China Resources Gas Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

China Resources Gas Group Bundle

From Overview to Strategy Blueprint

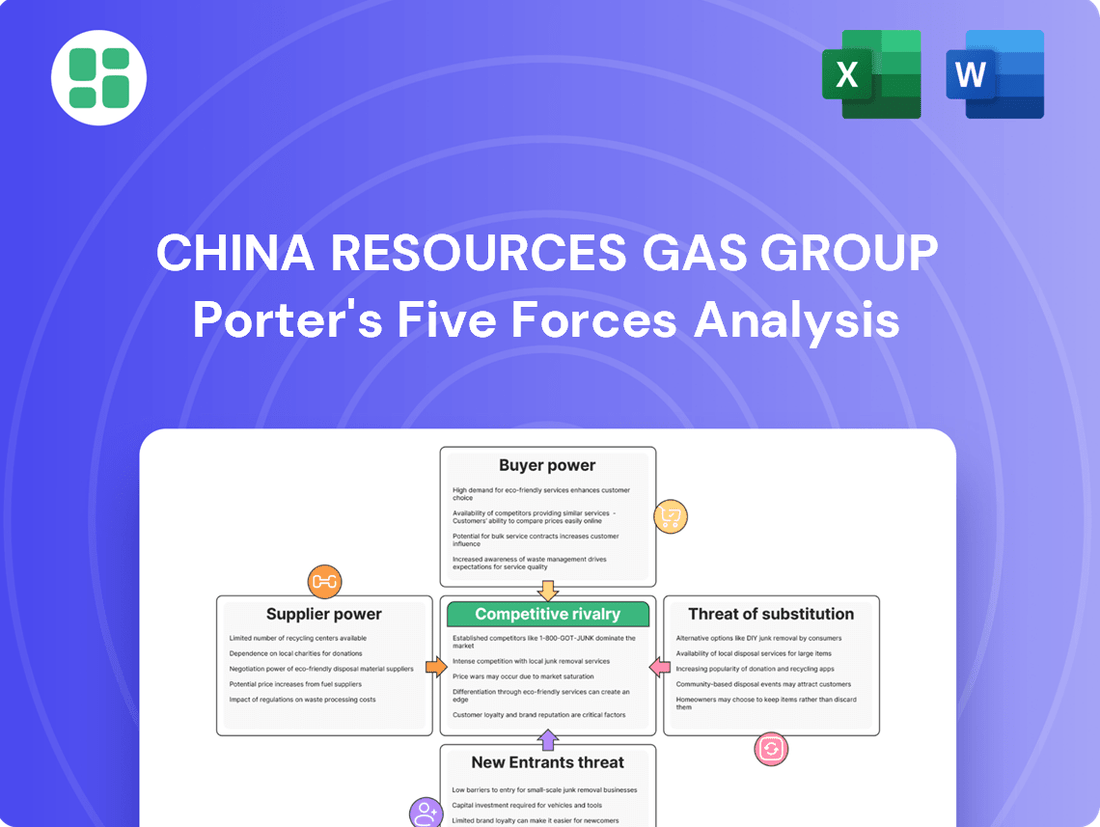

China Resources Gas Group operates within a dynamic energy landscape, facing moderate threats from new entrants and intense rivalry among existing players. Understanding the power of their buyers and the availability of substitutes is crucial for their strategic positioning.

The complete report reveals the real forces shaping China Resources Gas Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Upstream Gas Producers

China Resources Gas Group, a significant player in urban gas distribution, faces substantial bargaining power from its upstream natural gas suppliers. These suppliers, often large state-owned entities for domestic supply and major international corporations for imported liquefied natural gas (LNG) and pipeline gas, are few in number.

This limited pool of upstream producers means they hold considerable sway over pricing and the terms of supply agreements. For instance, in 2023, China's domestic natural gas production saw a notable increase, with state-owned giants like PetroChina and Sinopec being major contributors, yet their pricing power remains significant due to the capital-intensive nature of extraction and the strategic importance of energy.

Consequently, China Resources Gas Group's dependence on these key suppliers makes it vulnerable to fluctuations in supply, pricing adjustments, and even geopolitical events that can affect global energy markets, directly impacting the company's cost structure and profitability.

Rising Import Dependency and Global Price Volatility

China's natural gas consumption is on an upward trajectory, with imports, especially Liquefied Natural Gas (LNG), expected to fill a significant portion of this demand. This increasing dependence on international sources places China Resources Gas Group in a position where global suppliers, both for LNG and pipeline gas, wield considerable bargaining power.

The year 2024 highlights this trend, with projections indicating that China's natural gas imports could reach new highs, further amplifying the influence of international suppliers. This reliance exposes the group to the volatility of global spot prices and the inherent risks associated with geopolitical shifts, making supply agreements a critical negotiation point.

While long-term supply contracts offer a degree of insulation against immediate price swings, the overarching market conditions remain highly susceptible to global supply and demand dynamics. For instance, in 2023, disruptions in global LNG markets led to significant price increases, demonstrating the tangible impact of these external factors on the cost of gas for importing nations and companies like China Resources Gas Group.

Criticality of Natural Gas as a Core Input

Natural gas is absolutely critical for China Resources Gas Group, forming the very backbone of its gas distribution and sales operations. This means the company has very few options when it comes to its primary raw material, making it heavily reliant on its suppliers.

Because natural gas is so essential, China Resources Gas Group cannot simply swap it out for something else without a complete overhaul of its business. This deep dependence gives suppliers significant leverage, as the company is largely locked into its current supply chain.

In 2023, China's total primary energy consumption reached approximately 5.9 billion tons of standard coal equivalent, with natural gas playing an increasingly important role. This growing demand further solidifies the bargaining power of natural gas suppliers in the market.

High Switching Costs for Supply Sources

China Resources Gas Group faces considerable supplier power due to high switching costs. Shifting between major gas supply contracts, developing new domestic production fields, or expanding import infrastructure such as LNG terminals or cross-border pipelines requires significant capital expenditure and extended lead times. These substantial investments create high switching costs, limiting the Group's ability to rapidly change suppliers when faced with unfavorable terms.

These high switching costs directly translate to increased bargaining power for suppliers. For instance, securing long-term contracts for pipeline gas from national oil companies or investing in specialized LNG regasification terminals means China Resources Gas Group is locked into these arrangements for extended periods. This lack of immediate flexibility empowers suppliers to dictate terms, impacting the Group's profitability and operational agility.

- High Capital Expenditure: Developing new domestic gas fields or building LNG import terminals can cost billions of dollars, making it impractical to switch suppliers frequently.

- Long-Term Contracts: Existing supply agreements are often for decades, binding China Resources Gas Group to current providers.

- Infrastructure Dependency: Reliance on specific pipeline networks or LNG terminals means suppliers controlling these assets hold significant leverage.

- Regulatory Hurdles: Obtaining approvals for new infrastructure or supply routes can be a lengthy and complex process, further cementing supplier relationships.

Governmental Influence and Policy Directives

The Chinese government's direct involvement in the natural gas sector significantly shapes the bargaining power of suppliers. Policies regarding import quotas, approval of critical infrastructure like pipelines, and directives influencing domestic production levels all fall under governmental purview. This oversight can create a more predictable supply environment for companies like China Resources Gas Group, but it also means that suppliers, particularly state-owned entities, are often operating under national strategic mandates. These directives can impact the availability and pricing of gas, thereby reducing the urban gas operator's direct negotiation leverage with these suppliers.

For instance, in 2024, China continued to emphasize energy security, which often translates to prioritizing domestic production and carefully managing import volumes. This governmental control over supply channels can limit the ability of gas distributors to secure more favorable terms from suppliers, as the ultimate decision-making power often rests with state regulators. The approval process for new pipeline projects, a crucial factor in supply diversification, also highlights this dynamic, giving the government considerable influence over who can supply gas and under what conditions.

- Governmental Control: The Chinese government sets import quotas and approves major pipeline projects, directly influencing gas supply availability.

- State-Owned Suppliers: Key suppliers often operate under state directives, impacting their pricing and supply flexibility.

- Reduced Negotiation Leverage: China Resources Gas Group's ability to negotiate favorable terms is constrained by these top-down policy directives.

Suppliers' Strong Hand: Shaping Gas Group's Costs

The bargaining power of suppliers for China Resources Gas Group is substantial, primarily due to the concentrated nature of natural gas producers, both domestically and internationally. These suppliers, often large, state-backed enterprises or major global energy firms, have significant leverage because of the critical and non-substitutable nature of natural gas for the Group's operations.

High switching costs further bolster supplier power. Building new infrastructure, like LNG terminals or pipelines, and securing long-term contracts involve immense capital investment and time, locking China Resources Gas Group into existing relationships. This lack of flexibility allows suppliers to dictate terms, impacting the Group's cost structure and profitability.

Government policies in China also play a crucial role, often favoring state-owned suppliers and influencing supply availability and pricing. This governmental oversight can limit China Resources Gas Group's negotiation leverage, as ultimate decisions on supply channels and critical infrastructure often rest with regulators, making it challenging to secure more favorable terms.

| Factor | Impact on China Resources Gas Group | Supporting Data/Context (as of mid-2024) |

|---|---|---|

| Supplier Concentration | High; few domestic and international suppliers dominate the market. | China's domestic gas production is heavily concentrated among state-owned giants like PetroChina and Sinopec. Imported LNG also comes from a limited number of major global producers and trading houses. |

| Switching Costs | Very High; significant capital investment and long lead times for new infrastructure. | Developing LNG import terminals can cost billions of dollars. Long-term pipeline contracts can span decades, creating substantial barriers to changing suppliers. |

| Importance of Input | Critical; natural gas is the core product for distribution and sales. | Natural gas is essential for urban heating and industrial use, making it irreplaceable for China Resources Gas Group's business model. |

| Governmental Influence | Significant; policies on import quotas and infrastructure approval affect supply. | China's emphasis on energy security in 2024 influences import volumes and domestic production mandates, directly impacting supplier relationships and negotiation power. |

What is included in the product

This analysis unpacks the competitive landscape for China Resources Gas Group, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Gain immediate clarity on competitive pressures, allowing China Resources Gas Group to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Fragmented Residential and Commercial Customer Base

China Resources Gas Group's customer base is incredibly widespread, serving millions of homes and businesses across many different cities. This sheer volume means that no single customer, or even a small group, has much sway. For instance, in 2023, the company reported serving over 30 million residential customers, highlighting the immense fragmentation.

Individually, these residential and commercial customers have very little bargaining power. Their gas consumption is typically small, and since gas is a necessity, they have limited ability to negotiate prices or terms. This essential nature of the service further weakens their individual leverage.

The company's vast network of city gas projects, operating in numerous urban areas, reinforces its strong position against any significant customer-driven influence. This widespread infrastructure means customers are largely dependent on China Resources Gas Group for their essential energy needs.

Price Sensitivity of Industrial Customers

Industrial customers, particularly those with significant natural gas consumption, demonstrate a heightened price sensitivity. This is especially true in a decelerating economy where cost optimization becomes paramount. They are more inclined to explore alternative energy sources if natural gas prices become unmanageable, giving them considerable bargaining leverage.

For China Resources Gas Group, this means that large industrial clients can exert substantial influence on pricing. In 2023, for instance, industrial gas consumption in China represented a significant portion of total demand, and any shifts in their purchasing power could directly impact the company's revenue streams. The group must therefore carefully manage its pricing strategies to retain these crucial customers.

High Switching Costs for End-Users

For most piped natural gas customers, the cost and inconvenience associated with switching to an alternative energy source, like converting heating systems from gas to electricity, are substantial. This structural barrier significantly limits the direct bargaining power of the end-consumer. For instance, in 2024, the average cost to retrofit a residential property for electric heating was estimated to be between $5,000 and $15,000, a significant deterrent for consumers.

Government Regulation of Gas Prices

Government regulation significantly impacts the bargaining power of customers in China's gas market, particularly for residential users. Residential gas prices in China are often regulated to ensure affordability and social stability. This regulatory framework limits China Resources Gas Group's ability to fully pass on increased procurement costs to its household customers, effectively capping potential revenue from this crucial segment and empowering the regulator on behalf of the consumer. While reforms are ongoing to rationalize the residential gas price mechanism, the current structure grants considerable leverage to end-users through governmental oversight.

The regulated nature of residential gas prices directly curtails China Resources Gas Group's pricing flexibility. For instance, in 2023, while global natural gas prices experienced volatility, the domestic residential gas price adjustments were managed cautiously by authorities. This regulatory intervention means that even if the company faces higher import costs, it cannot unilaterally increase prices for a large customer base, thereby strengthening the customers' position by proxy.

- Regulated Pricing: Residential gas prices are capped, limiting the company's ability to pass on cost increases.

- Affordability Focus: Government prioritizes social stability and affordability for households.

- Limited Revenue Potential: The inability to adjust prices freely caps revenue growth from the residential segment.

- Regulator as Customer Advocate: The government acts as a strong representative for consumer interests in price negotiations.

Increasing Downstream Market Competition

Despite high switching costs for individual residential customers, the overall downstream gas market in China is becoming increasingly competitive among urban gas distributors. This intensified competition among operators, such as those in major cities like Beijing and Shanghai, indirectly empowers customers.

Operators are compelled to enhance their service offerings, improve customer support, and explore more competitive pricing strategies, particularly in non-regulated market segments. For instance, by 2024, several urban gas companies reported increased customer acquisition costs due to promotional activities aimed at attracting new users in saturated markets.

- Intensifying Competition: The Chinese urban gas distribution market is seeing a rise in the number of players, leading to greater rivalry.

- Customer Benefits: Increased competition translates to better service packages and potentially lower prices in non-regulated gas services.

- Operator Response: Gas companies are investing more in customer service and marketing to retain and attract users.

Customer Power Dynamics in China's Gas Market

While individual residential customers have minimal power due to essential needs and high switching costs, large industrial clients can exert significant influence. These industrial users, often price-sensitive, can negotiate favorable terms or explore alternatives, especially during economic slowdowns. In 2023, industrial gas consumption was a substantial part of China's energy mix, making these customers crucial for revenue, and by 2024, their bargaining power was amplified by a focus on cost optimization.

Government regulation significantly limits the bargaining power of residential customers, as prices are often capped for affordability and social stability. This regulatory oversight, which prioritizes consumer interests, means China Resources Gas Group cannot freely adjust prices to reflect higher procurement costs. For instance, in 2023, domestic residential gas price adjustments were carefully managed, limiting the company's ability to pass on market volatility.

The increasing competition among urban gas distributors in China, particularly in major cities, indirectly empowers customers. This rivalry forces companies to improve services and offer competitive pricing, especially in non-regulated areas. By 2024, this competitive landscape led to higher customer acquisition costs for gas companies due to promotional efforts in saturated markets.

| Customer Segment | Bargaining Power Factors | Impact on China Resources Gas Group | 2023/2024 Data Point |

|---|---|---|---|

| Residential | Low (Essential need, high switching cost, regulated prices) | Limited pricing flexibility, capped revenue potential | Residential gas prices adjusted cautiously in 2023 despite global price volatility. |

| Industrial | High (Price sensitivity, potential for alternatives, significant volume) | Direct influence on pricing, revenue stream vulnerability | Industrial gas consumption represented a significant portion of total demand in 2023. |

| Overall Market | Increasing (Intensifying competition among distributors) | Pressure to improve service and offer competitive pricing | Customer acquisition costs increased by 2024 due to market competition. |

Full Version Awaits

China Resources Gas Group Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces Analysis for China Resources Gas Group, detailing the competitive landscape and strategic implications. The document you see here is the exact, fully formatted analysis you will receive immediately after purchase, offering actionable insights into the industry's dynamics.

Rivalry Among Competitors

Fragmented Urban Gas Market with Regional Players

The urban gas distribution sector in China, though featuring major entities like China Resources Gas Group, is characterized by a significant number of provincial and municipal gas companies. This fragmentation fuels robust competition, especially when vying for new city gas distribution rights and extending reach into emerging urban areas.

In 2023, China's urban gas consumption reached approximately 240 billion cubic meters, with competition intensifying as companies sought to capture market share. This competitive landscape means that securing and maintaining concessions often involves aggressive pricing and service offerings.

Competition for New City Concessions and Projects

China Resources Gas Group faces intense competition from other major urban gas operators vying for lucrative new projects and exclusive concessions across China's cities. This rivalry is evident in the significant upfront capital expenditures and sophisticated bidding strategies required to secure these expansion opportunities. For instance, in 2023, the total investment in China's urban gas pipeline network construction reached approximately 200 billion yuan, highlighting the scale of capital deployment and the competitive landscape.

Government-Driven Market Reforms and Consolidation

The Chinese government's ongoing market-based reforms, particularly the drive to integrate urban pipeline gas networks, are a significant force reshaping the competitive landscape for companies like China Resources Gas Group. This policy aims to create more efficient and unified gas distribution systems across the country.

This push for integration is directly fueling industry consolidation. As smaller or less efficient players are absorbed or exit, the remaining large entities, including China Resources Gas, are likely to face intensified rivalry. They will be competing more fiercely for regional dominance and operational efficiencies in a more concentrated market.

For instance, in 2023, China's natural gas consumption reached approximately 370 billion cubic meters, highlighting the sheer scale of the market and the strategic importance of these reforms. Companies that can adapt to and leverage these consolidation trends, improving their operational scale and regional reach, will be better positioned for success.

Differentiation in Service Offerings and Value-Added Services

China Resources Gas Group faces intense rivalry not just on natural gas supply, but also on a range of value-added services. These include crucial offerings like pipeline installation and maintenance, sales of gas appliances, and increasingly, integrated energy solutions designed for efficiency and sustainability.

Differentiation is key, with companies like China Resources Gas Group focusing on superior service quality, leveraging technological innovation, and providing comprehensive energy management solutions to stand out. For instance, in 2023, China Resources Gas Group reported revenue from value-added services and other businesses contributing significantly to their overall financial performance, showcasing the importance of these offerings.

- Pipeline Installation and Maintenance: Ensuring safe and efficient delivery networks.

- Gas Appliance Sales: Offering a range of modern and energy-efficient appliances.

- Integrated Energy Solutions: Providing holistic energy management for residential and commercial clients.

- Customer Service Excellence: Differentiating through responsive and high-quality support.

Impact of Slowing Natural Gas Demand Growth

The anticipated moderation in China's natural gas demand growth, with projections suggesting a deceleration from the robust expansion seen in prior periods, is poised to intensify competitive pressures within the sector. This shift means companies like China Resources Gas Group will likely face a more challenging environment as they vie for market share in a market that is expanding at a less rapid pace.

As the overall market growth slows, the competition among existing players for each percentage point of market share will inevitably become more pronounced. This heightened rivalry can lead to price wars and increased marketing expenditures, ultimately impacting profitability and demanding greater operational efficiency to maintain or grow market position.

- Slowing Demand Growth: China's natural gas demand growth is projected to slow down, impacting market expansion.

- Increased Rivalry: Companies will compete more intensely for a larger share of this moderately growing market.

- Margin Pressure: Aggressive competition is likely to put downward pressure on profit margins for industry participants.

- Efficiency Imperative: Businesses will need to enhance their operational efficiency to succeed in this more competitive landscape.

China's Urban Gas: Billions Invested, Competition Intensifies

Competitive rivalry within China's urban gas sector is fierce, with numerous provincial and municipal players challenging established giants like China Resources Gas Group for new concessions and market share. This dynamic is amplified by significant capital investments, with approximately 200 billion yuan invested in urban gas pipeline construction in 2023 alone, underscoring the intense competition for expansion opportunities.

The drive for industry consolidation, spurred by government reforms, is further intensifying rivalry among the remaining large entities. Companies are not only competing on gas supply but also on value-added services such as installation, maintenance, and integrated energy solutions, with China Resources Gas Group seeing significant revenue from these areas in 2023.

As China's natural gas demand growth moderates, the competition for each percentage point of market share is expected to intensify, potentially leading to price wars and increased marketing expenses, impacting profit margins for all players.

| Metric | 2023 Value (Approx.) | Significance |

|---|---|---|

| Urban Gas Consumption (Billion m³) | 240 | Indicates market size and growth potential |

| Urban Gas Pipeline Investment (Billion Yuan) | 200 | Reflects capital intensity and competitive bidding |

| Natural Gas Consumption (Billion m³) | 370 | Overall market scale for natural gas |

SSubstitutes Threaten

Rapid Growth of Renewable Energy Sources

The rapid growth of renewable energy sources like solar and wind power in China presents a substantial threat of substitution for natural gas. This is especially true in sectors like power generation and residential heating, where gas has traditionally been a dominant fuel. China's commitment to clean energy is evident in its ambitious targets, with installed solar capacity alone expected to exceed 1,000 GW by 2025, signaling a clear move away from fossil fuels.

Persistent Reliance on Coal

Despite China's ambitious environmental goals, coal's persistent prevalence poses a significant threat of substitutes for natural gas. In 2024, coal still accounted for a substantial portion of China's primary energy consumption, often remaining more cost-effective for industrial processes and electricity generation compared to natural gas.

Government policies, while promoting cleaner energy, sometimes balance this with energy security concerns, which can lead to continued support for coal production. This can slow down the transition to natural gas, limiting its market penetration and making it a less dominant substitute in certain sectors.

Increasing Electrification Across Sectors

The increasing electrification across residential heating, industrial processes, and transportation, particularly the surge in electric vehicles, directly diminishes the demand for natural gas. This technological and policy-driven transition poses a significant and growing threat to China Resources Gas Group's core business and sales volumes.

Availability of Alternative Fossil Fuels

The availability of alternative fossil fuels presents a significant threat to China Resources Gas Group. Liquefied petroleum gas (LPG) and other petroleum products can directly substitute for natural gas, particularly in areas with less developed piped natural gas networks or for specific industrial processes. This substitution is often driven by price fluctuations and the relative cost-effectiveness of these alternatives.

Economic considerations play a crucial role in this substitution dynamic. For instance, while natural gas is generally favored for its environmental benefits, substantial price advantages offered by LPG or other petroleum products can compel consumers, especially in the industrial and commercial sectors, to switch. In 2024, global energy markets saw continued volatility, with the price of natural gas experiencing fluctuations influenced by supply chain issues and geopolitical events, making the cost comparison with alternatives even more critical for end-users.

The threat is amplified by the existing infrastructure for these alternatives. Many regions already have established distribution networks for LPG and other petroleum fuels, reducing the switching costs for consumers. This readily available infrastructure means that customers can adopt substitutes with relative ease, increasing the competitive pressure on natural gas providers like China Resources Gas Group.

- Substitution Risk: LPG and petroleum products offer viable alternatives to natural gas, especially where piped infrastructure is limited.

- Economic Drivers: Price competitiveness of alternatives is a primary factor influencing consumer choice and substitution.

- Infrastructure Advantage: Existing distribution networks for LPG and petroleum products lower switching costs for consumers.

- Market Volatility: Fluctuations in energy prices in 2024 highlighted the sensitivity of the market to the cost differential between natural gas and its substitutes.

Government Policy Favoring Cleaner Energy Transition

China's government is actively promoting a shift to cleaner energy sources, which presents a significant threat of substitutes for natural gas. The nation's 14th Five-Year Plan (2021-2025) and recent energy legislation clearly outline a long-term strategy focused on reducing carbon emissions and developing a low-carbon economy.

This policy framework directly encourages the expansion of renewable energy technologies, such as solar and wind power, and promotes greater energy efficiency. Consequently, these cleaner alternatives are increasingly positioned as viable substitutes for natural gas across various sectors of the economy.

- Renewable Energy Growth: China aims to increase the share of non-fossil fuels in its primary energy consumption to around 20% by 2025, a substantial increase from previous years.

- Coal-to-Gas Switching Reversal: While earlier policies encouraged switching from coal to gas, current trends and future plans are more focused on renewables, potentially dampening future gas demand growth.

- Policy Incentives: Government subsidies and preferential policies for renewable energy projects make them more competitive against natural gas.

Competing Energies: The Threat to Natural Gas in China

The threat of substitutes for China Resources Gas Group is multifaceted, encompassing both cleaner energy alternatives and other fossil fuels. Renewable energy sources, particularly solar and wind, are rapidly gaining traction due to government policy and falling costs, directly competing in power generation and heating. Furthermore, the continued reliance on coal, especially in industrial applications, remains a persistent substitute due to its cost-effectiveness, despite environmental concerns. Electrification, driven by electric vehicles and industrial processes, also directly erodes natural gas demand.

| Substitute Type | Key Drivers | Impact on Natural Gas Demand | 2024 Data/Trends |

|---|---|---|---|

| Renewable Energy (Solar, Wind) | Government policy, declining costs, environmental targets | Reduces demand in power generation and heating | China's installed solar capacity projected to exceed 1,000 GW by 2025; renewables target of ~20% of primary energy consumption by 2025. |

| Coal | Cost-effectiveness, energy security concerns | Continues to be a substitute in industrial processes and power generation | Coal still accounted for a substantial portion of China's primary energy consumption in 2024. |

| Liquefied Petroleum Gas (LPG) & Other Petroleum Products | Price fluctuations, existing infrastructure | Direct substitute where piped gas infrastructure is limited; competition based on cost. | Global energy market volatility in 2024 impacted natural gas prices, influencing cost comparisons. |

| Electrification | Technological advancements, government incentives (e.g., EVs) | Decreases demand in transportation, residential heating, and industrial sectors. | Significant surge in electric vehicle adoption continues to displace fossil fuel demand. |

Entrants Threaten

High Capital Investment for Infrastructure Development

Establishing a comprehensive urban gas distribution network, like those operated by China Resources Gas Group, demands substantial upfront capital. This includes significant investment in laying pipelines, constructing storage facilities, and building city-gate stations. For instance, in 2023, the company continued its extensive infrastructure development, with capital expenditures focused on expanding its pipeline network across various cities in China.

Strict Regulatory Hurdles and Licensing Requirements

The natural gas distribution sector in China operates under a rigorous regulatory framework. New entrants must secure numerous licenses and permits, and strictly adhere to safety and environmental standards, making market entry a complex and lengthy undertaking.

Economies of Scale and Established Incumbents

China Resources Gas Group, like other major urban gas operators, enjoys substantial economies of scale. This means they can procure gas at lower prices and spread their fixed infrastructure costs over a larger customer base, giving them a significant cost advantage. For instance, in 2023, their total revenue reached approximately RMB 110 billion, reflecting their vast operational scope.

The sheer size and established market presence of companies like China Resources Gas Group create a formidable barrier to entry. Newcomers would struggle to match the operational efficiencies and customer service levels that incumbents have honed over years, especially when competing on price. This makes it challenging for new entrants to gain a foothold without substantial initial investment and a long-term strategy to overcome these inherent advantages.

Access to Natural Gas Supply and Transmission Networks

Securing reliable and affordable access to natural gas supply, a critical input for China Resources Gas Group, acts as a significant barrier to entry. New companies face immense challenges in establishing robust supply chains, whether through domestic sourcing or international liquefied natural gas (LNG) imports. For instance, China's domestic natural gas production reached approximately 230 billion cubic meters (bcm) in 2023, but securing consistent and cost-effective volumes for a new entrant is complex.

Connecting to the national pipeline transmission network, predominantly controlled by the state-owned PipeChina, represents another formidable hurdle. New entrants would find it exceptionally difficult to gain access to this essential infrastructure without substantial governmental support or strategic alliances. PipeChina's extensive network, covering hundreds of thousands of kilometers, is integral to efficient distribution, and its control significantly limits independent market participation.

- Supply Chain Dependency: New entrants must navigate complex domestic and international procurement channels for natural gas, often requiring long-term contracts and significant capital investment.

- Infrastructure Access: Gaining access to PipeChina's national transmission network is a major impediment, as capacity is often prioritized for established players and requires regulatory approval.

- Capital Requirements: The substantial investment needed to secure gas supply and establish transmission links makes entry prohibitively expensive for most potential competitors.

Government's Strategic Control and Support for State-Backed Entities

The Chinese government's strategic control over the energy sector presents a significant barrier to new entrants. By favoring and actively supporting state-backed entities, such as those within the China Resources Gas Group ecosystem, the government creates an uneven playing field. This implicit preference makes it exceedingly difficult for independent new companies to secure necessary permits, access infrastructure, and compete effectively against well-established, government-aligned players.

For instance, in 2024, the National Development and Reform Commission (NDRC) continued to implement policies prioritizing energy security and the development of national champions. This often translates into preferential treatment for state-owned enterprises in areas like gas pipeline access and distribution rights. New entrants, even with substantial capital, often find themselves navigating a complex regulatory landscape designed to protect and bolster existing state-backed infrastructure.

- Government favoritism towards state-backed enterprises in energy infrastructure.

- Difficulties for independent new entrants in securing permits and access.

- Policies in 2024 continue to prioritize national energy security and state champions.

Gas Sector: High Barriers Deter New Entrants

The threat of new entrants for China Resources Gas Group is relatively low due to significant capital requirements for infrastructure development and securing gas supply. For example, in 2023, China's domestic natural gas production was around 230 billion cubic meters, highlighting the scale of supply chain operations new entrants must manage. Additionally, stringent regulatory hurdles and the dominance of state-owned entities like PipeChina in transmission networks create substantial barriers.

| Barrier Type | Description | Impact on New Entrants |

| Capital Requirements | High upfront investment for pipelines, storage, and city-gate stations. | Prohibitively expensive for most new competitors. |

| Regulatory Hurdles | Complex licensing, permits, and adherence to safety/environmental standards. | Makes market entry a lengthy and difficult process. |

| Economies of Scale | Lower procurement costs and spread of fixed costs for incumbents. | Gives established players a significant cost advantage. |

| Infrastructure Access | Limited access to PipeChina's national transmission network. | Restricts efficient distribution for new market participants. |

| Government Policy | Favoritism towards state-backed energy enterprises. | Creates an uneven playing field for independent entrants. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for China Resources Gas Group leverages data from company annual reports, investor presentations, and official regulatory filings. We also incorporate insights from reputable industry research firms and macroeconomic data providers to offer a comprehensive view of the competitive landscape.