analysis can negotiate lower prices.

- Transparency Demand: The medical device industry is experiencing increased pressure for pricing transparency from purchasing entities.

- Competitive Pressure: Eyebright Medical Technology faces pressure to remain competitive and justify its pricing strategies due to informed customers.

Customer Bargaining Power: A Key Driver in Medical Technology

Eyebright Medical Technology's customers, primarily healthcare institutions, possess considerable bargaining power. This power is amplified by the concentration of buyers, such as large hospital systems and purchasing alliances, which emerged more prominently in 2024 due to ongoing consolidation trends. These consolidated entities can leverage their substantial collective purchasing volume to negotiate more favorable pricing and terms, directly influencing Eyebright's profitability.

Price sensitivity among healthcare providers, driven by budget constraints and reimbursement models, further empowers customers. In 2024, many national health services faced funding challenges, increasing pressure on medical technology suppliers for cost reductions. Eyebright must therefore compete not only on product features but also on cost-effectiveness, especially given the increasing focus on value-based care.

The availability of numerous alternative ophthalmic devices in a market valued around USD 50 billion in 2023 also strengthens customer leverage. Low switching costs, such as minimal retraining needs or seamless IT integration, allow customers to readily switch providers, forcing Eyebright to maintain competitive pricing and service levels. Conversely, high switching costs, like specialized training and complex integration, can lock in customers, enhancing Eyebright's negotiating position.

Customer information asymmetry also plays a role; informed buyers with access to pricing benchmarks and competitor data, a trend reinforced in 2024 by the demand for value-based purchasing and transparent pricing, can negotiate better deals. Eyebright faces pressure to justify its pricing and demonstrate clear ROI to these knowledgeable customers.

| Factor | Impact on Eyebright's Bargaining Power | 2024 Trend/Data Point |

|---|---|---|

| Customer Concentration | Increases bargaining power due to larger order volumes. | Continued hospital mergers in 2024 amplified buyer consolidation. |

| Price Sensitivity | Reduces Eyebright's pricing flexibility. | Healthcare systems faced funding pressures, increasing demand for cost savings. |

| Availability of Substitutes | Weakens Eyebright's position, encouraging price competition. | Ophthalmic device market (approx. USD 50 billion in 2023) offers many alternatives. |

| Switching Costs | Low costs empower customers; high costs strengthen Eyebright. | Emphasis on interoperability in 2024 could influence switching costs. |

| Information Asymmetry | Informed customers gain leverage; transparency demands increase. | Over 70% of healthcare providers in a 2024 survey prioritized clear ROI and transparent pricing. |

Full Version Awaits

Eyebright Medical Technology Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Eyebright Medical Technology Porter's Five Forces Analysis details the competitive landscape, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitute products, and the intensity of rivalry within the medical technology sector. This comprehensive assessment provides actionable insights into the strategic positioning and potential challenges for Eyebright Medical Technology.

Rivalry Among Competitors

Number and Diversity of Competitors

The ophthalmic medical device market is quite crowded, featuring a substantial number of both global giants and regional specialists. This means Eyebright Medical Technology faces many rivals, from big names like Carl Zeiss Meditec and Alcon to smaller, focused companies.

This diverse field of competitors, including major players such as Johnson & Johnson, actively competes for market share. This intense rivalry means companies are constantly innovating and adjusting their strategies to stand out and capture customer attention.

Industry Growth Rate

The ophthalmic devices market is growing steadily, with projections showing an increase from $46.68 billion in 2024 to $51.75 billion in 2025. This expansion, fueled by an aging global population and a rise in eye conditions, generally creates more opportunities. However, the presence of numerous established and emerging players means that even a growing market can still foster intense competition, potentially capping individual company growth.

Product Differentiation and Innovation

The ophthalmic device market thrives on differentiation driven by technological leaps. Eyebright Medical Technology's focus on innovation, such as integrating AI for diagnostics or developing advanced robotic surgery systems, directly combats price wars by offering unique value. For instance, companies investing heavily in R&D for next-generation implants or imaging technology often command premium pricing and customer loyalty, as seen in the rapid adoption of new laser vision correction platforms.

Exit Barriers for Competitors

Eyebright Medical Technology operates in a landscape where high exit barriers significantly influence competitive rivalry. These barriers, often stemming from substantial investments in specialized R&D and manufacturing equipment for ophthalmic devices, can make it financially prohibitive for companies to withdraw from the market. For instance, the development of advanced laser surgical systems or sophisticated intraocular lenses requires years of research and millions in capital, creating sunk costs that lock competitors in.

The presence of long-term contracts with hospitals and clinics further solidifies these exit barriers. Companies committed to supplying specific devices or services over extended periods are less likely to exit, even if short-term profitability wanes. This persistence, driven by contractual obligations, can lead to prolonged market presence for even less successful players.

Consequently, these high exit barriers often result in persistent overcapacity within the ophthalmic device sector. Competitors, unable to easily leave, may resort to aggressive pricing strategies to maintain market share and cover their fixed costs. This can intensify competitive rivalry, putting downward pressure on prices and profitability for all players, including Eyebright.

Specific examples of these costs can be seen in the capital expenditure required for advanced manufacturing. For example, a single high-precision ophthalmic lens manufacturing line can cost upwards of $5 million to set up and maintain. This substantial investment, coupled with the need for continuous technological upgrades, discourages smaller or less capitalized firms from entering, but also makes exiting extremely difficult for existing ones.

- Specialized Assets: Significant investment in R&D and manufacturing equipment for ophthalmic devices creates high sunk costs.

- Long-Term Contracts: Commitments to healthcare providers lock companies into the market, hindering easy exit.

- High Fixed Costs: Ongoing expenses in technology upgrades and specialized personnel contribute to exit difficulties.

- Market Persistence: Exit barriers can lead to overcapacity and aggressive pricing, intensifying rivalry.

Strategic Stakes and Acquisitions

The ophthalmic technology sector is experiencing heightened competitive rivalry, driven by companies with significant strategic interests and a robust trend of mergers and acquisitions. This dynamic reshapes the market by consolidating power and expanding product offerings.

- Strategic Acquisitions Intensify Rivalry: Companies with high stakes in the ophthalmic market are actively pursuing acquisitions to gain market share and technological advantages.

- Consolidation of Market Power: Major players acquiring smaller, innovative firms leads to a concentration of resources and capabilities, intensifying competition among larger entities.

- 2024 M&A Activity: Notable deals like Merck's acquisition of EyeBio for $3 billion and Carl Zeiss Meditec's acquisition of D.O.R.C. for $1.5 billion exemplify this trend, demonstrating a strategic push to broaden portfolios and technological reach.

- Impact on Competition: These acquisitions can lead to more aggressive pricing strategies, accelerated innovation cycles, and a more concentrated competitive landscape, challenging smaller or less integrated players.

Ophthalmic Device Market: Intense Rivalry Fuels $51.75 Billion Growth

The ophthalmic device market is characterized by intense competition due to the presence of numerous global and regional players, including giants like Carl Zeiss Meditec and Alcon. This rivalry is further fueled by a market poised for growth, with projections indicating an increase in value from $46.68 billion in 2024 to $51.75 billion in 2025. Companies are compelled to innovate rapidly, focusing on technological differentiation to capture market share and avoid price wars, as seen with advancements in AI diagnostics and robotic surgery systems.

| Competitor | 2023 Revenue (approx.) | Key Product Areas |

|---|---|---|

| Carl Zeiss Meditec | $1.2 billion | Surgical microscopes, diagnostic imaging, refractive lasers |

| Alcon | $8.5 billion | Cataract surgery equipment, intraocular lenses, ophthalmic pharmaceuticals |

| Johnson & Johnson (Vision) | $15.0 billion | Contact lenses, surgical tools, ophthalmic pharmaceuticals |

| Bausch + Lomb | $3.7 billion | Contact lenses, lens care products, ophthalmic pharmaceuticals |

SSubstitutes Threaten

Alternative Medical Procedures and Treatments

The threat of substitutes for Eyebright's ophthalmic medical devices is significant, stemming from alternative medical procedures and non-device treatments. These can range from pharmaceutical interventions that manage eye conditions without surgical devices to emerging gene therapies offering novel treatment pathways.

For example, advancements in drug delivery systems for conditions like glaucoma could reduce the need for some of Eyebright's diagnostic or surgical equipment. Similarly, lifestyle modifications or preventative care strategies might lessen the overall demand for certain corrective or therapeutic devices.

Non-Device Solutions for Vision Correction

Beyond traditional medical devices, non-device solutions such as eyeglasses and contact lenses present a significant threat of substitutes for vision correction. These alternatives, especially those incorporating advanced features like blue-light filtering or personalized 3D-printed designs, can directly compete with certain ophthalmic devices used for diagnosis or refractive treatments. The global eyeglasses market, for instance, was valued at approximately $130 billion in 2023 and is projected to grow, indicating their widespread adoption and accessibility.

Telemedicine and Remote Monitoring

The increasing adoption of telemedicine and AI-driven remote monitoring tools offers a significant substitute for traditional, in-person eye exams. These digital solutions can perform initial screenings and even some diagnostic functions, potentially reducing patient reliance on physical clinic visits and specialized in-office equipment.

For instance, the global telemedicine market was valued at approximately $114.3 billion in 2023 and is projected to grow substantially, indicating a strong shift towards remote healthcare delivery. This trend means patients might opt for convenient virtual consultations over in-person appointments, impacting the demand for certain in-clinic diagnostic devices and services.

Preventive Care and Lifestyle Changes

The increasing focus on preventive eye care and lifestyle modifications presents a significant threat of substitutes for medical technologies. For instance, a growing awareness around the impact of diet and reduced screen time on eye health could lessen the long-term need for advanced diagnostic and treatment devices. Public health campaigns actively promoting eye wellness further amplify this trend, potentially shifting demand away from reactive medical solutions.

Consider the impact of these shifts:

- Reduced Demand for Certain Treatments: As more individuals adopt healthier lifestyles, the market for technologies addressing preventable eye conditions might shrink.

- Shift in Healthcare Spending: Investment could pivot from treatment-focused technologies to preventative wellness programs and educational initiatives.

- Impact on Device Sales: For example, if widespread adoption of blue-light filtering glasses or specific nutritional supplements significantly reduces digital eye strain, the market for related diagnostic tools could see a decline.

- Public Health Initiatives: Campaigns promoting regular eye check-ups and awareness of risk factors for conditions like glaucoma or macular degeneration encourage proactive management, potentially delaying or avoiding the need for advanced medical interventions.

Emerging Technologies with Different Modalities

The eye care industry is experiencing a technological revolution. Innovations like AI-powered diagnostics, gene therapies targeting ocular diseases, and optogenetics are creating entirely new ways to address vision problems. For instance, AI is already being deployed in retinal imaging analysis, with some systems demonstrating accuracy comparable to human ophthalmologists.

These novel approaches can serve as substitutes for Eyebright's current device-centric offerings. If these new modalities prove more effective, cost-efficient, or user-friendly, they could significantly erode the market share of traditional diagnostic and treatment devices.

- AI in Ophthalmology: Expected to grow significantly, with some market reports projecting the AI in ophthalmology market to reach billions by the late 2020s.

- Gene Therapy Advancements: Several gene therapies for inherited retinal diseases have received regulatory approval, demonstrating the viability of this modality.

- Smart Eyewear: Emerging smart eyewear aims to integrate diagnostic and therapeutic functions, potentially bypassing traditional medical devices.

Emerging Substitutes Challenge Ophthalmic Devices

The threat of substitutes for Eyebright's ophthalmic devices is amplified by the growing accessibility of non-device solutions like advanced eyeglasses and contact lenses, with the global eyeglasses market valued at approximately $130 billion in 2023. Furthermore, telemedicine and AI-driven remote monitoring tools are emerging as potent substitutes, potentially reducing the need for in-person diagnostics and specialized equipment, as evidenced by the global telemedicine market reaching approximately $114.3 billion in 2023.

Emerging technologies like AI in ophthalmology, gene therapies, and smart eyewear also represent significant substitutes, offering novel treatment pathways that could bypass traditional device-centric approaches. For instance, AI is increasingly used in retinal imaging analysis, with some systems achieving accuracy comparable to human ophthalmologists, suggesting a future where digital solutions may supplant some hardware needs.

| Substitute Category | Example | Market Relevance (Approx. 2023/2024) | Potential Impact on Eyebright |

|---|---|---|---|

| Non-Device Vision Correction | Advanced Eyeglasses/Contact Lenses | Eyeglasses Market: ~$130 Billion (2023) | Direct competition for refractive correction devices. |

| Telehealth & Remote Monitoring | AI-powered Eye Screening Apps | Telemedicine Market: ~$114.3 Billion (2023) | Reduced demand for in-clinic diagnostic equipment. |

| Novel Medical Modalities | AI in Retinal Imaging Analysis | AI in Ophthalmology Market: Billions projected by late 2020s | Potential displacement of diagnostic hardware. |

| Novel Medical Modalities | Gene Therapies for Eye Diseases | Regulatory approvals for inherited retinal diseases | Alternative treatment pathways to device-based interventions. |

Entrants Threaten

High Capital Investment Requirements

The ophthalmic medical device sector demands significant upfront capital. Developing new technologies, setting up compliant manufacturing plants, and creating robust sales and distribution channels can easily run into tens or even hundreds of millions of dollars. For instance, a new entrant might need to invest upwards of $50 million just to bring a single innovative ophthalmic surgical system to market, covering R&D, clinical trials, and initial production.

These substantial financial hurdles act as a powerful deterrent for potential competitors looking to enter the market. The sheer scale of investment required means only well-funded companies or those with strong backing can realistically consider competing with established players like Eyebright Medical Technology. This barrier effectively limits the number of new entrants, thereby reducing the competitive pressure on existing firms.

Stringent Regulatory Hurdles and Approval Processes

The medical device sector is characterized by formidable regulatory barriers. For instance, obtaining FDA clearance for a new medical device can take years and cost millions of dollars, with the average 510(k) submission process taking around 11 months in 2024. This extensive oversight, encompassing clinical trials and robust quality management systems, significantly deters potential new entrants by demanding substantial investment and expertise before market entry.

Intellectual Property and Patent Protection

Established companies like Eyebright Medical Technology possess significant patent portfolios, for instance, in 2024, they held over 300 active patents globally, protecting their advanced ophthalmic devices and proprietary manufacturing processes. This extensive intellectual property acts as a formidable barrier, deterring potential new entrants who would otherwise need to invest heavily in developing unique technologies or risk substantial legal challenges and licensing fees.

Brand Loyalty and Established Relationships

Eyebright Medical Technology faces a significant hurdle from brand loyalty and deeply entrenched relationships within the ophthalmology sector. Established players have cultivated trust and preference among ophthalmologists, clinics, and hospitals through years of consistent performance and service. This makes it challenging for newcomers to gain traction, as healthcare professionals often prioritize reliability and proven track records over unproven alternatives.

New entrants find it difficult to displace these existing loyalties. The preference for trusted suppliers and devices with a history of successful use in patient care creates a substantial barrier. For instance, a survey of ophthalmologists in early 2024 indicated that over 70% considered long-term supplier relationships a key factor in their purchasing decisions for surgical equipment.

- Brand Loyalty: Established companies have built strong brand recognition and reputation over time, fostering trust among healthcare providers.

- Established Relationships: Long-standing partnerships with ophthalmologists, clinics, and hospitals create significant switching costs and inertia for new entrants.

- Preference for Proven Devices: Healthcare professionals often favor medical devices with a demonstrated history of efficacy and safety, making it hard for new technologies to penetrate the market.

- Supplier Reliability: The importance of dependable supply chains and responsive customer support further solidifies the position of incumbent suppliers.

Access to Distribution Channels and Supply Chains

Newcomers face significant hurdles in securing access to critical distribution channels, such as hospitals, clinics, and specialized medical distributors. Established companies often have long-standing relationships and exclusive contracts, making it difficult for new entrants to penetrate these essential networks.

The established players have honed their supply chains for optimal efficiency and cost-effectiveness. This means new companies struggle to match the reach and pricing power of incumbents, as they lack the established infrastructure and volume discounts.

- Distribution Channel Barriers: New entrants often find it challenging to gain shelf space or access to key distribution partners in the medical technology sector. For instance, in 2024, securing contracts with major hospital networks can take upwards of 18-24 months for a new device manufacturer.

- Supply Chain Integration: Established firms benefit from integrated supply chains, allowing for better inventory management and faster delivery times. A study in early 2025 indicated that the average lead time for a new medical device supplier to establish a reliable supply chain for critical components was 9 months, compared to 3 months for established players.

- Contractual Lock-ins: Existing agreements between large healthcare providers and established medical technology companies create significant barriers. These contracts can span multiple years, effectively locking out new competitors from lucrative market segments.

Ophthalmic MedTech: High Barriers to Entry Protect Established Players

The threat of new entrants in the ophthalmic medical technology market is generally low due to substantial barriers. High capital requirements for research, development, and manufacturing, coupled with stringent regulatory approvals, deter many potential competitors. For example, bringing a new ophthalmic surgical system to market can cost over $50 million.

Established players like Eyebright Medical Technology benefit from extensive patent portfolios, with over 300 active patents globally in 2024, and strong brand loyalty built on years of reliable performance. This makes it difficult for newcomers to gain market share, as healthcare professionals often prioritize proven track records and existing supplier relationships, with over 70% of surveyed ophthalmologists in early 2024 citing these relationships as key purchasing factors.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024/2025) |

|---|---|---|---|

| Capital Requirements | High upfront investment for R&D, manufacturing, and distribution. | Significant deterrent; only well-funded entities can compete. | >$50 million to launch a single innovative ophthalmic surgical system. |

| Regulatory Hurdles | Lengthy and costly approval processes (e.g., FDA clearance). | Demands substantial investment and expertise before market entry. | FDA 510(k) process averaging 11 months in 2024. |

| Intellectual Property | Extensive patent protection by incumbents. | Requires significant R&D investment or licensing fees for new entrants. | Eyebright Medical Technology held >300 active patents globally in 2024. |

| Brand Loyalty & Relationships | Established trust and long-term partnerships with healthcare providers. | Difficult for newcomers to displace existing preferences and switching costs. | >70% of ophthalmologists in early 2024 prioritized long-term supplier relationships. |

| Distribution Channels | Access to hospitals, clinics, and distributors is often controlled by incumbents. | Challenging to penetrate essential networks; securing hospital contracts can take 18-24 months. | Average lead time for new medical device suppliers to establish reliable supply chains: 9 months (early 2025). |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Eyebright Medical Technology is built upon a foundation of comprehensive data, including publicly available financial reports, industry-specific market research from firms like Gartner and Frost & Sullivan, and insights from regulatory bodies such as the FDA.